by Brian Levitt, Global Market Strategist, Invesco

Key takeaways

Real estateThe US office market may be struggling, but I don’t believe that stress is systemic to the rest of the commercial real estate market or the US banking system. |

Debt downgradeThe decision by Fitch Ratings to downgrade US debt two months after lawmakers successfully negotiated a debt ceiling deal seems somewhat bizarre to me. |

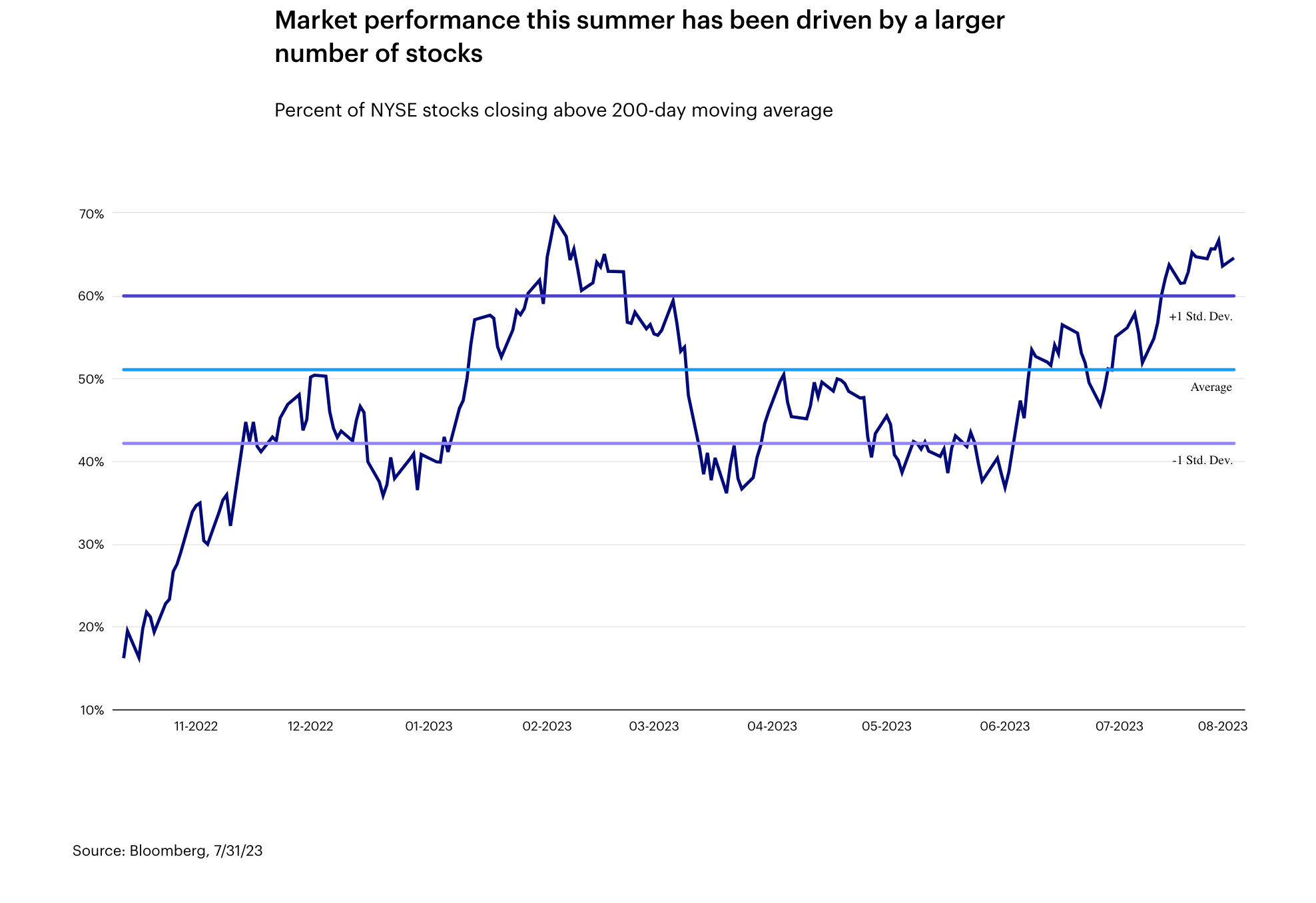

Better breadthThe market today isn’t as concentrated as it was at the start of June. More stocks are contributing to the market’s advance than we saw earlier this year. |

Happy first birthday to Above the Noise!

I celebrated by baking myself a smash cake, hiring a clown, and rereading the first edition. The focus then was on recession risk, inflation, and the Federal Reserve. Clearly, not much has changed. That is, besides the state of the stock market, with the S&P 500 gaining over 13% since ATN first hit the newsstands last August.1

A ’keep it simple’ strategy

We start with three simple questions.

1. Where are we in the cycle?

Economists are tripping over one another to offer their mea culpa on the 2023 recession calls. Perhaps the lagged effects of policy tightening are just lagging for longer this time. A prolonged period of consumers and businesses locking in low rates loans will do that. Official recession or not, I believe an economic downturn in 2024 is likely.

2. What’s the market telling us about the direction of the US economy?

Risk appetite had improved significantly in June and July. This type of reversal in sentiment has historically signaled an improvement in growth expectations and a subsequent improvement in economic data. Historically, that has created a good backdrop for risk assets, particularly cyclical stocks. Admittedly, growth in the near-term may be too strong for risk assets, as higher rates weigh on valuations.

3. What will be the Fed’s policy response?

Will they? Won’t they? Is November in play? Regardless, the Fed Funds futures market suggests that the end of tightening is near.

Tactically we favor cyclical, smaller-cap, and value-oriented stocks. Really, you might ask? Yes — our view reflects the ongoing resilience in the economy and recent improvements across various sectors. The risk to the market is that interest rates continue to climb, but in that environment, we would still expect smaller-cap and value stocks to outperform the mega-cap growth names, which are trading at higher valuations.

It may be confirmation bias …

… but I believe US consumer spending will ultimately moderate. Outstanding credit card debt is $1.26 trillion, up 15% since the beginning of the pandemic.3 Now, I refuse to be one of those “small minds that are impressed by large numbers” that author Sir Arthur Clarke spoke about. The $1.26 trillion needs to be put into context. Still, the average balance per borrower, according to TransUnion, is close to $6,000, the highest in a decade.4 That’s $1,500 per ticket for a family of four to attend the summer’s hottest concert. The math adds up! Kidding aside, the consumer is unlikely to go on like this forever, even with a 3.5% unemployment rate.5

It was said

“…the decision of a credit rating agency today, as the economy looks stronger than expected, to downgrade the United States is bizarre and inept.” – Lawrence Summers, Former US Treasury Secretary

I’m with the former Treasury Secretary on this one. Fitch Ratings cited “a steady deterioration in standards of governance” as its rationale for downgrading US debt from AAA to AA+ on Aug. 1. Yet, the downgrade came two months after lawmakers successfully negotiated a debt ceiling deal. It’s also more than a decade after Standard & Poor’s downgraded the US debt over similar concerns. Since then, US borrowing costs have, for the most part, been historically low6 while the US dollar has been a strong currency.7

A few other points:

- America is not a corporation which can run out of cash.

- There may be a limit to how much debt the US government can take on as a percentage of gross domestic product (GDP), but other countries, such as Japan, have significantly higher debt-to-GDP ratios than the US without having experienced a fiscal shock.8

- Even so, the US is a very wealthy country. Debt-to-GDP may be elevated, but debt compared to US government assets including land, commodities, military, taxing power, and more (all of which may total over $200 trillion) does not appear to be a concern.9

- Yes, today’s higher rates, if sustained, would result in a greater interest burden, but a debt spiral would only occur if interest rates were consistently meaningfully higher than the nominal growth rate of the country.

- Finally, the nation’s politicians can adjust the programs that make up the lion’s share of the nation’s spending.

Special thanks to Fitch for causing a commotion by telling Americans what they largely assumed anyway.

Since you asked: Part 1

Will the challenges in the US office property market result in the next Global Financial Crisis?

It’s true that the US office market is still grappling with the negative effects of pandemic-era shutdowns. Almost one out of every five offices in the US are currently vacant, and none of the major metropolitan areas in the US are going unscathed.10

Fortunately, we don’t believe that the stress in the US office space is systemic to the rest of the commercial real estate market or to the US banking system.

- While vacancies have risen significantly in US offices since the pandemic, other sectors, such as retail strip malls, storage, and single-family rentals have experienced lower vacancy levels than before the pandemic.11

- The commercial mortgage-backed securities market today is roughly 1/5th of the size that the residential mortgage-backed securities market was in 2008.12

- The loan-to-value ratio in the commercial mortgage market is near a multi-year low, down meaningfully from the 2008 crisis.13 This has been driven by more stringent lending standards in the aftermath of the GFC, as well as a significant increase in commercial real estate values over the past decade.

- The banks are significantly better capitalized today than they were in 2008.14

Since you asked: Part 2

Are you concerned about market performance being driven by only a handful of stocks?

The market is not nearly as concentrated as it was at the beginning of June. I’m still getting questions about the bad breadth of the market, all the while nearly two-thirds of the stocks on the New York Stock Exchange closed July above their 200-day moving average.15 It’s no longer just the Magnificent 7 (Apple, Amazon, Alphabet, Nvidia, Meta, Microsoft, Tesla) supporting markets. The market’s advance in June and July was “healthier” than it was from February to May.

Phone a friend

Interest rates have surged since the middle of July. How concerned should we be for risk assets? I posed the question to Matt Brill, Head of Investment Grade for Invesco Fixed Income. His response:

“At some point, the yield curve must normalize. Most people were expecting that the Fed would have to cut rates aggressively because of an economic hard landing. Rather, it doesn’t seem likely we will get a recession in the next two quarters or maybe even further out. As a result, the 10-year Treasury rate probably needed to be a little bit higher than it was in the spring. Still, the expectation is that the Fed is going to cut rates at some point in 2024.16 The long rate will then likely be in this 3.5% to 4.0% range. Eventually you get a more normalized curve, but it happens through a slower process, because the Fed isn’t forced to respond to a very negative outcome. This slow process should be bullish for equities and credit.”

Automate my job?

Each month I pose a question to ChatGPT — the artificial intelligence-driven chatbot — and assess the response.

Q: Is a bear steepening of the US Treasury yield curve bad for stocks?

A: A bear steepening of the yield curve, where long-term interest rates rise faster than short-term rates, can potentially signal concerns about economic growth and inflation. This could impact stock markets negatively, as it might lead to higher borrowing costs and reduced corporate profitability.

Good answer. I’m watching the 10-year US Treasury yield closely. There’s been a big move higher from the middle of July to the middle of August. If it persists, then that’s a risk to our optimistic market view. I’m with Matt on this one. My instincts tell me that rates will go lower as global growth and inflation moderate but this bears watching.

(Speaking of ChatGPT, I recently had a great conversation with Senior Investment Analyst Ashley Oerth about artificial intelligence — what it is, what it isn’t, and what types of companies may benefit from this technology. Listen in to the conversation and explore more episodes of Market Conversations.)

On the road again

My travels took me to Bloomington, Minnesota, to present at an investment conference. My hotel was not in walking distance to a restaurant. The Twins were in Detroit. So the Mall of America it was. Alas, I didn’t ride the Brain Surge or the Avatar Airbender, but I had a nice meal and walked by much of the 2.87 million square feet of retail space.17 I would place the occupancy rate at around 95%,18 and the mall was packed for a Thursday night. It’s a reminder that not all commercial real estate is created equal, the concerns about office properties notwithstanding.

Is it me or did summer go fast? As the Grateful Dead sang, “Summertime done, come and gone, my, oh, my.”

Copyright © Invesco