by Systematic Investments Team, BlackRock

Macroeconomic uncertainty has sparked questions over the durability of the traditional 60/40 portfolio—highlighting why investors may want to add alternative investments to the mix.

Key points

- The 60/40 portfolio today – Inflation poses a challenge to the traditional stock-bond portfolio. The diversifying nature of the two assets can be sensitive to the level of inflation, which makes rethinking portfolios more critical than ever.

- Rebuilding resilience – A sensible evolution of portfolio construction can include complementing traditional asset classes with alternative sources of return that provide additional diversification.

- Three Ds of alternative diversifiers – When looking for liquid alternatives that can improve portfolio resilience, we believe buyers should look for diversification, durability, and defensiveness.

The 60/40 today

The foundational 60/40 portfolio, where 60% is invested in stocks and 40% in bonds, is the initial starting point for many portfolios. The exact proportion of the mix is often adjusted based on an investor’s time horizon, risk tolerance and financial goals, but the simple, proportional stock-bond combination is core to what is considered by many to be a “diversified” portfolio.

The main premise for the combination is that when growth assets, like stocks, sell off due to economic slowdowns, fixed income assets like bonds typically appreciate. While stocks tend to suffer in a recession due to lower earnings, bonds can rally because central banks typically cut interest rates to support the economy. When central banks ease policy, bond yields drop and bond prices rise. This dynamic means that bonds can provide a shock absorber in the portfolio, helping to cushion overall returns when stocks are falling.

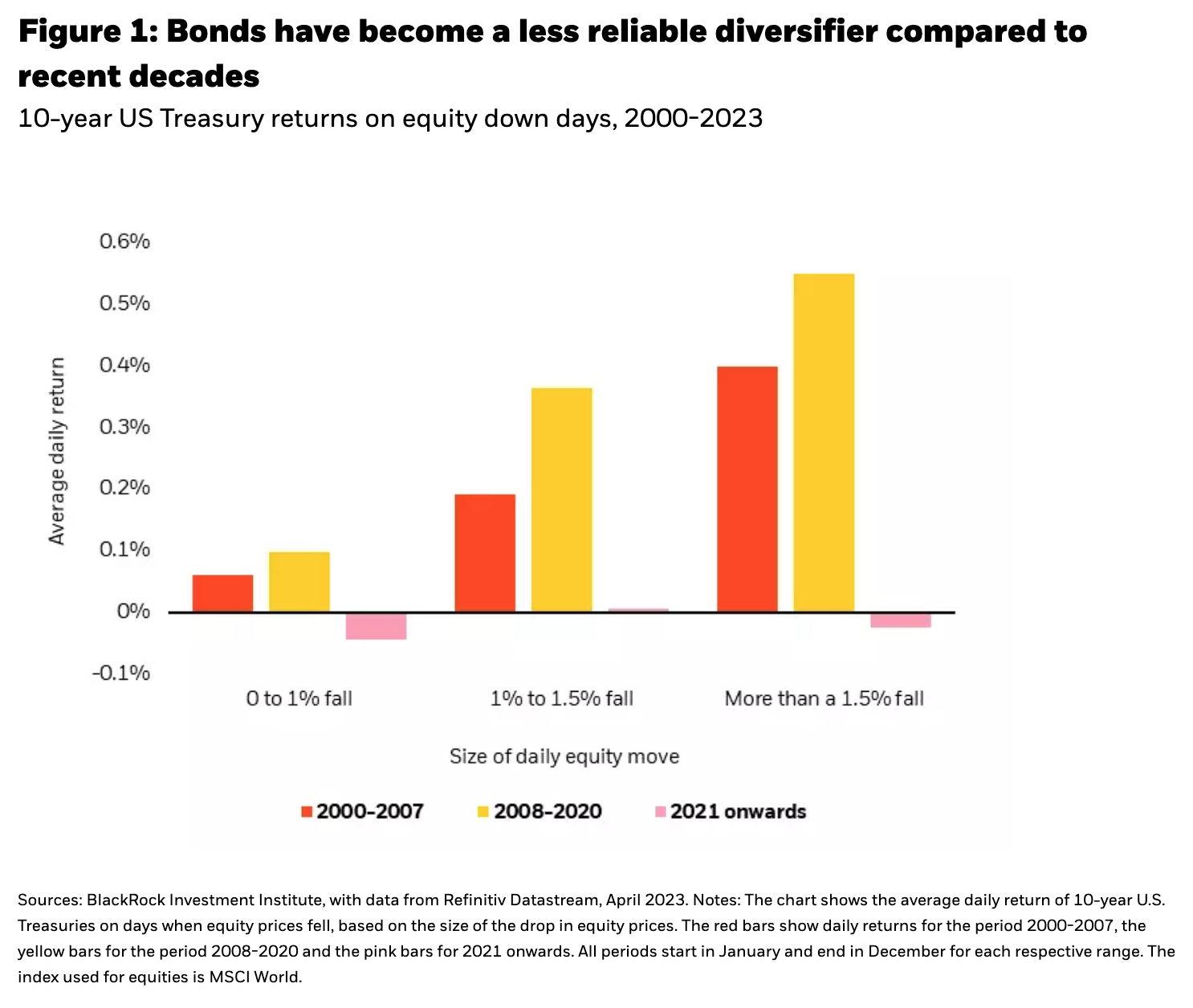

Post-pandemic, the dynamics underpinning the “diversified” 60/40 portfolio have changed. Figure 1 illustrates how over the last two years, the 10-year U.S. Treasury has, on average, delivered negative returns on equity down days. That dynamic is a stark contrast from the diversifying returns of bonds that many investors relied on in the 2000-2007 and 2008-2020 time periods.

This portfolio challenge was on full display in 2022 as stock and bond returns were both meaningfully negative for the calendar year. In 2023, returns have been positive for both stocks and bonds, but the correlation has remained positive. This raises the question: is the “diversified” 60/40 portfolio back?

Our answer is that this largely depends on the future path of inflation. That is because persistent inflation would likely alter the monetary policy dynamics of the previous two decades. With inflation still well above the Fed’s 2% target, the Fed is less likely to materially cut interest rates in the face of a growth slowdown. That is because they would likely prioritize achieving their inflation target over cushioning a short-term downturn in economic growth. As a result, bonds may not offer the same degree of ballast in a 60/40 portfolio.

Rebuilding resilience

With the 60/40 portfolio becoming increasingly challenged, now may be the time to consider alternatives that can add diversification and target new sources of return.

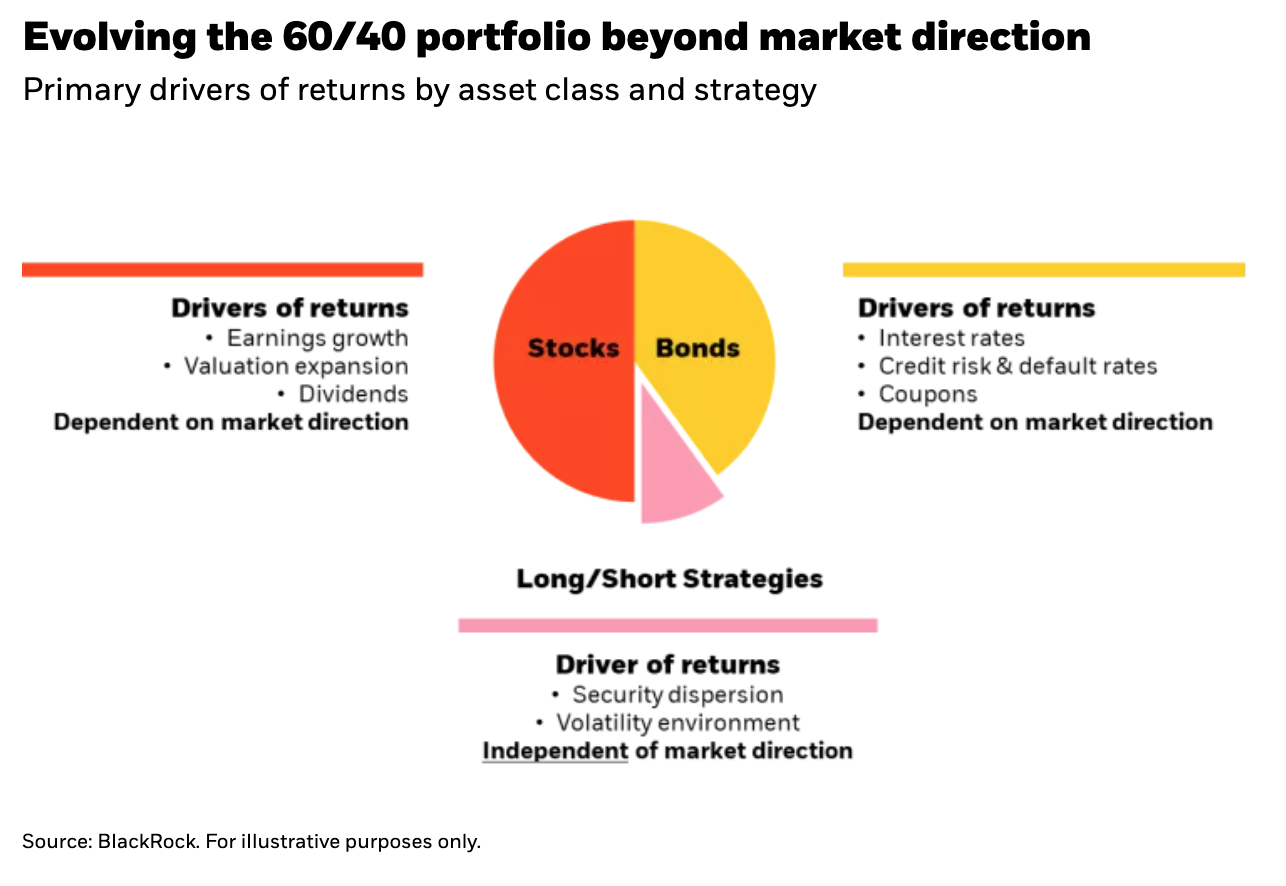

One way to do this is to look to strategies that go long AND short securities.* Unlike traditional long-only strategies that own “best-in-class” securities that are expected to outperform the market, long/short strategies seek to target the entire opportunity set—what is believed to be the best and the worst investments available. They seek to generate returns by going long securities that will outperform and going short securities that will underperform. In this way they can generate returns on both sides of the market and tap into an opportunity set that long-only investments cannot access (Figure 2).

This type of alternative strategy allows investors to access an alternative source of return, called security dispersion, that is not currently captured in 60/40 portfolios. What is security dispersion? Dispersion is the difference between winners and losers in the market. High dispersion implies a wide difference between winners and losers, while low dispersion implies a narrow difference between winners and losers.

Inflation and policy uncertainty tend to influence security dispersion. For example, individual company returns have become more dispersed as businesses differ in their ability to adapt to challenges like persistent inflation and higher interest rates. Similarly, from a top-down macro perspective, divergence in inflation and growth data across countries has led to different policy responses from central banks—driving greater dispersion in country returns. Long/short strategies can thrive in high dispersion environments because they can go long securities that may become outsized winners and go short securities that may become relative losers.

Taking advantage of dispersion can act as another form of return in a portfolio that a traditional 60/40 construct overlooks. Why? The returns of a 60/40 portfolio are based on market direction. Equity returns are driven by growth in earnings, the valuation multiple of those earnings, and to a lesser degree the payment of dividends. These are heavily dependent on the direction of economic conditions and overall direction of equity markets. The same applies to bond returns which are driven by prevailing interest rates, credit spreads, and coupon payments. If market returns are muted or more volatile, buy-and-hold asset allocation becomes considerably less effective.

Dispersion, however, is not dependent on market direction. It can exist in markets with low absolute returns or even downward trending markets—the very time a 60/40 portfolio needs alternative sources of return the most.

The three Ds of alternative diversifiers

Alternative investments can vary widely. Understanding the characteristics of a strategy is crucial because many in the same category or with similar labels may produce vastly different portfolio outcomes.

When looking for an alternative to diversify a portfolio, we believe it’s key to ask if it has historically exhibited the three Ds: diversification, durability, and defensiveness.

First, does the strategy diversify your current portfolio? A telling characteristic to look for is low correlations to other broad asset classes in your portfolio—think risky assets like U.S. and global equities, high yield bonds, or private markets. Many alternative strategies offer strong double-digit returns, but with very high correlation to equities and other risky assets—essentially doubling down on the pre-dominant risk you have in the portfolio. Others offer more modest returns but deliver them without the same level of equity-related risk. Consider finding a middle ground between return potential and low correlations when evaluating alternative diversifiers. Another dimension of an alternative’s diversification potential is the correlation to other alternatives you may already have in your portfolio. A low correlation between another liquid alternative can signal that they are complementary and additive to your current allocation.

Next, does the strategy have a history as a durable source of return? As a long-term holding in an asset allocation, it is key that your capital is put to good use to produce positive returns. Consistent returns with relatively low volatility can help balance out the loss of return from other asset classes, but still deliver stability in a portfolio. Furthermore, a positively skewed upside/downside capture ratio (one where you capture more upside on up days, than downside on down days) can signal that the strategy is not just providing a watered-downed version of market beta, but rather, demonstrating a source of durable return.

Finally, is the strategy defensive when you need it? The timing of returns matter. Potential ways to gauge this is examining how the strategy has historically performed on down equity market days or during specific bouts of market stress—the time diversification is most needed. Shallower drawdowns or even stable to flat returns from an alternative diversifier can indicate defensive qualities. An alternative diversifier may not always exhibit defensiveness across all market environments or events—all investments have ups and downs—but what is essential is the alternative’s diversifying behavior doesn’t consistently disappear at the same time other assets in your portfolio are selling off. An alternative diversifier that is defensive when other assets are under pressure may allow your total portfolio to better weather different market environments.

The long and short of it

Inflation poses a unique challenge to the traditional stock-bond portfolio that we haven’t seen in several decades. The diversifying nature of the stock-bond relationship is under increasing pressure, making resilient portfolio construction more critical than ever.

Long/short strategies have two major benefits for 60/40 portfolios. First, by going short securities they can greatly expand the opportunity set to generate returns and tend to take less directional market exposure. Second, by going long and short they can benefit from increased security dispersion. Dispersion is independent of market direction and can act as a new source of return that is not available in the 60/40 framework.

Finally, when looking for alternative diversifiers, we believe it’s best to ask the right questions. Is it diversifying to your current portfolio? Does it offer a durable source or return? Has it been defensive when the rest of your portfolio needed it most? Adding exposure to the right liquid alternative can help to make portfolios more resilient to not just elevated inflation, but to a range of more disparate market environments.

Copyright © BlackRock