by Ryan James Boyle, Senior Economist, Northern Trust

Around this time three years ago, it was clear our lives were changing. We held out hope that lockdowns and social distancing wouldn’t last forever, but we did spend some time speculating about what might be permanently different. Now, life feels mostly normal, until I look around my office and see a sea of vacant desks. Offices are not the same.

A reckoning has been a long time coming. Even before the pandemic, office real estate had slack capacity in many cities. During the 2020 crisis, I started tracking monthly reports from commercial real estate (CRE) data aggregators, watching for evidence of falling rents or higher office vacancies. My research was premature. Office leases run on long cycles of up to ten years. Most businesses maintained their revenues and were able to honor their lease payments, even as some explored subletting.

As a broad category, CRE has recovered: warehouses and industrial assets saw higher demand in the pandemic, while multifamily and tourism survived a lull and are on firm footing today. Office spaces stand out as the most impaired market.

Commercial real estate lending is a fundamental, mature component of most banks’ portfolios. From construction to operation to resale, banks have a deep understanding of real estate deals. History provides a guide for avoiding mistakes: Excessive lending into commercial developments was one of the drivers of the savings and loan crisis of the 1980s, as troubled lenders took greater risks in search of higher returns.

Reforms and modernization led to a period of relative stability, until 2008. Stress in commercial mortgage backed securities (CMBS) showed there were no safe havens in the global financial crisis. Today, worries about the stability of the banking sector are bringing attention to these potentially troubled assets on banks’ balance sheets.

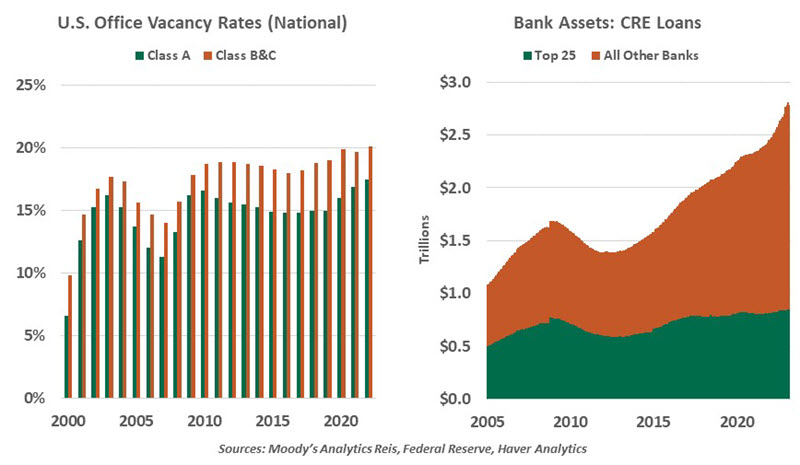

The exposure is substantial. U.S. banks hold about 39% of the nation’s outstanding CRE debt, a share totaling $2.8 trillion. Of that subset, 30% is held by the 25 largest banks, leaving smaller banks with the majority of these assets. According to Trepp, $270 billion of bank-held commercial mortgages will mature this year. Cracks are emerging, with banks issuing warnings of distress in their portfolios.

Smaller banks tend to lend to projects within their communities. Office real estate looks very different once an underwriter moves outside of central business districts. Offices in outlying areas are likely to be smaller professional centers with lower values and more predictable demand than urban skyscrapers. Contagion is still possible as small banks may participate in syndication loans tied to larger projects, but this is a small share of most banks’ portfolios.

In general, commercial loans held by banks will consist of smaller and older, Class B/C buildings, as well as properties under construction. Loans on leased, top-tier, Class A buildings will usually be repackaged into CMBS to attract a wider range of investors. The CMBS market may face some discomfort as well, as deals structured five or ten years ago must be refinanced in a different market environment than they enjoyed at their origination. However, these structures often have supplemental credit protection that should forestall the worst outcomes. Banks may not have the same buffer in their own underwriting.

Too many jobs have gone remote for offices to entirely return to their old norm

Property cycles have played out in the past. The challenge today is a difficult combination of lower demand for office space and substantially higher borrowing costs. Even AAA-rated corporate bonds witnessed a tripling of interest rates. CRE deals previously premised on low borrowing costs will be strained.

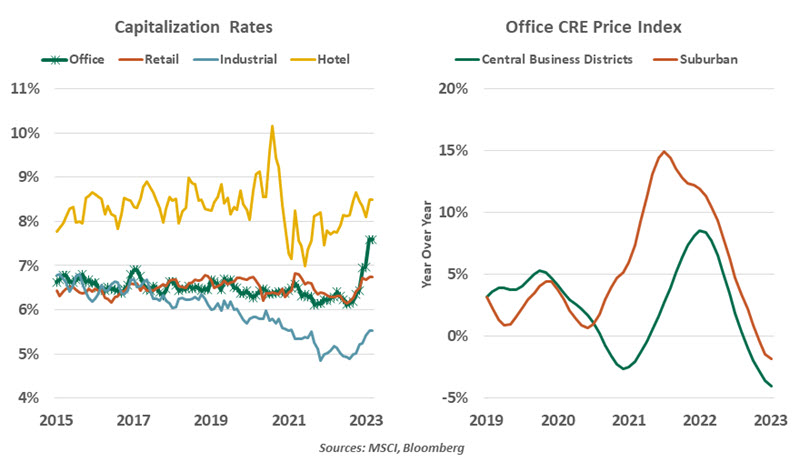

CRE is often described by its capitalization (or “cap”) rate, the ratio of a property’s income to its value, akin to an inverted equity multiple. Lower values and lower income are making cap rates volatile. Higher vacancies are giving tenants more leverage to negotiate lease payments down, pressuring income. Higher interest is thinning property owners’ margins. The uncertainty has made investors less willing to enter the space, depressing property values. With so much unsteadiness, negotiating new deals will prove challenging for all parties.

If a property has lost value at the end of a loan’s term (as short as three or as long as ten years), some pain will follow. A CBRE review of five-year loans issued in 2018-2020 revealed a funding gap (the difference between the asset’s new value and available credit) of over $50 billion. A committed property owner could put up additional capital to maintain the loan covenant. The lender can alter the terms of the loan to accommodate a less favorable cap rate. Though derided as “extend and pretend” or “delay and pray,” the approach is consistent with a belief that the properties will recover their value. This strategy was used to good effect following the financial crisis, as rising property values kept banks from realizing transitory declines in value of their CRE loans. Banks disclose few specifics about their CRE portfolios, and many extensions or losses will remain confidential. And distressed debt buyers are waiting in the wings if a deal cannot be found.

Real estate cycles play out over long horizons.

Though challenged, office properties did not become worthless overnight. Central business districts may feel overbuilt, but they are not dormant: Many offices are logging regular activity three days a week, with a few notable employers requiring a return to the old norm of five days in office.

Longer term, disused offices in otherwise desirable areas can be converted to other uses, like entertainment and multifamily. These projects won’t work for all properties, and will come at a high cost (requiring more financing), but they demonstrate the underlying value of commercial structures. An analogy can be drawn between offices today and shopping malls ten years ago: today, malls vary from thriving to languishing to abandoned to repurposed. Real estate in desirable locations will eventually find its highest and best use.

The years ahead for office real estate will undoubtedly be challenged. Banks will face impairments, and owners may need to find new capital or be forced to sell. My monitoring will continue beyond just data: I’ll stay on the lookout for empty desks and dark offices.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

Copyright © Northern Trust