by Rick Rieder, CIO, Global Fixed Income, Blackrock

The Aiguille du Midi, neighboring popular Mont Blanc in the French Alps, is famous for having the highest vertical ascent cable car in the world, a vertigo-inducing ride that is equal parts scary and awe-inspiring (see Figure 1). The mountain is so high, and the incline so steep, that there is a rest stop complete with bar and café along the 9,200-foot vertical journey, almost anticipating that some riders will inevitably be too impatient, or frightened, to continue. Skiers who do complete the journey to the top are rewarded by over 14 miles of exhilarating slopes as they coast effortlessly (in good conditions) back down to the village of Chamonix, nestled in the valley below.

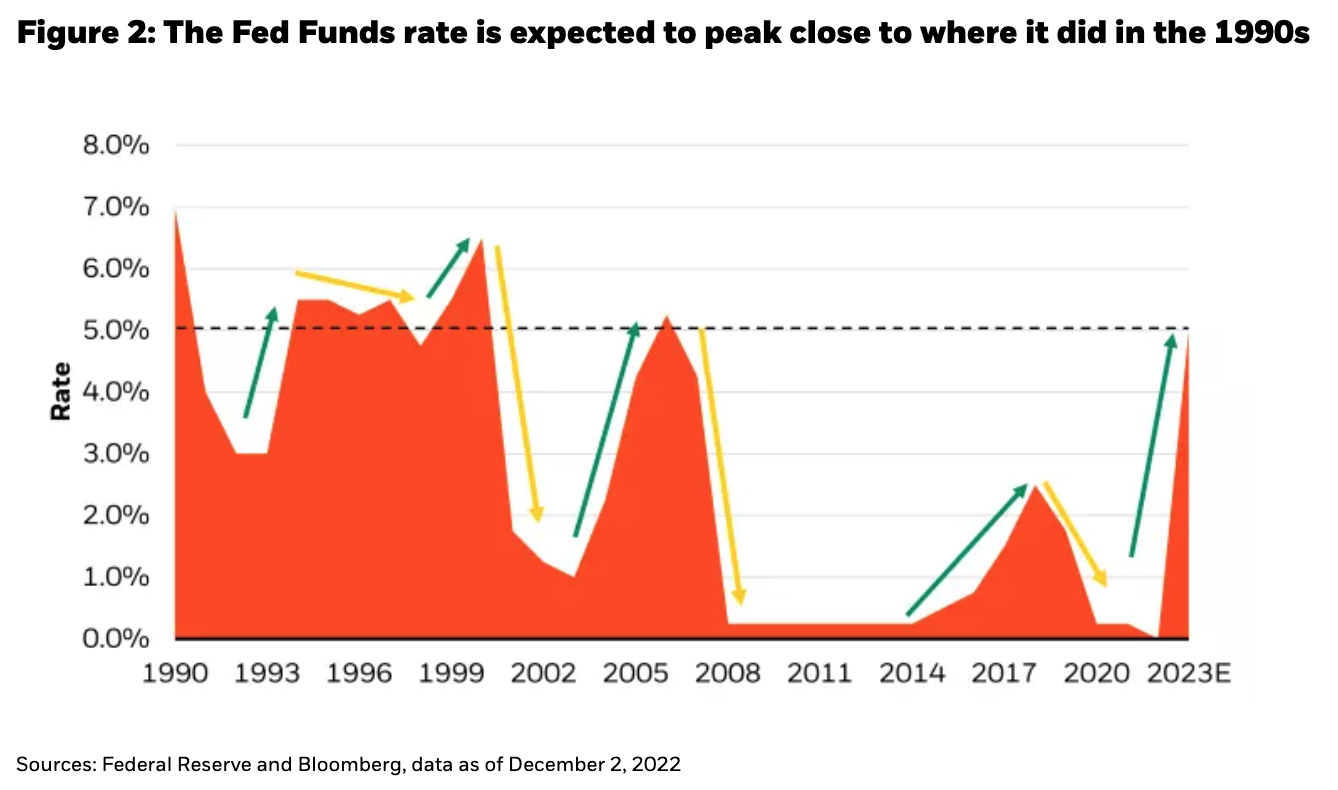

For many fixed income investors, the ascent of interest rates in 2022 has been similarly vertigo-inducing. However, history suggests that the higher the discount rate mountain rises, the longer the runway of positive returns that a fixed income investor can “coast” down on the other side - it’s just very difficult to identify exactly how high that peak (terminal rate) is, or once that peak is reached, what the slope on the other side looks like. Indeed, the current hiking cycle is the steepest in 15 years, and the market is projecting its peak to rival those of the ‘90s – creating a lot of vertical on the other side (see Figure 2).

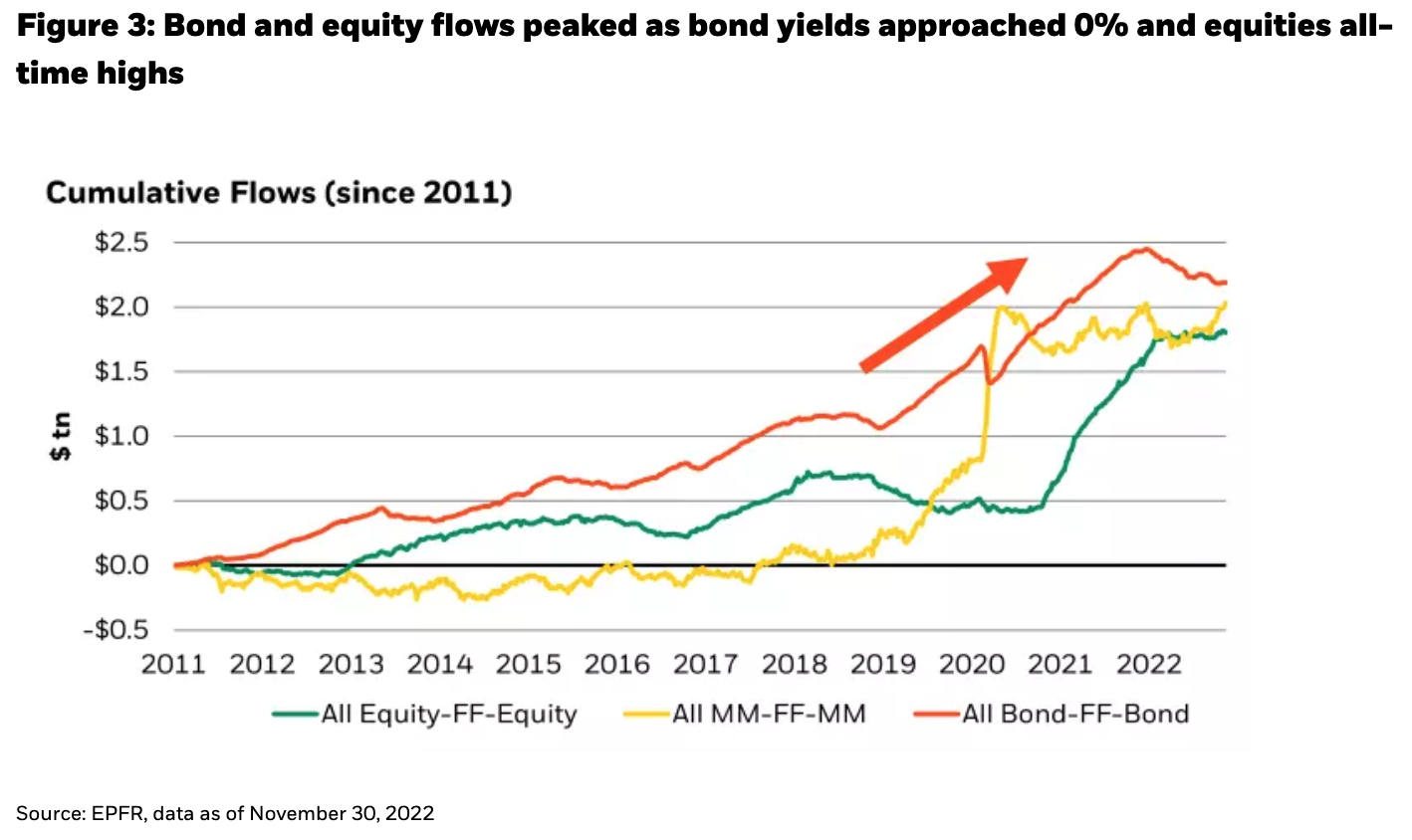

Contrary to what one might expect, investment inflows tend to dry up at higher yields, and to accelerate the lower bond yields go, the equivalent of a skier prematurely disembarking a chairlift, and then speeding up as they approach the end of that truncated run (see Figure 3). At times, this behavior can be the result of what an investor may need to do rather than what they may want to do, as we wrote extensively about in our May 2021 Market Insights commentary, “Investors’ Wants Can be Very Different From Their Needs,” briefly excerpted below:

“Investors generally want to “buy low, sell high” – to buy more bonds at higher yields (lower prices) and fewer bonds at historically low yield levels. However, what investors often need to do is to meet income requirements in order to match liabilities. Hence, they are often forced to buy more bonds at lower yields (to raise sufficient dollars of future annual income), such that they end up being overweight when yields are at their lowest.”

Still, there is another contributing factor to this phenomenon: since the Great Financial Crisis, central banks have almost entirely determined what the terrain for financial assets should look like, and consequently have cajoled investors into buying assets when there is no alternative (TINA), or to sell them when prices have cheapened markedly (for fear that central banks won’t step in to halt said falling prices). This also helps explain the moral hazard behind gamma gambling (a term we coined and explained in our last commentary), and why investors today pore over central bank press statements. In fact, some investors almost behave like cellular biologists, peering through their microscopes, painstakingly trying to decipher the difference between “some participants,” “many participants,” or “most participants,” as it pertains to Committee policy rate decisions. Unfortunately, these kinds of questions have become imperative in navigating today’s investment landscape.

Could this be changing in 2023?

Instead of using a microscope, which isn’t very helpful in observing a mountain, perhaps investors might find a zoomed out wide-angle lens more useful in navigating 2023, and beyond. Growth and inflation are slowing globally, from liquidity-charged levels toward something closer to equilibrium, suggesting that central banks could finally be taking a back seat, thereby allowing for more dramatic regional, sector, and idiosyncratic differentiation to manifest. According to Goldman Sachs forecasts, world nominal GDP is likely to drop from 10% in 2022 to 6% in 2023, with the U.S. following a similar trajectory.

Where once it may have made sense for investors to focus their energies on figuring out central banks’ next move, while using passive tools to implement investment strategies oriented around those moves, in a vacuum of central-bank-driven news flow, picking what to own based on security-by-security analysis becomes the more appealing way to differentiate return.

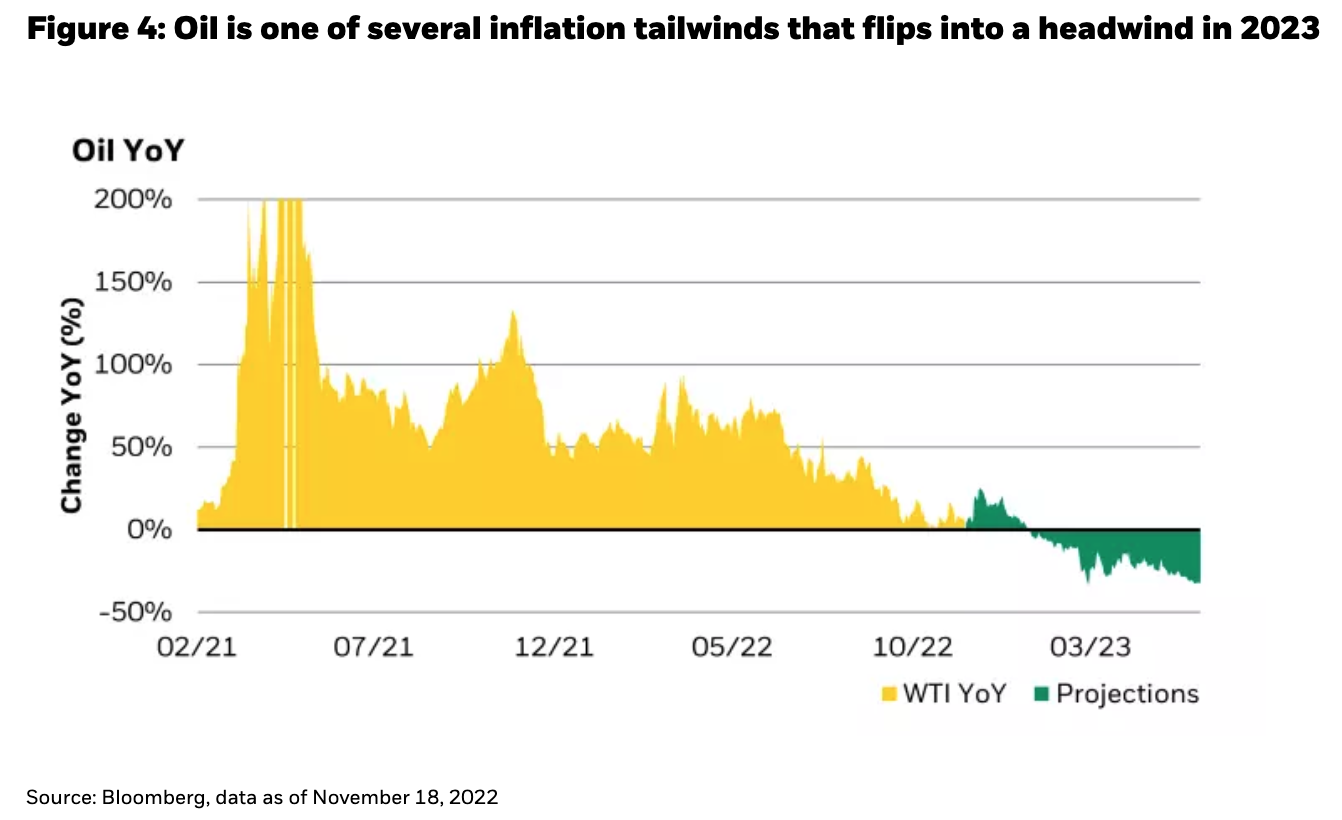

The Fed’s interest rate and liquidity tools are blunt instruments, particularly in a service-oriented economy. Today, those instruments are being used to combat inflation, but there are clear signs of inflation slowing, even beyond the trickle lower in hard inflation data over the last few months. Besides food and used car prices, which are easing from war and supply-chain-driven spikes, respectively, raw material inputs (like oil) are soon going to become a deflationary impulse, weighing on every other secondary and tertiary product down the value chain. By simply staying put at $80 a barrel, a double-digit annual oil inflation rate in 2022 becomes a double-digit deflation rate in 2023, as base effects catch up (see Figure 4). Applying the same logic to other components in the consumption basket ex-shelter (simply extrapolating recent price trends) would result in a material slowdown in headline inflation to between 4% and 5% by the end of 2023, and with some modest price depreciation, perhaps even to between 2% and 3%.

Shelter, the largest component in the consumption basket, is showing even more evidence of moderating, after a torrid run. New and existing home sales transaction volumes have dried up to almost the pandemic-era lows of early-2020, confirming what leading indicators of house prices, and rental rates, are suggesting: that a correction is in motion. Nonetheless, the scarce inventory of existing homes, which is near its lowest level in 40 years, should place a floor under prices and prevent them going into freefall.

Hence, it is plausible that the economy does not need to be engineered into a housing-bust-style recession to slow inflation. In fact, the labor market doesn’t suggest a recession is imminent. While it is slowing at the margin (most notably through a variety of employment PMI surveys), looking at hard data like payrolls, layoffs, hires and jobless claims through a zoomed-out lens is encouraging, as all are in strong multi-decade positions, even if they aren’t at the record levels of late-2021 and early-2022. So, what does this mean for financial assets and where we are on the discount rate mountain?

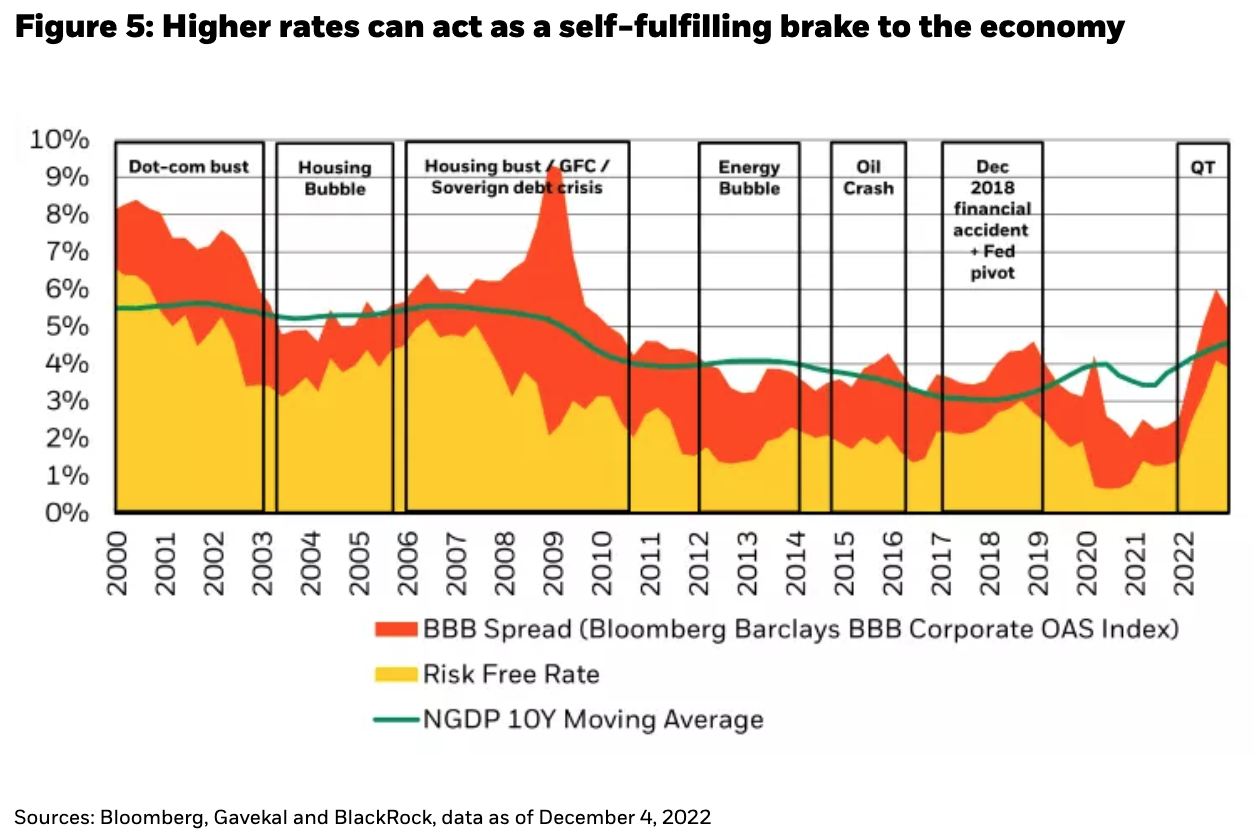

When the marginal borrowing cost to risky borrowers rises too far above the natural growth rate of the economy it acts as a self-fulfilling brake, as borrowing costs exceed future cash flows, disincentivizing new projects (see Figure 5). The opposite is also true – when borrowing costs are too low, they induce a bubble, as projects with sub-par cash flows end up getting funded. Today, the marginal risky borrowing rate has gone from the lowest it’s been relative to long-run nominal GDP, to the highest it’s been relative to long-run nominal GDP, in just a matter of one year. In other words, it is now a lender’s market.

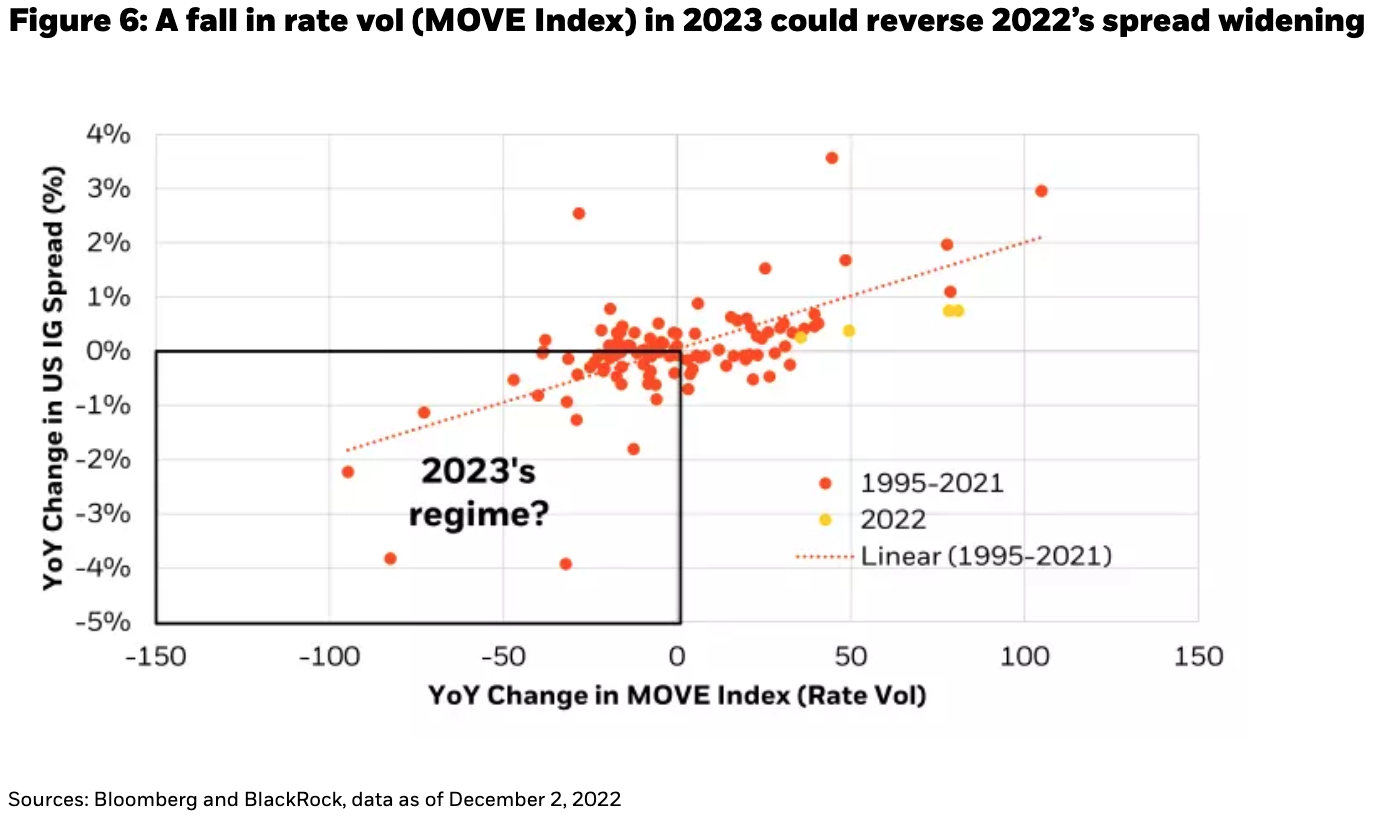

If inflation indeed moderates from here, it is likely that interest rate volatility moderates alongside it, since it is the uncertainty around the peak in inflation that has driven the uncertainty around the peak in interest rates. Central banks may not necessarily lower interest rates; but simply holding them stable for a while would already be a dramatic departure from the pattern of 2022. This leaves fixed income yields in a unique position – risky spreads have responded negatively to a rise in rate volatility, in a rare moment when rate volatility has risen because rates themselves have exploded higher (see Figure 6).

This may set up for a unique, “double-barreled” return environment sometime in the future should rate vol normalize. Risky asset returns may be boosted by both the excess return and rate return component – and at the very least by being able to clip a stable (and high) coupon.

In many respects upside inflation surprises from today’s yield levels, while resulting in short term losses, would potentially deliver an even larger opportunity set for investors that are able and willing to zoom out and widen their “camera aperture” to a 2-year time horizon. The Fed has indeed communicated this year that it is willing to tighten policy more. With a still-moving Fed, investors must worry about financial conditions tightening even further. Yet if the Fed tightens further, then the self-fulfilling economic brake kicks in harder – capital expenditures slow and debt burdens become even more burdensome, leading to less room for fiscal stimulus, higher mortgage rates, and lower consumption. Arguably, this may create an even better opportunity set in fixed income going forward, by establishing an even higher peak to the discount rate mountain, and even more runway to coast down on the other side.

Follow Rick Rieder on Twitter

At generational inflection points like these, it is worth looking at public markets through a private market lens, which often has a wider aperture (longer time horizon) that may be more appropriate for taking on slopes at these heights, rather than the microscope that public market investors usually use to manage daily, weekly and monthly events. What if we looked at the front-end of the U.S. Treasury market through the lens of a 2-year lockup? The 2021 vintage would look awful, but today’s yield looks extremely attractive for forward 2-year returns (see Figure 7).

Including some rolldown, it’s hard to ignore a potential 6% return, two years in a row, in a risk-free asset. The opportunity cost of putting cash into an investment other than the risk-free rate must surely be a consideration for many investors now, especially if it is lower rate volatility that is the predominant catalyst for returns in said other investment. Across major asset classes, the yield contribution from the risk-free rate has doubled from an average of under 2% from 2014 to 2022, to greater than 4% today.

That means that a diversified basket of high-quality fixed income (such as short-term U.S. Treasuries and Investment-Grade corporate bonds, or IG) can potentially deliver an even higher total return. Moving out the curve into 10-year IG bonds, and adding riskier instruments, like European high yield, Collateralized Loan Obligations (CLOs), Emerging Market (EM) bonds, and equities to the mix can bump up the yield of that portfolio, but not by much. However, the volatility of this higher yielding portfolio would have increased substantially, suggesting a vastly inferior risk-adjusted-return profile, in our estimation. The implications of this cannot be understated – it means that investors, especially pension and endowment funds, can get close to their return targets for the next few years without having to take much duration, credit, convexity or illiquidity risk. Portfolio risk budgets can be used far more efficiently than at any time in the last 15 years.

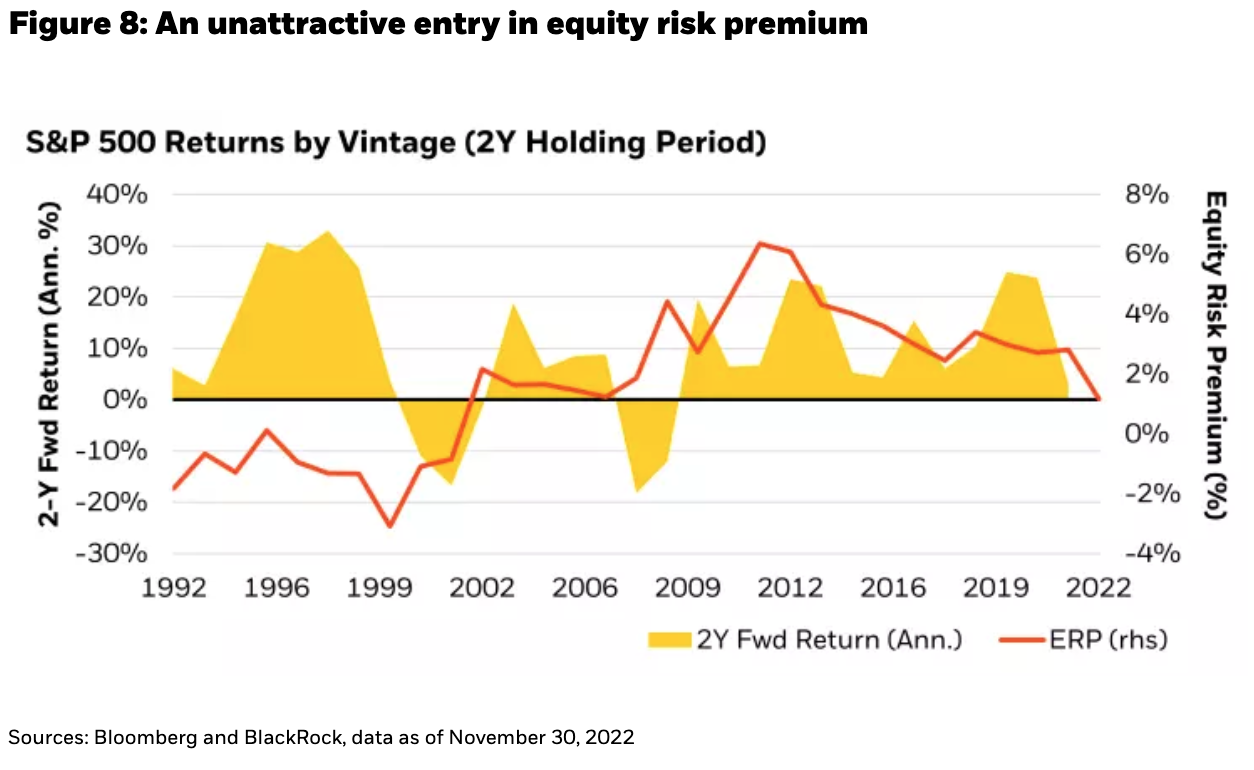

Going even further down the capital stack, the asset allocation opportunity looks quite different. While spreads in fixed income have widened in sympathy with heightened rate volatility, the equity risk premium has compressed, leaving equities looking as unattractive to fixed income as they have in more than a decade (see Figure 8). That is not to say that equities will not deliver positive returns should interest rate volatility decline (such a rising tide could indeed float all boats), but that the excess return over U.S. Treasuries that one might receive in equities is unlikely to be worth the risk (and potential negative returns) of being wrong.

Our sense is that the carry regime in fixed income is much better than in equities; and that the financial asset regime will be better in 2023 than in 2022, albeit with some aftershocks of volatility after 2022’s earthquake. Indeed, the future of Japan’s yield curve control continues to be the “1,000 trillion-yen elephant in the room” that could produce another bout of central bank-induced volatility in 2023. That alone may be an earthquake in fixed income worthy of its own spillovers and aftershocks, especially in currency markets.

Nonetheless, actively managing around asset dispersion is becoming increasingly critical.

Monetary policy has created the asset-on/asset-off framework, which we have grown accustomed to since the global financial crisis. Yet our sense is that policy volatility, and consequently rate volatility (and currency volatility) should all come down from here. Hence, we like owning more financial assets in 2023 than we did entering 2022, but we are being particularly selective about which ones.

While investors need to zoom out and widen their apertures to correctly identify where and when the discount rate mountain peaks, and how to navigate the slopes that follow, we also think it’s vital to simultaneously slide balance sheets and income statements under our microscopes. In a world where dispersion drives return (see Figure 9), investors who cannot manage their full suite of optical tools risk falling down the mountain in 2023. In a separate Market Insights commentary, our “Christmas Shopping List and 2023 Prognostications,” we identify the specific markets we like in this new world of greater dispersion.