by Brian Levitt, Global Market Strategist, Invesco

Key takeaways

|

The contraction continues From a tactical perspective, we still favour a more modest risk profile and a more defensive posture in the near term. |

Halt the hyperbole The airwaves are filled with doomsayers, but I lean more toward near-term realism and intermediate-term optimism. |

Fed flashback

In 1980, the U.S. Federal Reserve began restoring credibility and driving inflation expectations lower. That sounds relevant to our situation today. |

One thing we can’t scratch off of our lists just yet? Inflation. Since we’re constantly being reminded by the media that the inflation data is the worst in 40 years, this month’s column will have a 1970s/early 1980s theme. Admittedly, I was only 4 years old in 1980, but I have read extensively about that period in textbooks. Also, I was once in an elevator with Paul Volcker. So, in the words of Carl Spackler from the 1980 film Caddyshack, “I have that going for me, which is nice.”

A ‘keep it simple’ strategy

We start with the three critical questions that can help us gauge the potential impact on markets. How would I answer these questions this month? With 1970s song lyrics, of course.

1) Where are we in the cycle?

Bob Seger (1978): I know it’s late. I know you’re weary.

Inflation is still elevated,1 and the U.S. Federal Reserve (Fed) is committed to tightening conditions until it falls. The risks to the cycle are elevated.

2) What’s the direction of the economy?

Foghat (1975): Slow ride …

… into a contraction. Our proprietary leading indicators suggest that the economy is in contraction with growth expected to be below trend and falling.2

3) What will be the policy response?

Steely Dan (1972): You go back, Jack, do it again.

Just swap out “Jack” for “Jay” as Fed Chair Jay Powell does it again with interest rate hikes. Inflation appears to be peaking3 but remains too high for the Fed’s comfort. Policy uncertainty persists until inflationary pressures ease.

The upshot is the same as last month: From a tactical perspective, we would still favour a more modest risk profile and a more defensive posture in the near term. This includes quality bonds and businesses that can potentially generate cash flow and growth in a slowing environment.

The national conversation

I think we have a hyperbole problem. Does every economic and/or financial challenge need to be the next crash? It’s like everyone on social media has become Redd Foxx in Sanford & Son, clutching their chest and proclaiming that “This is the big one!”

Select high-profile strategists, many of them perennial doomsayers, are now calling for the bursting of a massive bubble. One notable strategist is warning of an “epic finale market crash.” For what it’s worth, the same strategist warned of “7 lean years” around the time of the 2009 market bottom. I admit, the pessimists do always sound smart. Although historically it’s been the optimists who have made money.4

The hyperbole works both ways. I have an email in my inbox now from a noted strategist predicting a large market rally ahead as inflation plunges. I respect the optimism. I too am an intermediate-term optimist, with intermediate-term being defined as the next 6 to 24 months. However, inflation “plunging” sounds too hopeful. In my view, inflation should come down eventually, but a quick fix is unlikely.

The answer, as is often the case, is probably somewhere in the middle. Although, my near-term realism and intermediate-term optimism isn’t nearly as attention-grabbing as Fred Sanford’s classic catchphrase.

Song of the month

Sticking with the motif, I’ll choose the 1982 hit “One Thing Leads to Another” by The Fixx. In two years, the world has transitioned from a pandemic and unprecedented economic shutdown to an inflationary environment and policy tightening — and a recession is likely next.

It’s clear that the Fed will “do what they say and say what they mean” as they try to get inflation under control. The question now is whether we will ultimately have to be “Saved by Zero”— that is, return to significantly easier monetary policy. The market is already expecting the Fed to be easing policy again by the middle of next year. One thing leads to another.

It was said

“…at some point in the tightening cycle, the risks become more two-sided.” – Lael Brainard, Vice Chair of the U.S. Federal Reserve

I promise to not have the quote of the month always come from a member of the Fed Open Mouth, err, Federal Open Market Committee. For right now though, the Fed is the only game in town. Brainard’s comments provide hope. The Fed wants to slow growth, but not crush it. If the Fed truly believes that the risks are soon to become more two-sided, then the downside risk to the market is limited and the tail risk is less fat. Unfortunately, what the Fed wants to do may be different than what they are forced to do.

Since you asked

What year does 2022 remind you of? Investors seem to have settled on two options: 1973 and 1980. Good choices as investors in those years (and the ones in between them) had to grapple with inflation.

My final answer is B: 1980. In 1973, the Fed had lost control of long-term inflation expectations, setting the stage for a prolonged difficult period for risk taking. In 1980, the Fed began restoring credibility and driving inflation expectations lower. That sounds more relevant to our situation today.5 Yes, there was a recession in 1981,6 but investors who allocated capital to the equity market when inflation peaked in 1980 were rewarded over the short-, intermediate-, and long-term time periods.7

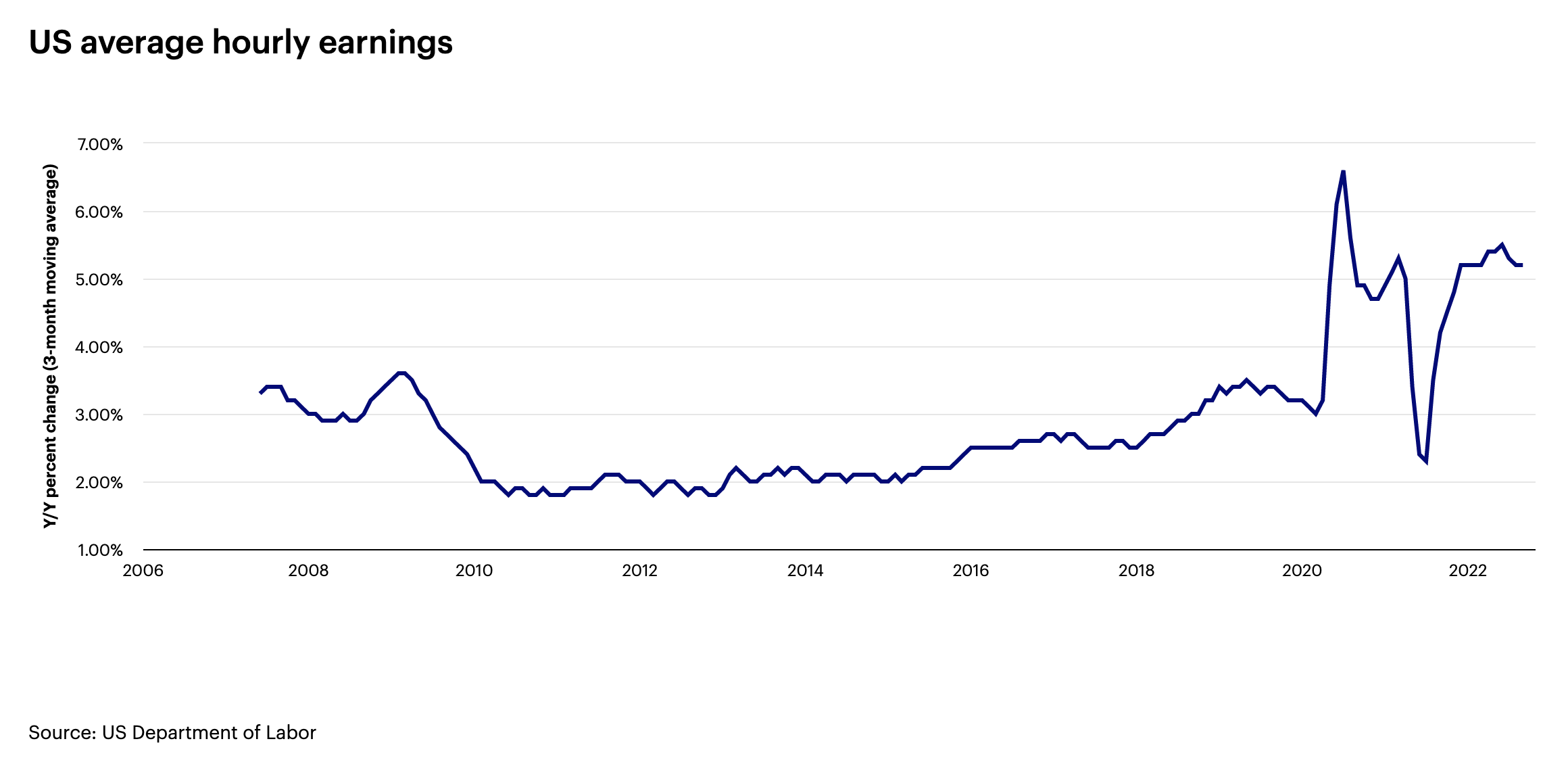

It may be confirmation bias, but …

… wages appear to have peaked, which may help the Fed in its efforts to control inflation.

Phone a friend

Over the past month, I’ve been asked numerous times about the so-called “crypto winter.” Why isn’t crypto performing well in today’s high-inflation environment? I phoned my colleague Ashley Oerth, Senior Investment Strategy Analyst at Invesco, for thoughts. Her response:

“Crypto winter” seems to be describing a consistent downtrend in crypto prices rather than a total fade-to-the-background of the space. I’d characterize what is happening in the crypto space more by what is happening in broader markets. Cryptocurrencies used to be viewed—and traded—as uncorrelated assets, but these days cryptos tend to trade alongside cyclical, risk-on assets like equities. I find it’s helpful to think about cryptos as macro assets: They usually are valued not by their own characteristics but by the prevailing macro environment. So excess liquidity, low rates, and expanding personal incomes are usually good factors, and the opposite are bad omens. With that said, “next summer” for crypto is probably when we see peak hawkishness from central banks and a start to easing policy. To the extent that you’re a believer in crypto’s long-term potential, now may be a buying opportunity — if you can stomach the volatility.”

Seasonal angst

Neil Diamond released “September Morn” in 1979. Maybe it should have been called September Mourn. Over the past 120 years, September has been the worst month of the year for stocks, both on average and median.8 As we go to print, we may be poised for another down September.9 The media is making certain to remind us of this fact.

Is there a rational explanation for this seasonal pattern or is it just a statistical anomaly? It’s largely the case of a few bad Septembers (1929, 1930, 1931, 1933, 1937, 1974, 2001, 2002, 2008) spoiling the month’s reputation.9 The Great Depression, 9/11, and Lehman Brothers skew the data. But in fact, since 1957, the S&P 500 Index has experienced positive September returns in half of the years.9

On the road again

My travels this month took me to Saratoga, New York, for a day with investment professionals at the racetrack. Do I gamble? In the words of Lieutenant Frank Drebin of Police Squad, “Every time I order out.” I don’t usually bet on horses, or anything else that I know nothing about. This time, however, I was with a few folks who knew a thing or two. The pedigrees, the experience of the jockeys, the condition of the track, the willingness of the owners to bend the rules, etc. It was fascinating to watch investment managers, with their newfound wisdoms, engulf themselves into picking horses as if they were looking for the next great stock or bond. As for me, let’s just say that our experts had some good insights. I’m not retiring on it, or even taking my family to dinner on it, but it beats losing.

See you in October.

Footnotes

1 Source: U.S. Bureau of Labor Statistics, 8/31/22. As represented by the Consumer Price Index.

2 Source: Invesco, 8/31/22.

3 Source: U.S. Bureau of Labor Statistics, 8/31/22. As represented by the Consumer Price Index.

4 Source: Bloomberg, L.P. $10,000 invested in the Dow Jones Industrial Average in 1900 would have grown to $5,139,072 as of Dec. 31, 2021. An investment cannot be made directly in an index. Past performance does not guarantee future results.

5 Source: Bloomberg, 9/16/22. Inflation expectations are based on breakevens in the U.S. Treasury market. The breakeven inflation rate is calculated by subtracting the yield of an inflation-protected bond from the yield of a nominal bond during the same period.

6 Source: National Bureau of Economic Research

7 Source: Bloomberg. As represented by the S&P 500 Index. S&P 500 Cumulative Returns from 3/31/80 forward were as follows: 1-year: 40.1%, 5-year: 127.1%, and 10-year: 409.5%. Indices cannot be purchased directly by investors. Past performance does not guarantee future results.

8 Source: Bloomberg, 8/31/22. As represented by the Dow Jones Industrial Average. Indices cannot be purchased directly by investors. Past performance does not guarantee future results.

9 Source: Bloomberg. As represented by the S&P 500 Index.