by William Smead, Smead Capital Management

Dear fellow investors,

To be, or not to be: that is the question:

Whether ’tis nobler in the mind to suffer

The slings and arrows of outrageous fortune,

Or to take arms against a sea of troubles

—William Shakespeare

We believe one of the hardest things to do in common stock investing is to hold winners for a long time. This is especially true with what are normally cyclical industries. In our view, we are suffering through the “slings and arrows” of a major price correction in the secular oil bull market that started in the spring of 2020. Is this the end of oil driving the inflation problem, which has led the Federal Reserve Board into a major tightening cycle? Is this the shortest bear market to cure a financial euphoria episode in history, and should we all go back to nothing but FAANG stocks?

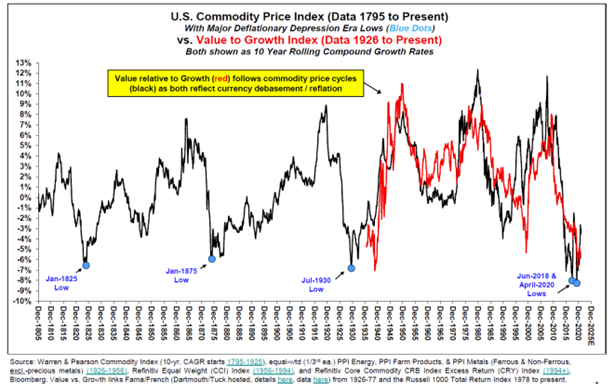

A review of how we got here is necessary. First, we saw this 250-year price chart that showed that the next commodity bull market was going to be a doozy:

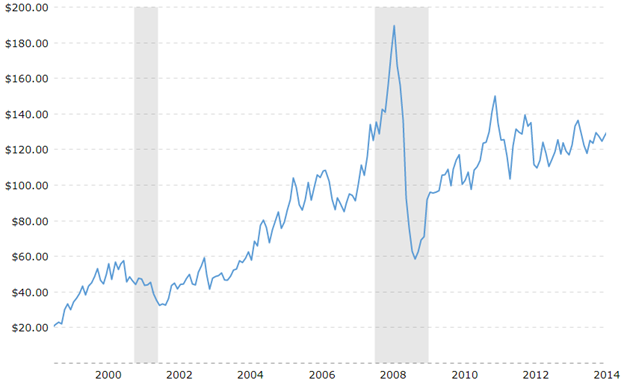

Second, we were reminded of the length of prior oil bull markets in the 1970s and from 1999 through 2014:

Source: macrotrends.com

Source: macrotrends.com

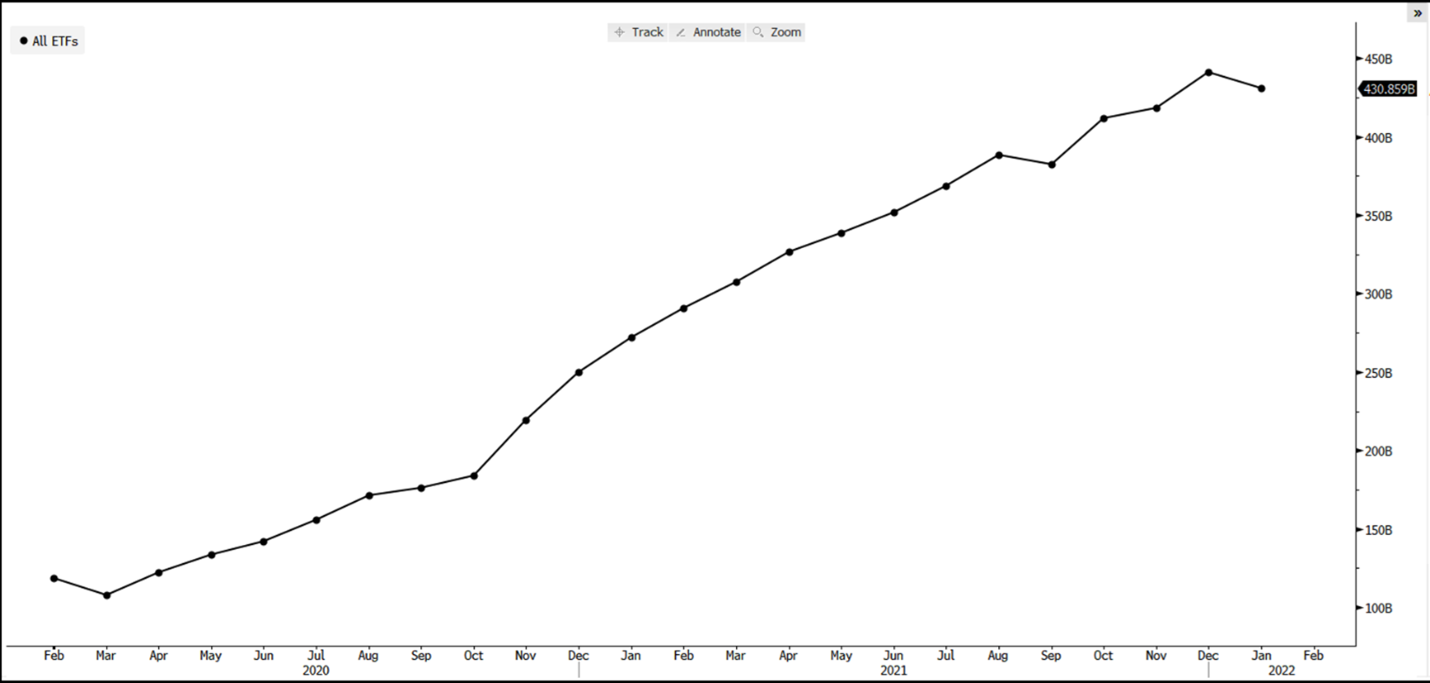

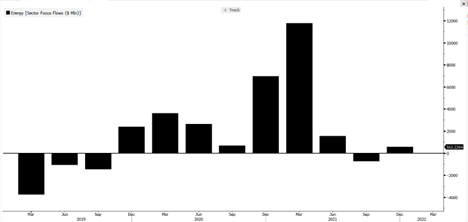

Third, we knew how much had been invested in ESG funds and ETFs versus oil and gas funds and ETFs in 2019-2021:

With these historical underpinnings, we felt compelled to invest in the oil and gas business in 2020-2022. This decision has been a ticket to “outrageous fortune” until the recent sharp correction spooked investors. The sharp oil price decline has combined with a drop in the 10-year Treasury bond interest rate to restimulate the large-cap tech trade which had dominated the stock market for ten years.

Our outrageous fortune in oil started with losing money on Occidental Petroleum (OXY) and buying Chevron (CVX). We then tax-loss sold OXY at around $15-17 per share and bought more CVX at around $80 per share average price. Ironically, it has been our least successful investment in oil with a move from $80 per share to the current level of $150 per share (plus copious dividends). Continental Resources (CLR) share price started in the teens in mid-2020 and today faces a going-private offer of $70 per share from the founder, Harold Hamm. ConocoPhillips (COP) looked attractive in the $30 per share area and has provided dividends and corrected to around $90 per share.

Finally, we invested in Occidental Petroleum in the fall of 2021 starting at around $25 per share after getting clobbered on it on the way down in 2019 into the COVID-19 bear market of 2020.

Therefore, why are we willing to “take arms against a sea of troubles” in a major correction in the oil price and in oil stock prices? The answer lies in the evidence. Obviously, we are keeping very good company in the oil patch. Peter Lynch, Sam Zell, Jerry Jones, Harold Hamm and Warren Buffett/Charlie Munger have backed up the truck over the last three years in the oil and gas patch. As we have said many times, “The only thing better than being smart is knowing who is!” As Munger says, “Plagiarism is completely acceptable in the investment business.”

Next is the body politic. The Senate of the U.S. just passed a major bill to subsidize clean energy. The best way to expedite a faster transition to cleaner energy is to drive the price of fossil fuels to the roof. We will not be shocked if the 2008 high of $150 per barrel gets knocked out in this secular cycle.

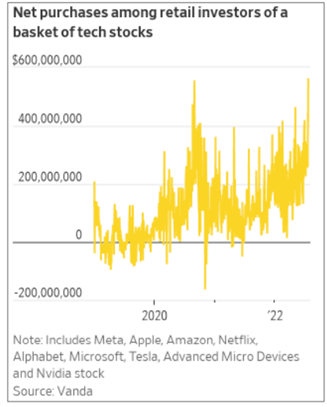

Additionally, the chart below shows that the retail investor enthusiasm for all things FAANG and tech have reemerged in this bear market rally:

Lastly, the sheer force of the returns these oil companies could make with prices exceeding $80 per barrel for a decade makes Warren Buffett’s mouth water. After all, the free cash flow numbers are making debt repayment last for a short time and copious dividends and stock buybacks last much longer. We will “take arms against the sea of troubles” in oil price volatility and the continuation of the bear market in the S&P 500 Index. As always, fear stock market failure.

Warm regards,

William Smead

The information contained in this missive represents Smead Capital Management’s opinions, and should not be construed as personalized or individualized investment advice and are subject to change. Past performance is no guarantee of future results. Bill Smead, CIO, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. Portfolio composition is subject to change at any time and references to specific securities, industries and sectors in this letter are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. In preparing this document, SCM has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. A list of all recommendations made by Smead Capital Management within the past twelve-month period is available upon request.

©2022 Smead Capital Management, Inc. All rights reserved.