by Carl R. Tannenbaum, Ryan James Boyle, Vaibhav Tandon, Northern Trust

The Northern Trust Economics team shares its outlook for growth, inflation and interest rates.

The year to date has brought a series of escalating worries: Will rising energy prices derail the recovery? Will inflation ever calm? Have we entered a recession? While we can address each of those questions on their merits, it was easy to feel overcome by a pervasive sense of fear.

As summer concludes, some of that fearful sentiment is dissipating. Many inflationary drivers are cooling, inventories are recovering, and risk assets are appreciating. A soft landing (lower inflation, steady growth, and minimal job losses) is still possible. However, we see no reason to expect a boom; the recovery is in a delicate position, and our outlook is for low but positive growth in the year to come.

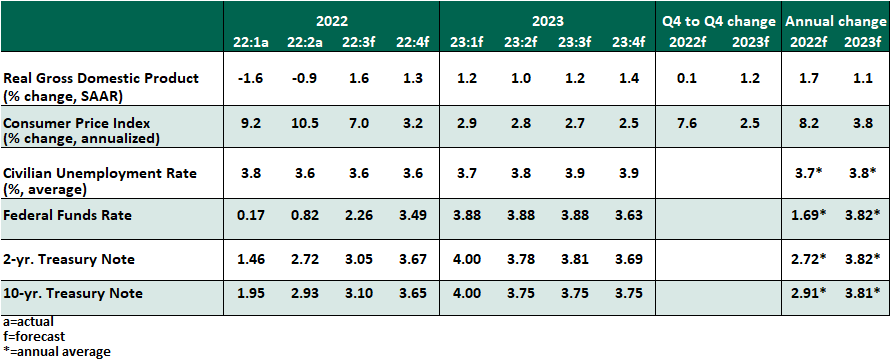

Key Economic Indicators

Influences on the Forecast

- The consumer price index (CPI) for July offered an encouraging signal, as headline inflation was flat month over month, bringing the year over year measure down to 8.5%. As hoped, lower energy costs led the decline. Prices also fell in some sectors that had been especially hot throughout the year, including airfares and used vehicles. However, inflation will remain top of mind: rent has increased 6.3% over the past year, and groceries by 13.1%. One favorable report will not be sufficient to move the Fed off its path of rapid interest rate increases.

- The July employment report revealed job creation continuing at a surprisingly rapid pace of 528,000 additional payrolls. With this gain, total employment has recovered to its pre-pandemic level; the unemployment rate of 3.5% has also returned to its 2020 low. However, labor force participation has ceased its recovery, holding almost a full percentage point below its prior norm. Average hourly earnings increased by 5.2%, maintaining a year-long elevated trend that will remain a persistent inflationary threat.

- Weekly initial unemployment claims are an important barometer of labor market conditions; a rapid elevation can signal a coming recession. From a record low earlier this year, they have risen. Their current level is consistent with readings seen during the strong labor market before the pandemic, but continued increases may be concerning.

- Reacting to high inflation and stable employment, the Federal Open Market Committee raised the Federal Funds rate by another 75 basis points in July, repeating the outsized move it made in June. In comments after the meeting, Chair Jerome Powell offered no forward guidance, insisting that no course is predetermined and all future decisions will be based on real economic results.

- Risk assets rallied following the meeting, as Powell’s remarks opened a possibility that the Fed could slow its path of rate hikes. In subsequent speeches, Federal Reserve governors uniformly pushed back on this narrative. As long as inflation is high, outsized interest rate increases are appropriate.

- We continue to expect large increases in the three meetings remaining in 2022, with the target rate reaching 3.75-4.00% before a pause and potential retreat late in 2023.

- A negative headline reading of real U.S. GDP for the second quarter renewed speculation that the country has entered a recession. Slower inventory accumulation was the primary downward force. Consumer spending continued to grow, but at a slower pace; business fixed investment contracted slightly. While activity and employment remain too strong to consider today’s economy as being in a recession, the interval of rapid rebound has concluded.

- After no significant legislative activity since the bipartisan infrastructure bill was ratified last November, Congress surprised with the passage of two bills.

- The bipartisan Chips and Science Act grants $280 billion to support research and domestic production of semiconductors, funding government research and private investment to address the imbalance in the global market for microchips.

- Senate Democrats agreed upon a reconciliation spending package that will include $433 billion in new spending on clean energy and healthcare. The bill’s new 15% minimum corporate tax rate and lower healthcare expenses will lower the deficit. The measure’s title of the “Inflation Reduction Act” shows that care was taken to minimize the inflationary effect of this new spending.

- These measures will lift investment and support GDP, but gradually and over a horizon of many years.

Copyright © Northern Trust