by Wai Tong, MBA, P.Eng., CFA Equity Analyst, AGF Investments Inc

Global supply chain disruptions may now be gradually abating after several chaotic months of pandemic-induced bottlenecks, but that doesn’t necessarily mean smoother sailing for investors. While a “return to normal” could help alleviate ongoing inflationary pressures – and temper the extent of central bank interest rate hikes in the process – the impact of normalization won’t be equally felt across equity markets and some segments of them are bound to benefit more than others. As an example, Industrials stocks may be in for one of the bigger shake ups if supply chains right themselves, leaving those invested in the sector re-thinking their current exposure.

Why Disruptions May Be Easing

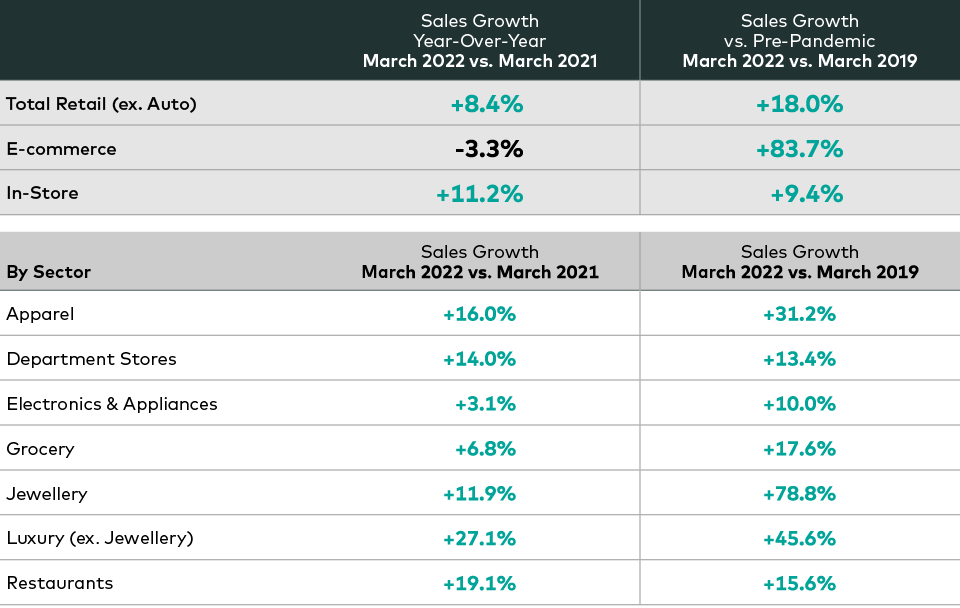

Several factors suggest supply chain disruptions are easing and will likely continue to do so going forward. First and foremost is the growing shift in consumer spending from goods to services, which could help correct the demand and supply imbalance of the former. Although e-commerce sales were up 83.7% in March 2022 from their level during the same month in 2019, they declined 3.3% from this time last year, according to Mastercard data, marking the first such decrease since the beginning of the COVID-19 pandemic. Meanwhile, spending in restaurants was one of the stronger categories on a month-over-month basis, finally eclipsing pre-pandemic levels.

Retail Sales Growth

Source: Mastercard SpendingPlus, which measures in-store and online retail sales across all forms of payment. Data as of April 6, 2022

Another reason to believe supply chain disruptions could be abating is related to inventories, which have reset higher following the double-ordering phenomenon that took place during peak season last year. Economic activity in the services sector grew in March this year for the 22nd consecutive month, with the Purchasing Manager Index (PMI) for services in the United States, increasing to 58.3 in March, according to the latest ISM Report on Business. U.S. business inventories, meanwhile, were up 12.5% year-over-year in February, according to statistics from the U.S. Commerce Department.

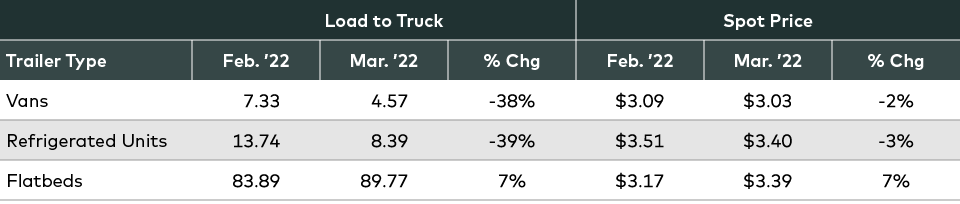

The impact of these trends can be seen in the decline of ex-fuel spot rates in truckload (TL) prices, which are one-time fees for shipping freight at current market pricing. Less-than truckload (LTL) pricing (i.e. freight that does not require the entire space of a truck) is holding up for now, but will likely come under pressure in the months ahead as demand weakens and higher supply comes online because of the potential of an improved jobs market. In fact, many companies across several sectors have already highlighted improvement in labour supply. Inflation headwinds impacting consumers in the lower income brackets (especially for food and fuel) will likely further exacerbate this slowing demand trend for goods.

Spot Trucking Prices

Source: DAT Solutions LLC, as of April 8, 2022. Load to truck measures the number of loads on the market and the numbers of trucks available to carry those loads.

In the meantime, U.S. factory output in March exceeded expectations as businesses continue to invest despite the recent spike in geopolitical risks and economic uncertainty. Capacity utilization rose to 78.7% in March from 78.1% the previous month, and up almost 18% from the April 2020 lows, according to statistics from the U.S. Federal Reserve (Fed). This shows manufacturers are having more success filling open positions and the supply chain situation is improving. Manufacturing output saw broad-based increases, growing at an annual rate of 5.4% in the first quarter of 2022, and included a 7.8% surge in the production of motor vehicles, again, according to the Fed. Auto production rose to an annualized 9.75 million units, the highest since January 2021.

Ultimately, these manufacturing production numbers, combined with the decline in consumer demand for goods, could mean we are near the peak of upward pressure on inflation coming from supply chain issues. In fact, these pressures should moderate as transportation costs decline entering the second half of 2022. Higher manufacturing production has historically led to lower pricing for some goods.

Implications for Investors

All of that is bound to have implications for the broader economy, and equity markets more specifically. For one, the Fed may not need to raise rates as aggressively as expected to combat inflation. And while recession risks are building given tightening monetary policy, geopolitical-related inflation shocks and other factors, supply chain constraints this cycle prevented the build-up of large excess inventories, as was the case in prior recessions. In turn, a recession is still possible, yet it could be shallower than prior recessions because there is more inventory to consume before production once again normalizes this time around.

When it comes to stocks, meanwhile, several sectors could be impacted, but perhaps none more so than Industrials. The recent decline in goods has already led to a decline in spot trucking prices. The contract price for trucking (i.e. longer term pricing agreements) has a 91% correlation to spot trucking prices, with an eight-to-nine month lag, according to Truckstop.com.

As such, the transport subsector in Industrials will likely be hard hit. The latest data from ACT Research for April 2022 already showed Class 8 truck orders are down 26% month-over-month and 53% year-over-year.

Supply Chain Normalization

Source: JPM Research, as of April 8, 2022.

Still, as congestion fades, supply chains normalize and freight demand weakens, not every transport stock will suffer equally – and the group will be defined by potential winners as much as it is potential losers. Truck brokers could do relatively well, for example, as truckers pay them to find volumes of goods to move. The rails are also potential winners since they have an inherent cost advantage versus truck transport, especially with the current high prices for fuel.

Of course, as noted, the biggest losers will be the truckload truckers, whose labour and fuel costs will likely increase just as the price they can charge for their services decline. The truckload market is especially fragmented, and the players will not be able to maintain price discipline.

In other words, while consumers, manufacturers and retailers will most likely benefit from lower transportation costs, it’s much more nuanced whether the transportation subsector of Industrials will or not.

The views expressed in this blog are those of the author(s) and do not necessarily represent the opinions of AGF, its subsidiaries or any of its affiliated companies, funds, or investment strategies.

The commentaries contained herein are provided as a general source of information based on information available as of May 16, 2022 and are not intended to be comprehensive investment advice applicable to the circumstances of the individual. Every effort has been made to ensure accuracy in these commentaries at the time of publication, however, accuracy cannot be guaranteed. Market conditions may change and AGF Investments accepts no responsibility for individual investment decisions arising from the use or reliance on the information contained here.

AGF Investments is a group of wholly owned subsidiaries of AGF Management Limited, a Canadian reporting issuer. The subsidiaries included in AGF Investments are AGF Investments Inc. (AGFI), AGF Investments America Inc. (AGFA), AGF Investments LLC (AGFUS) and AGF International Advisors Company Limited (AGFIA). AGFA and AGFUS are registered advisors in the U.S. AGFI is registered as a portfolio manager across Canadian securities commissions. AGFIA is regulated by the Central Bank of Ireland and registered with the Australian Securities & Investments Commission. The subsidiaries that form AGF Investments manage a variety of mandates comprised of equity, fixed income and balanced assets.

® The “AGF” logo is a registered trademark of AGF Management Limited and used under licence.