by Vaibhav Tandon, Senior Economist, Northern Trust

When life gives you lemons: sell them! In India, prices of lemons have more than quadrupled from ₹75/kg ($1) to record highs of ₹350/kg ($4.50) in just a matter of weeks. This has left Indians with a sour taste, but the cost of a glass of lemonade is the least of our problems. A range of other important foodstuffs are also becoming dearer, in a country where half the population is living on less than $3.20 a day.

Higher costs of essentials are not confined to India. Short supplies and rising prices for food are reducing the weight of consumer wallets everywhere. The problem started off with the pandemic as a key underlying force, as logistic systems surrounding food distribution were significantly disrupted. While COVID-19 is less of an issue today in most parts of the world, problems in food supply chains have lingered.

The war in Ukraine has also added a massive strain. Moscow is the world’s largest exporter of wheat and fertilizer. Kyiv is the biggest supplier of sunflower seed oil and a significant source of wheat, maize and barley. Sanctions on Russia coupled with port blockades and the damage to railroad infrastructure in Ukraine have brought exports to a standstill. In March, Kyiv could export only a quarter of the grains it supplied in February. To keep domestic prices in check, Russia has suspended sales of fertilizer and grains to other nations. Ukraine has also limited their exports of sunflower oil, wheat, oats and cattle.

The conflict is driving a new wave of protectionism. Desperate to ensure adequate domestic supplies, governments are raising new barriers to exports. A total of 47 export curbs on food and fertilizers have been put in place by various countries this year, according to a professor at the University of St. Gallen. 43 of those 47 restrictions have coincided with the war.

The rules of the World Trade Organization (WTO) allow countries to impose temporary measures for national security or safety. But the restrictions are adding to the global pain. Indonesia, which produces more than half the world’s palm oil, has halted exports. Turkey has halted supplies of a host of food items such as butter, lamb and vegetable oils. Supply of fertilizers from China, a major producer of the commodity, has remained offline since last year to cater to domestic demand.

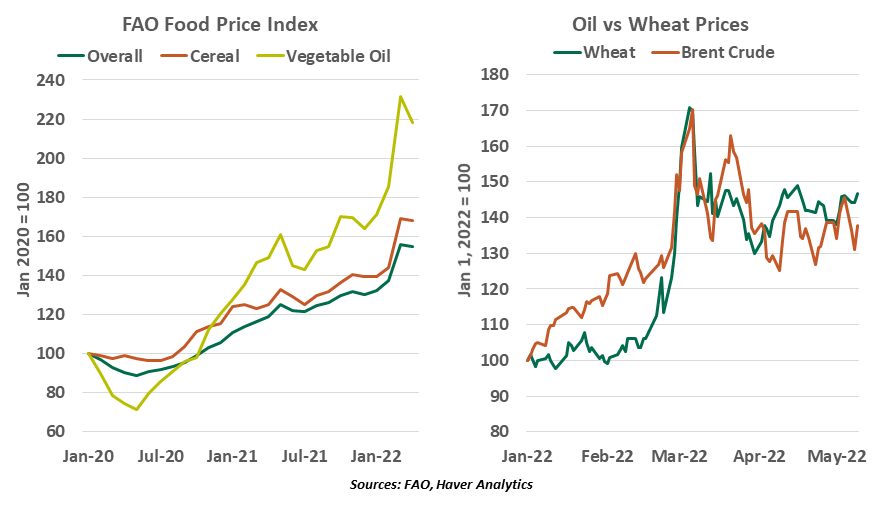

The curbs are making food items less affordable and harder to come by. The Food and Agriculture Organization (FAO) Food Price Index rose to an all-time high in March; the index is up 30% year-over-year in April and 20% since the start of the year. Vegetable oil and cereal have been the biggest contributors. Costs of raw materials like petroleum, ammonia, nitrates and nitrogen are on the rise. This has led to fertilizers and farming becoming more expensive. More worryingly, the price of wheat has surged more than the price of oil this year. This is raising the cost of bread, a staple of most global cuisines.

India is the world’s second largest wheat exporter, and seasonally, the only major supplier at this time of the year. It is filling in some of the supply gap and benefitting from increased exports amid the scramble for alternatives to Ukrainian wheat. But diversifying supplies is not going to be easy, particularly for African nations. About 85% of wheat consumed in Africa comes from abroad, with the bulk of it imported from Russia and Ukraine. Even in India, the gains may not last for long. Wheat is very sensitive to heat, so the current heatwave could lead to lower yields and exports.

COVID-19 led to an increase in poverty; the war could contribute to more starvation.

India’s current weather is a salient example of the risks of climate change. Agricultural regions are facing historic drought and extreme weather conditions. According to the United Nations, droughts have caused global economic losses of over $120 billion between 1998 and 2017. The drag on gross domestic product in India alone was estimated to be 2%-5%.

The world’s poor will bear the greatest burden of the looming food crisis. High-income economies are worried about stagflation, but poorer nations are facing the risk of starvation. Before the war, over 800 million people around the world did not have enough to eat, a number poised to increase.

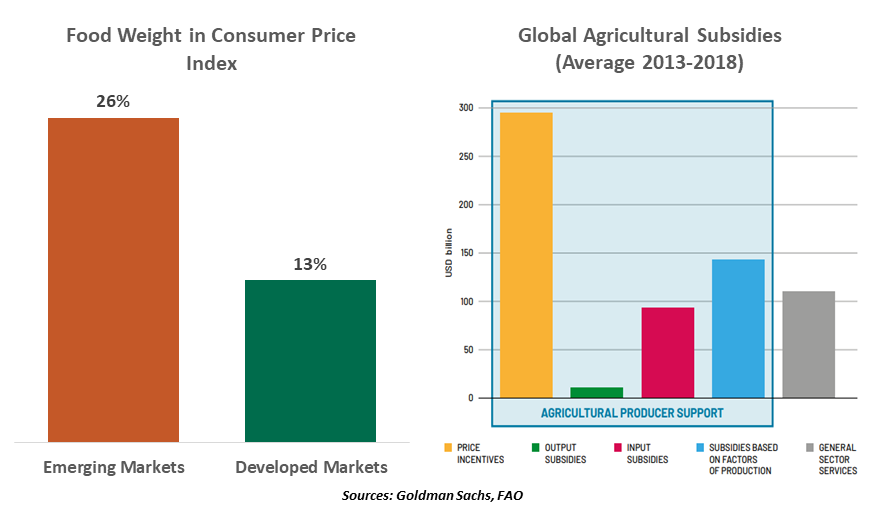

Richer economies and people can deal with higher food prices with relative ease. But edibles represent a much higher share of total consumption in emerging markets. Food is currently contributing 7.1% and 2.8% to headline inflation in Emerging Europe and Latin America (LATAM) respectively, compared to 0.8% in developed economies.

This is creating an environment of food insecurity, often a root cause for riots, famine and migration in low-income economies. Historically, food shortages and higher costs have sparked major uprisings, from the French Revolution to the Arab Spring.

Africa and LATAM are the most exposed areas, where people generally spend as much as half of their income on food. In Asia, Filipinos spent nearly 40% of their money on essentials in 2021. By contrast, an average American family spends less than a tenth of its disposable income on foodstuff.

Developing economies don’t have adequate resources to ensure food security.

Social safety nets have diminished amid the pandemic, and the rising cost of living is creating a clamor for more subsidies. Governments around the world spend $540 billion a year in agriculture support. There is little room to do more. Additional outlays will push governments deeper into debt and widen fiscal deficits. This could lead to debt distress and limit their ability to raise money. And returns would diminish: cash subsidies alone cannot counteract droughts and wars.

Nations and multilateral institutions need to do more to prevent a food crisis. To begin with, the WTO will have to work with countries to prevent further food export bans undermining supplies. Additional contributions will be needed for the World Food Program to help countries in distress. And in the longer run, the global community will have to support weaker economies so they become more resilient to energy, weather, health and geopolitical shocks.

Now if you’ll excuse me, I have lemons to squeeze to make a glass of lemonade. I have to find relief from this scorching heat.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

Vaibhav Tandon

Vaibhav Tandon

Vice President, Economist

Vaibhav Tandon is an Economist within the Global Risk Management division of Northern Trust. In this role, Vaibhav briefs clients and colleagues on the economy and business conditions, supports internal stress testing and capital allocation processes, and publishes the bank's formal economic viewpoint. He publishes weekly economic commentaries and monthly global outlooks.

Copyright © Northern Trust