by Tony DeSpirito, BlackRock Fundamental Active Equity Investment Team, Blackrock

Seeking resilience. 2022 started with rising interest rates, high inflation and unthinkable violence and human tragedy in Europe. Uncertainty is high, investing is more complicated and, we believe, active stock selection is more important. As Q2 begins, we see:

- Opportunity to add to stocks unduly punished in the downturn

- Longer-term potential in value-oriented strategies

- U.S. stocks holding an edge across global asset classes

Market overview and outlook

A confluence of negative factors set U.S. stocks up for a difficult start to 2022, with the S&P 500 recording its worst January since 2009 and officially hitting correction territory (a 10%+ decline) in February. Growth-oriented stocks were at the epicenter of the pain amid fears of rising rates and a slowing economy.

We see both a short- and longer-term opportunity taking shape. In the near-term, we believe indiscriminate selling has created attractive entry points, particularly into some high-growth-potential stocks. At the same time, we believe investors should prepare for a longer-run regime shift as the once familiar slow-growth, low-rate environment transitions to a new world order that may warrant greater selectivity and a rebalance toward value.

The virtues of an active approach to both stock selection and risk management can be most evident at times of significant market disruption

A time for resilience

The investing backdrop is mired in uncertainty. Just as the global economy is looking to emerge from pandemic malaise, a callous war has applied new pressures to a global system that was looking to normalize interest rates and process the effects of the highest inflation seen in decades.

Intraday market volatility has been dramatic and stock selling has become indiscriminate, as is often the case in big market swings. We believe this has opened attractive entry points, particularly into some growth stocks that have been punished beyond what their fundamentals would imply.

The prevailing backdrop highlights the importance of building resilience into portfolios. We believe this is best achieved through diversification and a focus on quality ― particularly stocks of companies with strong balance sheets and healthy free cash flow characteristics.

A new chapter in the investing playbook

Amid the uncertainty, one thing we feel relatively certain about is that we are exiting the investing regime that had reigned since the Global Financial Crisis (GFC) of 2008. That was marked by low to moderate economic growth, alongside low inflation and interest rates. The new environment is still taking shape but will undoubtedly entail higher inflation and rates than we knew from 2008 to 2020.

Stock selection matters more

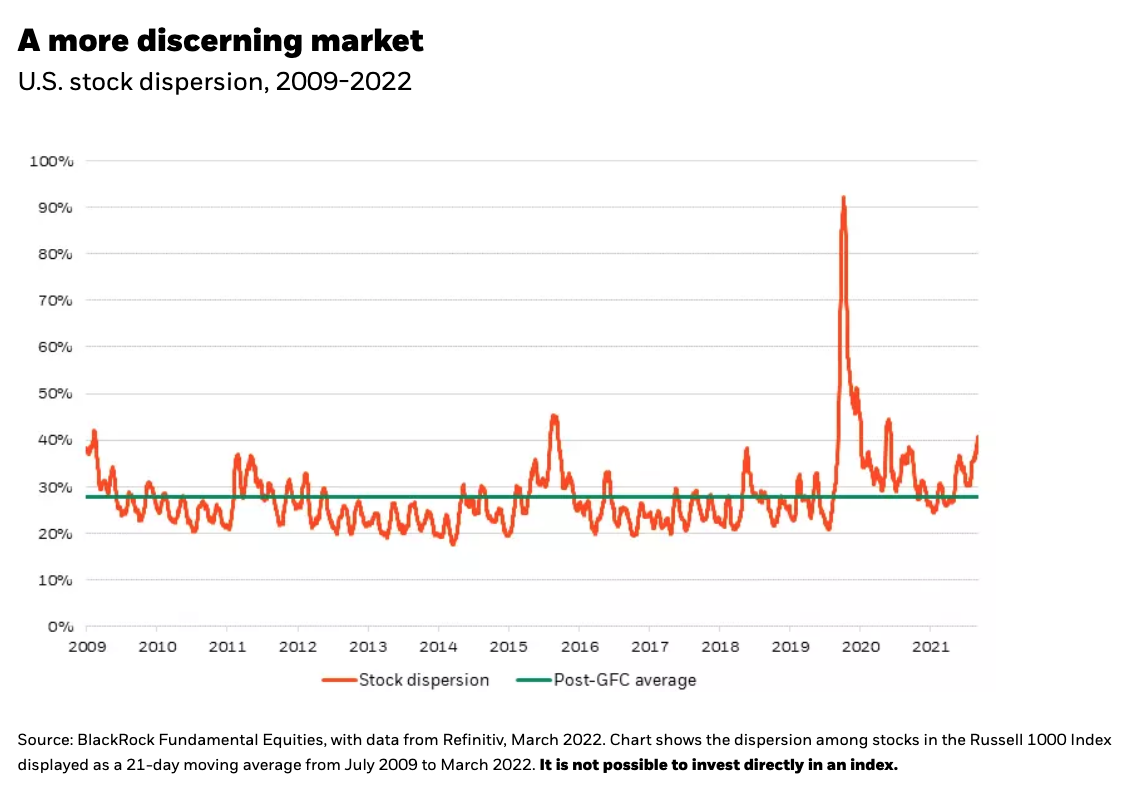

We see stock selection becoming more important as companies navigate higher inflation and rates with varying degrees of agility. Stock dispersion, a measure of the potential risk/return outcomes for individual stocks, already sits well above its average since the GFC, as shown in the chart below.

Higher inflation than the roughly 2% we knew before the pandemic will challenge companies’ cost structures. Investors must discern which companies are most impacted by rising costs, and which have the pricing power to pass those higher costs through to consumers and maintain their profit margins. From there, the question is how much of this is (or is not) reflected in stock prices.

As part of our analysis, we look for companies with unique products or services, durable cost advantages, or that operate in consolidated and rationale industry structures. We think businesses selling labor-saving equipment and technology will benefit as companies seek to offset higher wages. Software solutions and some industrial equipment are two potential beneficiaries.

Value revisited

Inflation has implications for both the overall level of the market and for market internals, particularly the value versus growth debate. Value stocks have dominated so far this year as rising rates weighed on growth stocks. Growth stocks are considered long duration because their cash flows are realized further into the future. Higher rates drag on the present value of these future cash flows. Value stocks, meanwhile, are shorter duration with cash flows that are front-end loaded ― capital is returned to shareholders earlier in the investment lifecycle.

The period of extremely low interest rates was very good for growth stocks ― and very challenging for value investors. The road ahead is likely to be different, restoring some of the appeal of a value strategy.

A time for active decision-making

Times of uncertainty can test investors’ fortitude. We believe these are the moments when active, fundamental-based stock selection and thoughtful portfolio construction can provide a measure of solace and have a profound impact in the pursuit of long-term financial goals.

Copyright © Blackrock