by Lance Roberts, RIA

During bull markets, investors have a concise memory of previous bear markets. Such is why, throughout history, cycles repeat as lessons must get learned and relearned.

Such was the topic of a recent article from ARS Technica:

“There’s extensive academic literature on the risks faced by investors who are overly confident of their ability to beat the market. They tend to trade more often, even if they’re losing money doing so. They take on too much debt and don’t diversify their holdings. When the market makes a sudden lurch, they tend to overreact to it. Yet, despite all that evidence, there’s no hard data on what makes investors overconfident in the first place.”

Behavioral finance has spent years digging into investor psychology and the repeated behaviors through market cycles. As you can probably surmise, investors develop few “good” behaviors and are the biggest reason for underperformance over time.

“Behavioral biases that lead to poor investment decision-making is the single largest contributor to underperformance over time. Dalbar defined nine of the irrational investment behavior biases specifically:”

- Loss Aversion

- Narrow Framing

- Anchoring

- Mental Accounting

- Lack of Diversification

- Herding

- Regret

- Media Response

- Optimism

During bull market advances, “herding,” “lack of diversification,” and “anchoring” are the most common problems. These behaviors tend to function together and compound investor mistakes. As noted previously:

“Bull markets hide investment mistakes. Bear markets expose them.”

Short Memory But Long Market Cycles

There are few things in this world you can ABSOLUTELY count on;

- Death

- Taxes

- Day Turning Into Night

- Seasons

- Market Cycles

Without fail, bull markets have turned into bear markets throughout history, as shown.

These cycles all contained the same psychological traits. Investors chanted during the bull phase, “this time is different.” During the bear phase, the belief was it would never end. In other words, the “Fear Of Missing Out (FOMO)” always reverted to the “Fear Of Being In (FOBI)” and vice-versa.

What is most interesting about investor psychology is that once a new “bull cycle” engages, the “pain” of the previous “bear cycle” gets forgotten. While a “baby boomer” vividly remembers the losses incurred in 2000 and 2008, the bull market eventually displaces “fear” with “greed.”

“Generation Z,” born between 1995 and 2005, was between the ages of 6 and 16 during the “Financial Crisis.” As a result, that generation is the most susceptible to inherent behavioral biases as that generation has never experienced a “bear market” cycle.

As noted previously, bear market cycles are long-lasting affairs, as shown below, which can wreck financial plans when they occur.

The eventual second half of the “full-market cycle” will likely be just as unforgiving.

Selective Memory

“With the cost of going wrong, you’d think that people who risk money in stocks would learn from their past mistakes. But a new study suggests that our memory’s tendency to take an optimistic past gets in the way, with people inflating their gains and forgetting their losses.” – ARS

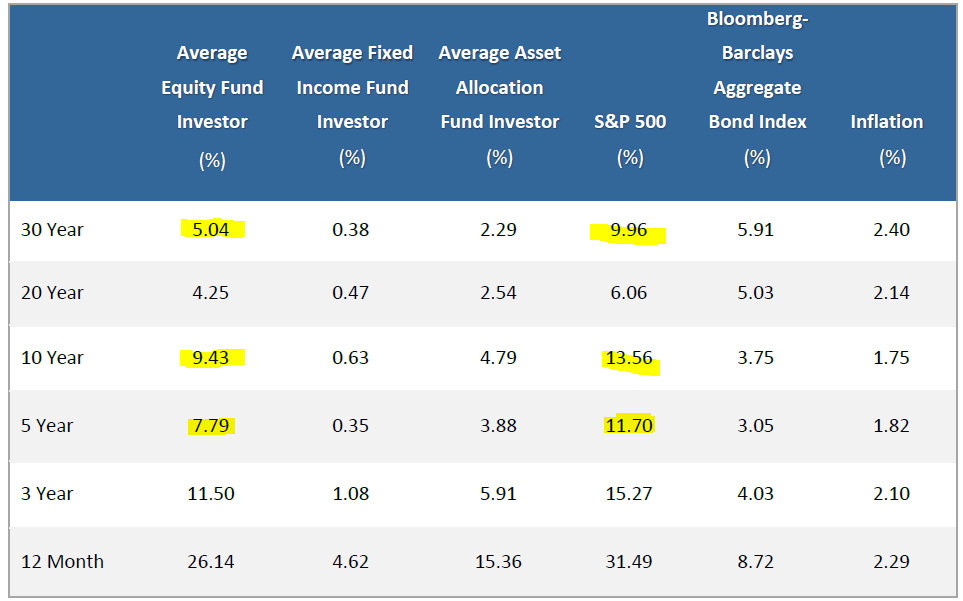

The reality is that most investors do far worse than the market over time. Dalbar publishes research showing the long-term performance of investors relative to the market. The results, not surprisingly, aren’t great.

The entire differential in performance comes down to investing mistakes over time driven by psychology. As Dalbar previously stated:

“No evidence is found to link predictably poor investment recommendations to average investor underperformance. Analysis of the underperformance shows that investor behavior is the number one cause, with fees being the second leading cause.”

Daniel Walters and Philip Fernbach ran a couple of experiments on people who had traded last year. To wit:

“The differences between memory and reality weren’t dramatic, but they were consistent. When asked to recall a trade, the average person in one experiment reported it as yielding a 44 percent profit; reality showed it was 40 percent. When asked for a second, the difference was even wider: 41 percent in memory, 34 percent in reality. In another experiment, participants were asked to write down their 10 biggest trades of the last year. People tended to forget to list losses about 40 percent of the time, while gains only slipped their memories 30 percent of the time.

In all cases, the faulty memories tended to be linked with a higher interest in future trading, along with a greater optimism about the ability to beat the market in the future.”

There is a simplistic cycle worth noting.

“Selective Memory => Over Confidence => Investment Losses.”

Don’t Be A Goldfish

A careful review of your investment strategy, with an honest comparison to actual returns, might be an enlightening exercise to reduce potential risk in your portfolio. As ARS noted:

“In a lot of situations, people are advised not to get hung up on poor past performance. If you search for the phrase ‘don’t dwell on your mistakes,’ you’ll find a large collection of pages advising you to do so, along with a large collection of images of self-help slogans. A variant of the idea—be a goldfish—even made its way into a popular TV show. Maybe it’s time to put an asterisk on it to alert people that it may not apply to investing.”

Many investors in the market currently have already forgotten the “gut-wrenching” plunge in March 2020. That rapid decline was a function of a very illiquid market. It will happen again. The only question is “when.”

Bull Market And Investor Memory

During bull markets, investors have very short memories of painful events. It is part of our genetic makeup.

“After a painful event, most of us find that time eventually eases the pain. But it’s not physical time that causes pain to diminish. Vivid emotional details become less accessible to conscious experience. The edges of memory are smoothed over, and painful memories diminish in intensity.” – Psychology Today

That “smoothing” allows us to move forward with our lives. However, when it comes to investing, we tend to repeat our mistakes by forgetting the past. Some investment guidelines can help mitigate repeating our previous failures.

- Investing is not a competition. There are no prizes for winning but severe penalties for losing.

- Emotions have no place in investing.You are generally better off doing the opposite of what you “feel.”

- The ONLY investments that you can “buy and hold” are those providing an income stream and return of principal.

- Market valuations are very poor market timing devices.

- Fundamentals and Economics drive long-term investment decisions – “Greed and Fear” drive short-term trading.

- “Market timing” is impossible– managing exposure to risk is both logical and possible.

- Investment is about discipline and patience. Lacking either one can be destructive to your investment goals.

- There is no value in daily media commentary– turn off the television and save yourself the mental capital.

- Investing is no different than gambling– both are “guesses” about future outcomes based on probabilities. The winner is the one who knows when to “fold” and when to go “all in”.

- No investment strategy works all the time. The trick is knowing the difference between a bad investment strategy and one that is temporarily out of favor.

“The investor’s chief problem – and even his worst enemy – is likely to be himself.” – Benjamin Graham.