by Lance Roberts, RIA

Last week, we asked if there would be a market correction before “Santa visits Broad and Wall?”

“Investors’ ‘wish lists’ are hung by the chimney with care, hopeful the ‘Santa Claus rally’ will soon be there. While they remain ‘snug in their beds, the historical data dances in the heads.’ The chart below from @themarketear shows the annual “seasonality” from 1985 through 2019.

It certainly seems there is little to worry about. However, notice that dip at the beginning of December.“

We made the case that mutual fund distributions would provide additional selling pressure on a market already plagued by weak internals. To wit:

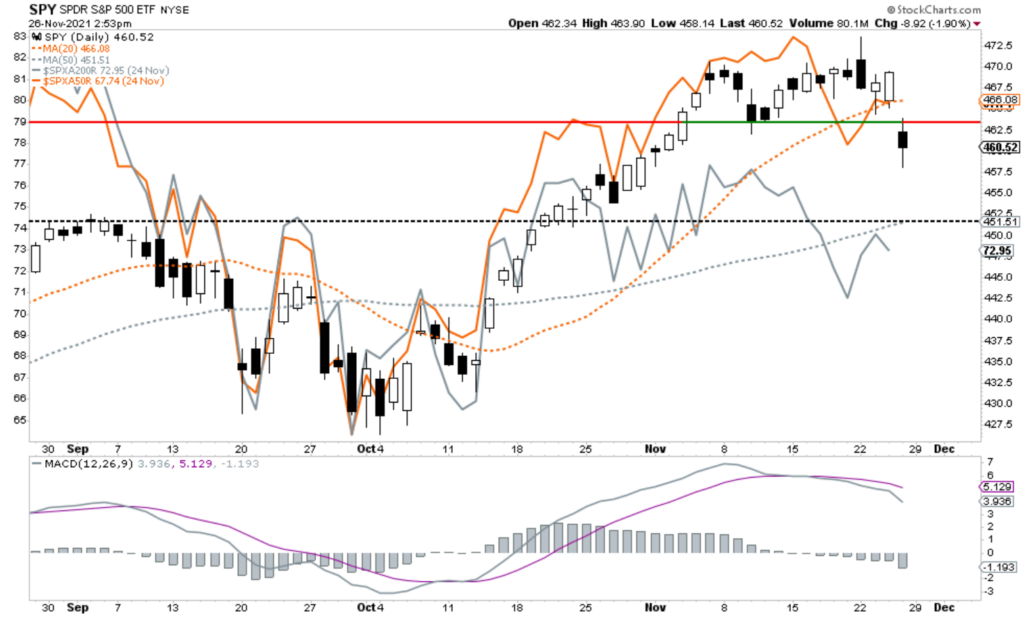

However, there is potentially a negative impact on the market. Such is particularly the case when volumes are weak, liquidity is low, and breadth is poor. As shown, during the entire advance from the September lows, the volume declined. Importantly, over the last week, breadth deteriorated.

All that was missing was a catalyst to create a market correction.

“Over the last couple of weeks, the market has been warning to the risk of a downturn, all that was needed was a catalyst to change sentiment.” – The Real Investment Report

Chart updated through Friday.

The Lack Of Liquidity

On Friday, news of a new “Covid” variant broke, and stocks marked “Black Friday” by plunging firmly through the 20-dma and support at recent lows.

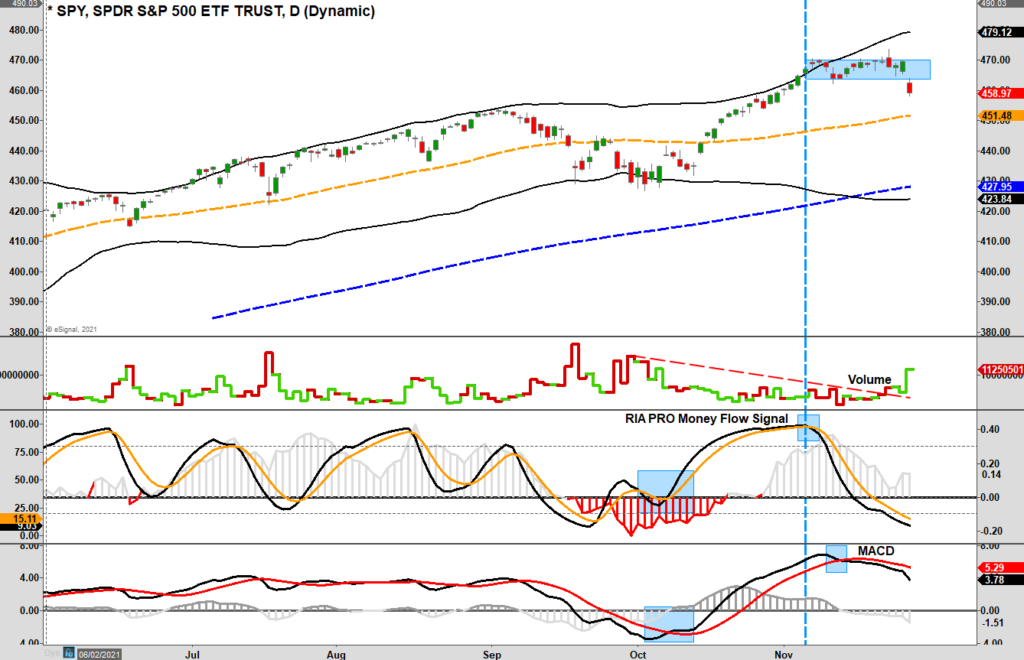

“Notably, that downside break broke the consolidation pattern (blue box in the chart below) that began in early November. While there is some minor support around 4550, critical support lies at the 50-dma at 4527. That support level also corresponds to the September peak.” – Real Investment Report

As you will note, the market correction was swift. Such is because of the “lack of liquidity” in the markets.

As discussed previously, the stock market is a function of buyers and sellers agreeing to a transaction at a specific price. Or rather, “for every seller, there must be a buyer.”

The chart from last week’s discussion showed there was a lack of volume a lower prices. As I wrote:

“Buyers appear to be ‘living’ closer to the 50-dma (orange dashed line.) As the Wall Street axiom goes: ‘Sellers live higher. Buyers live lower.'”

These “gaps” between buyers and sellers lead to sharp price reversions in markets.

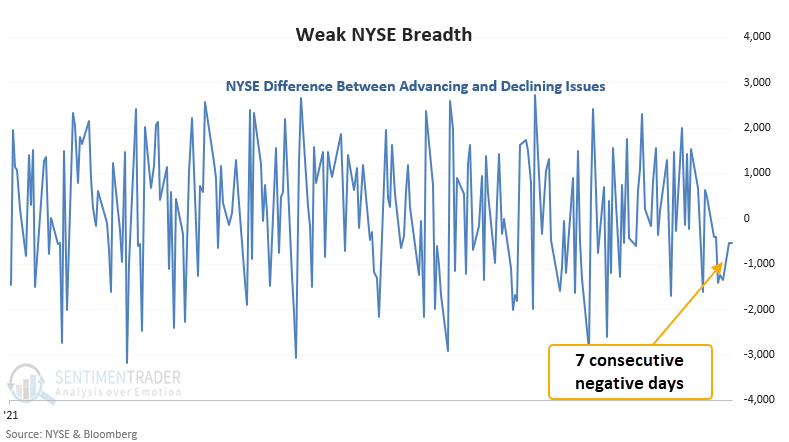

Breadth Suggests There May Be More Work To Do

While the market correction last Friday was sharp and did push several of our short-term indicators into oversold territory, any bounce this week could lead to more selling pressure near term. While we previously noted our concerns about the “bad breadth” of the market, SentimenTrader also suggests such may lead to a pause in the rally. To wit:

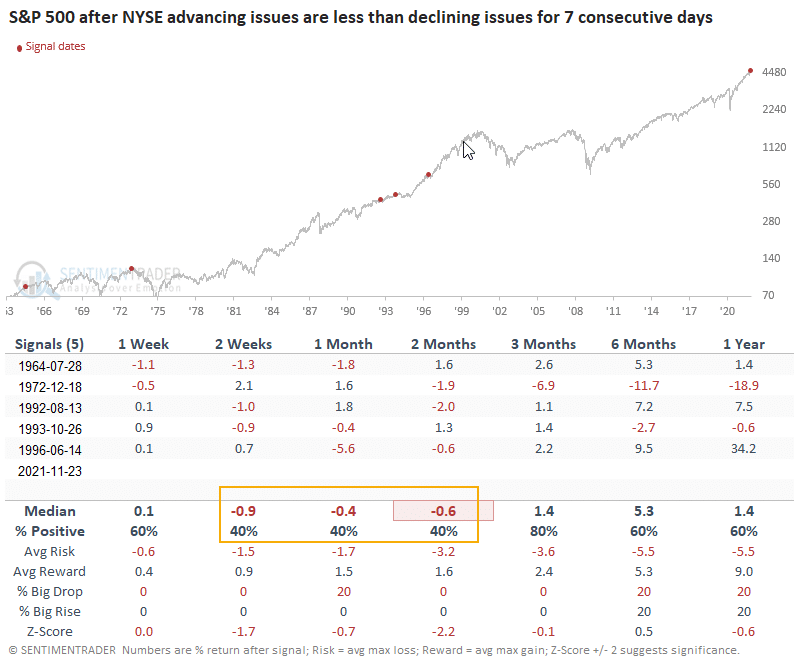

“For only the 6th time since 1926, declining issues outnumbered advancing issues for 7 consecutive days when the S&P 500 closed 2% or less from its 252-day high. If I eliminate the distance below the high condition, the study returns 123 instances when screening out repeats. Almost half of those signals occurred when the S&P 500 was down 10% or more from its 252-day high.”

“This signal triggered 5 other times over the past 96 years. After the others, future returns and win rates were weak in the 2-to-8-week time frame. If I optimize a short signal, the test returns 27 days as the best time frame to hold a negative view of the market. And, the S&P 500 closed down in 5 out of 6 instances. The sample size is small.”

Notably, weak breadth, light volumes on rallies, and speculative behaviors make the market vulnerable to sharp reversals. Moreover, as noted last week, with mutual funds adding to the selling pressure over the next two weeks, there is a risk of further downside.

However, such will provide a trading opportunity for year-end “window dressing.”

Trading The Santa Rally

I agree with Doug Kass’ recent comment:

“While I am not bullish, I am less bearish. On a (tactical) trading and investing basis, markets probably overreacted to the Omicron news on Friday, It is likely time to consider being a bit more greedy when others are fearful. Many stocks, away from “The Nifty Seven,” have fallen dramatically and may represent both shorter and longer-term value“

We agree. After previously taking profits in overbought and extended equities, we are now looking for discounted positions in technology, energy, consumer, and financial-related sectors.

One other comment is that the “Omicron variant” could provide “cover” for the Federal Reserve to slow their monetary tightening. The majority of the rally on Monday was likely bulls coming around to this idea. As such, it was no surprise to see Jerome Powell already pivoting towards a more dovish stance in prepared remarks for the CARES Act Hearing.

“The recent rise in COVID-19 cases and the emergence of the Omicron variant pose downside risks to employment and economic activity and increased uncertainty for inflation.

Greater concerns about the virus could reduce people’s willingness to work in person, which would slow progress in the labor market and intensify supply-chain disruptions.” – Powell

Of course, this is the excuse Powell needs to slow tapering of the balance sheet and delay hiking interest rates.

For now, that keeps the bullish bias in stocks. But as we head into 2022, I would not be surprised to see a pick up in volatility as liquidity flows decline along with economic growth.

As an investor, always remember that making money in the market is only one-half of the job. Keeping it is the other.

“We can not direct the wind, but we can adjust the sail.” – Anonymous