by Tom Parker, CIO of Systematic Fixed Income & Jeff Rosenberg, Sr. Portfolio Manager, Systematic Fixed Income, Blackrock

Real interest rates on Treasuries have been strongly negative throughout 2021. But why do investors keep piling into these negative “real” yielding assets? BlackRock’s systematic investment experts decode the markets to reveal why rates are so disconnected from fundamental values and what it means for your bond portfolio.

Understanding real interest rates

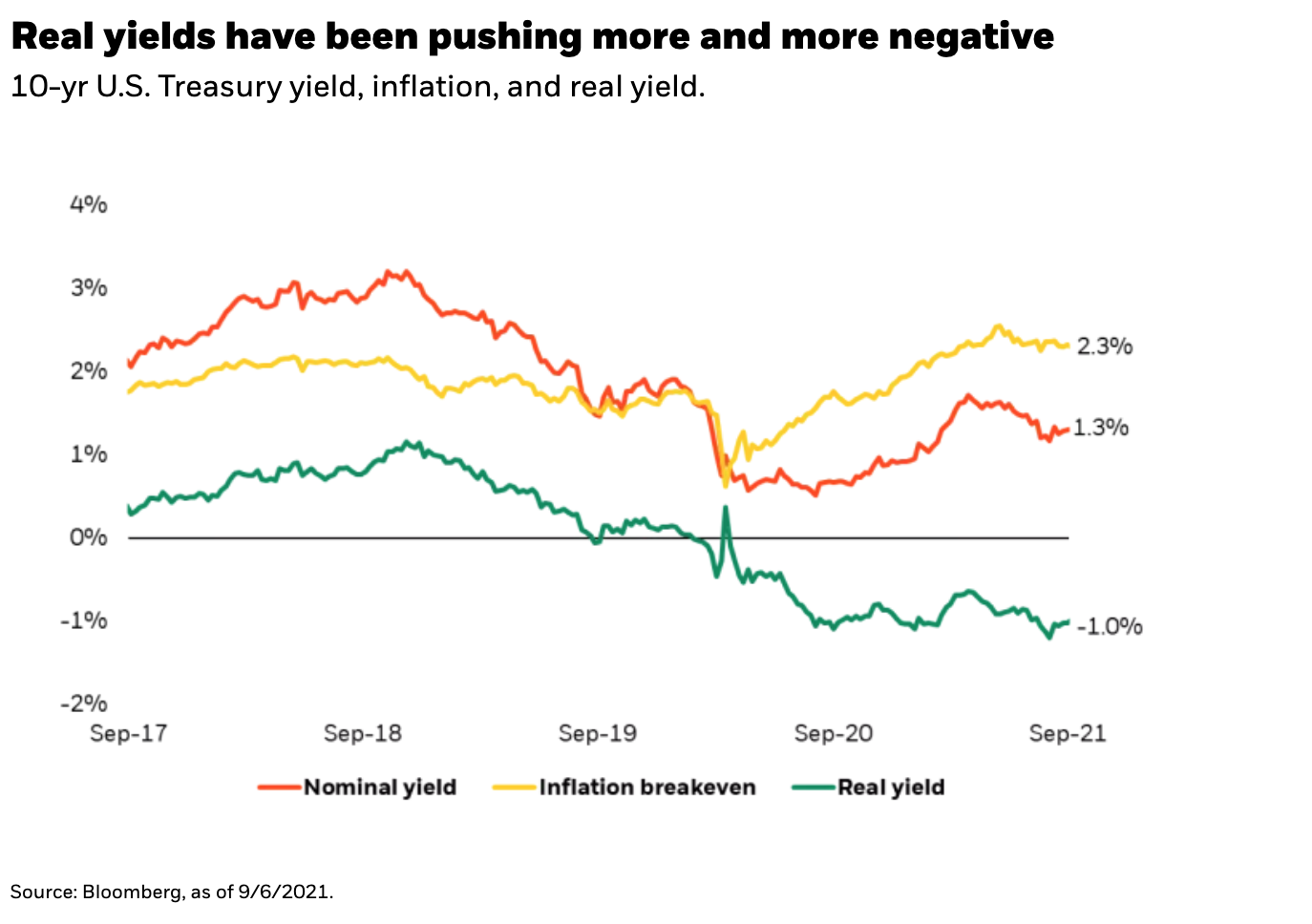

First off, what are real rates and why do they matter? The rates or yields you see on a bond like the 10-year U.S. Treasury are typically “nominal” rates. “Real” rates are the interest rates that an investor receives after adjusting for inflation—in this sense they are the “real” yield you receive from owning the asset. To illustrate, a Treasury bond that pays 5% in nominal yield per year when inflation is 3% per year would have a real rate of 2%. So, the real rate is determined by the combination of the nominal level of rates and the level of inflation.

The real economics aren’t adding up

Why are markets so focused on real rates now? It’s no secret that nominal rates have been declining for a long time. COVID accelerated that trend as investors flocked to safe haven assets like Treasuries during the crisis. This pushed nominal yields down to record lows, but inflation expectations collapsed as well. In early 2021, as economies opened up and economic growth restarted, demand for Treasuries waned and nominal yields rose. But now, with economies still chugging along and yield-eating inflation rising, investors are piling back into Treasuries. The result is real yield dynamics plunging to record lows in the U.S. with the 10-year U.S. Treasury yield around 1.3%, inflation expectations around 2.3% and a real yield at -1.0%.

Once again, at current levels, investors who are buying Treasuries now are essentially expected to earn NEGATIVE 1.0% in real yield annually. The economics just don’t make sense.

Decoding the “real” disconnect in rates and inflation

So, if the economics of Treasuries have been clearly distorted, who is continuing to gobble up these negative real yielding assets? While continued concerns over the spread of the virus may be having an effect, a number of “non-economic” investors are currently creating excess demand for longer-dated Treasuries and driving nominal rates down. Let’s take a closer look at who these investors are:

- Foreign investor demand: As the U.S. economy has reopened, imports of goods from other countries has increased significantly. Many of these exporting companies and countries have bought U.S. debt to build up their foreign exchange reserves. Additionally, while nominal yields are low in the U.S., they are even lower in other parts of the developed world. Many foreign investors have been picking up U.S. Treasuries because of their (relatively) high yield.

- Large institutions are rebalancing: The low level of rates is forcing large institutional investors like pension funds to rebalance their portfolios. Without getting into the nitty gritty of pension accounting, in essence, many pension funds must buy Treasuries to fund longer-term liabilities and cash flows that they must pay in the future. When rates fall, their calculated level of liabilities rises, forcing them to buy more Treasuries to offset their future liabilities. The result is steady demand from some of the world’s largest investors.

- Momentum players are piling in: The Treasury trading ecosystem now has a large number of algorithmic-based investors that hedge portfolios by responding to the direction of rates quickly. Our research shows that these momentum traders have recently shifted from going short (selling U.S. Treasuries), to going long (buying U.S. Treasuries). Once again, adding incremental demand.

What is the catalyst for real rates to move up?

One thing each of these investor types has in common is that none of them are buying Treasuries because they are cheaply priced or have a strong long-term return potential.

The catalyst for higher nominal rates (and as a result real rates) will not be the fact that they are out of sync with the current macro story. This is already well-known by the market. Instead it may come down to a combination of factors that may startle the investors who have been steadily grazing on Treasury bonds. It could be upside surprises in job growth, even more profound moves in fiscal spending, sooner-than-expected rate hikes by the Fed, or the realization that “transitory” inflation might be much longer than expected.

In our view, the most powerful catalyst may be a starkly positive real growth surprise that will finally move the non-economic players—resulting in the real rate economics to matter once again and significantly elevating nominal rates. However, without significant growth surprises, it will be hard to move the excess demand for longer safe assets that is being created by large excess liquidity in the financial system.

What do negative real rates mean for bond investors?

Low nominal rates in Treasuries results in low yields everywhere else in fixed income markets—creating a major problem in the face of higher inflation. The most recent reading of U.S. inflation in July was 4.3% as measured by Core CPI. To put that into context, if we look at the Bloomberg Barclays Multiverse Index as a proxy for the global bond market, only 3.7% of bonds are yielding more than 4% in nominal terms. While this level inflation is likely to abate, it’s a clear headwind for fixed income returns right now.

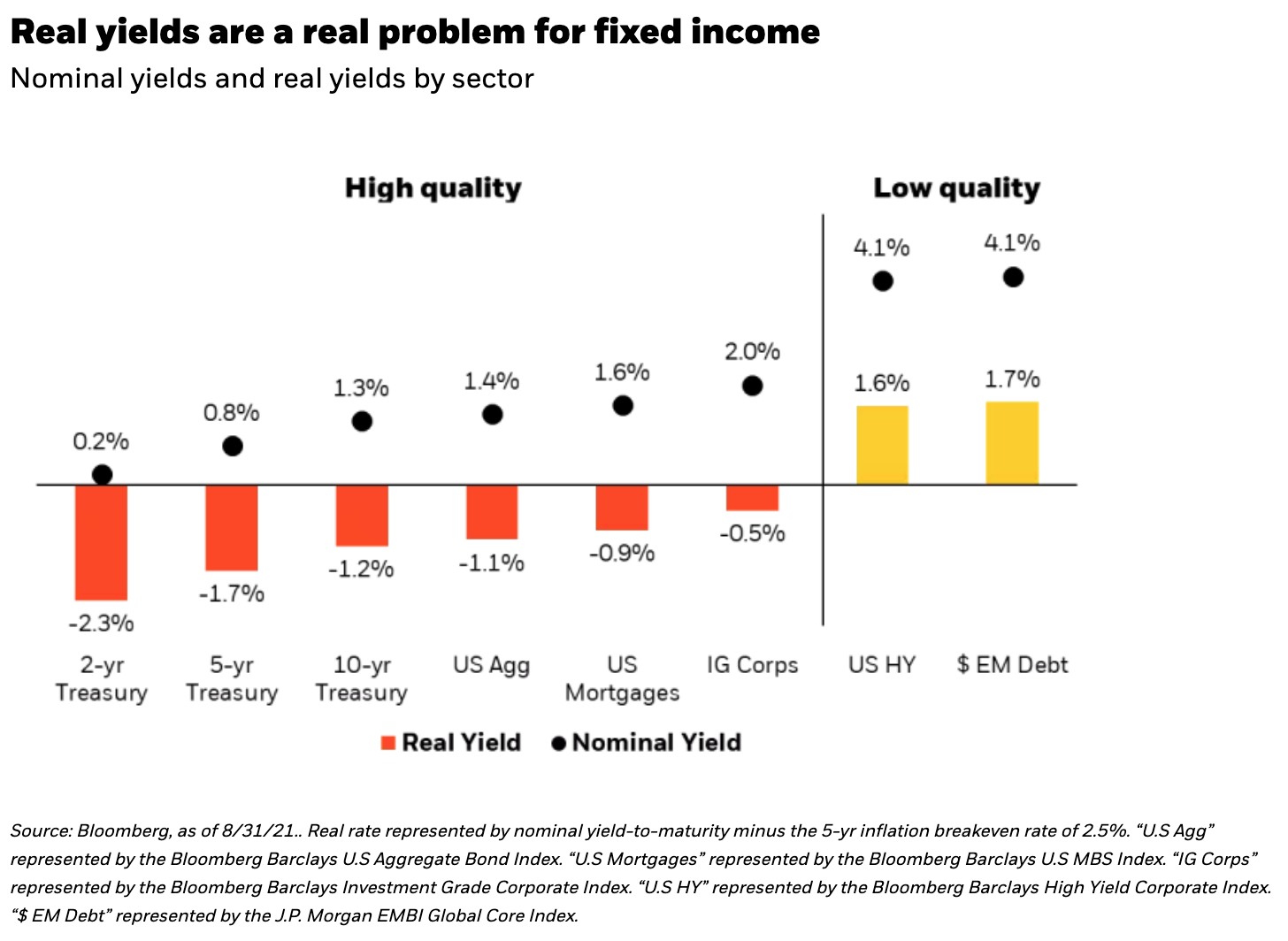

Viewing inflation across a more realistic 5-year timeframe shows just how high of a hurdle inflation poses for nominal yields. The chart below outlines the real yields of different fixed income asset classes based on the current nominal yield minus the market implied rate of inflation over the next five years of 2.5%.

High quality bonds such as Treasuries, mortgages, and investment grade corporates all result in strongly negative annual rates of real yield. Looking at the Aggregate Index, which is commonly used as the core of investors’ bond portfolios, the expected real yield is -1.1% over the next 5 years. In order to gain any positive real yield, investors must look at lower quality holdings such as U.S. high yield corporate bonds or dollar-denominated emerging market debt to gain low single-digit yields.

Clearly there are some hard choices ahead for bond investors. Doing nothing and staying in the safety of high quality bonds results in negative real yields. On the other hand, reaching out into lower credit quality securities like high yield and emerging market debt comes with higher default risk, more volatility, and potentially greater correlation to equities—all for a meager level of positive real yield.

Bottom line

Real rates are likely to remain low in the absence of a sudden growth surprise with some room to slowly rise as non-economic demand forces abate slightly. For investors who care about bond economics and the “real” rate of return, many have turned to finding higher nominal yields in riskier areas of the fixed income market. This strategy comes at the cost of sacrificing the safety of bond allocations and reduces diversification potential if equity markets sell off. To that end, the real problem of negative real yields looks like it is here to stay and makes rethinking the 60/40 portfolio framework more imperative than ever.