by Randall Dishmon, Invesco Canada

I often get asked about my team’s outlook, or our thoughts on “What’s the market going to do from here?” Well, we don’t make market predictions for a living. I’ve yet to see the person in this industry, no matter how bright they may be, who can consistently make money from correctly calling what the short-term gyrations of the market are going to look like.

In particular, there seems to be a great deal of controversy in the financial media around the question of valuation and the struggle between “value” and “growth” for style supremacy. People love labels. But the people who have known me for the past 20 years know I hate labels. I believe they’re the enemy of great investing.

The style question misses the point

In general, I think the entire discussion around style misses the point. The market has a valuation attached to it – sometimes it’s fair and sometimes it’s too high or low. But we don’t buy the market, we buy a highly curated list of great ideas all around the world. We look for companies that have a competitive advantage within broader structural growth themes that are changing the world — things like e-commerce, cloud software, medical diagnostics and life sciences tools, digital payments, and immuno-oncology.

In my view, the price-to-earnings ratio of individual stocks or sectors is useless information without a thorough understanding of what is happening to their fundamentals. Both have to be taken together. We’re not concerned about the valuation of what we own; we own stocks because we believe their fundamentals are very, very strong and there is much that we like about these businesses.

A commodity supercycle?

Many commentators like to fill airtime speculating that we’re in the early stages of a commodity supercycle, a similar dynamic to what drove the last period of value outperformance back in 2000-2007. This may make for entertaining television, but we think the parallels they’re drawing are wrong. In our view, what fueled that bull market in commodities was the huge level of capital investment required to urbanize China, which is a demographic wave that is unprecedented in human history and it won’t be repeated any time soon, maybe ever.

Rather, we’d bet this is a market cycle, unfolding in a normal rhythm, but off of a level of severity that has been extremely rare due to the COVID-19 pandemic.

Early expansion periods tend to favour value

So where are we in that market cycle? Historically in a recession, amid an environment of weak earnings and declining interest rates induced by central bank policies, stocks often begin to move up. Multiple expansion can occur quickly in the stocks most levered to a recovery (such as cyclicals with debt on the balance sheet), as the market looks past the current weakness in the economy. Strong earnings may last a year or two as the market cycle plays out, but that early multiple expansion is where the best returns have often happened across the whole cycle for value stocks.1

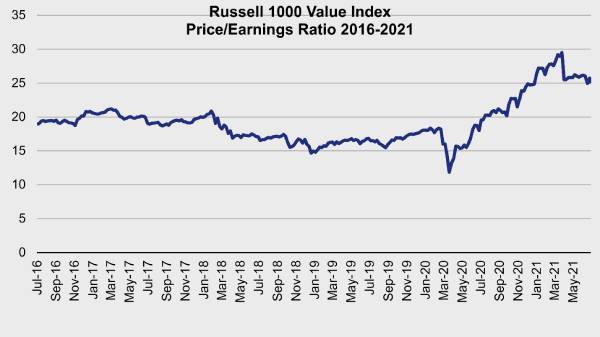

And indeed, if you were waiting for the recovery in value coming out of the pandemic … it’s already happened. It may surprise many readers, for example, that the Russell 1000 Value Index has outperformed the Russell 1000 Growth Index prettily handily on a trailing 12-month basis.2 The big “value” multiple expansion was a back half of 2020 and early 2021 phenomenon (see Figure 1).

Figure 1: Value stocks staged a recovery coming out of the pandemic

In contrast, growth is usually less in favour in an early expansion.1 Most of the better long-term growth companies have share prices that tend to follow the revenue growth up over time, which makes perfect sense. Investor cash, however, has been finding opportunistically higher returns elsewhere lately, in the cyclicals.

Structural growth trends endure

That is where we are now. Rest assured that structural change has continued to play out, away from the spotlight of the market these last few months, and we expect markets to find appeal (as they always have) in the strong, accelerating growth many of these companies offer as the cyclical rebound peters out. Earnings are now coming in nicely for the structural growers, as they are apt to do for a while yet, in our view.

Always and forever, within the broad aggregate valuation level, the market continues to make mistakes … our job is to be prepared and willing to act with conviction when it does, so that we can buy structural growth leaders at attractive prices. Market mistakes, like much of what we witnessed during the month of March 2020 and again earlier this year, create opportunity for long-term investors like us, and many of you.

The structural growth areas that I mentioned previously are undergoing once-in-a-generation changes, and we think the market continues to underestimate the sustainability of the growth potential of the leading companies in these areas. Valuations remain very attractive. Earnings season will be upon us again in a few weeks and we are excited about the potential in many of the stocks we own.

1 Source: Bloomberg, L.P., based on the Russell 1000 Value Index and Russell 1000 Growth Index, and how their P/E ratios have expanded/contracted across market cycles. Past performance does not guarantee future results. An investment cannot be made directly in an index.

2 Source: Morningstar as of June 25, 2021. 12-month return for the Russell 1000 Value Index was 45.31% and for the Russell 1000 Growth Index was 41.84%. Past performance does not guarantee future results. An investment cannot be made directly in an index.

This post was first published at the official blog of Invesco Canada.