by Ryan Detrick, CMT, Chief Market Strategist, LPL Financial, and

Jeff Buchbinder, CFA, Equity Strategist, LPL Financial

“Sell in May and go away”[2] is probably the most widely cited stock market cliché in history. Every year a barrage of Wall Street commentaries, media stories, and investor questions flood in about the popular stock market adage. We tackle this commonly cited seasonal pattern and why some seasonal weakness could make sense in 2021.

THE WORST SIX MONTHS OF THE YEAR

“Sell in May and go away” is the seasonal stock market pattern in which the six months from May through October are historically weak for stocks, with many investors believing that it’s better to avoid the market altogether by selling in May and moving to cash during the summer months.

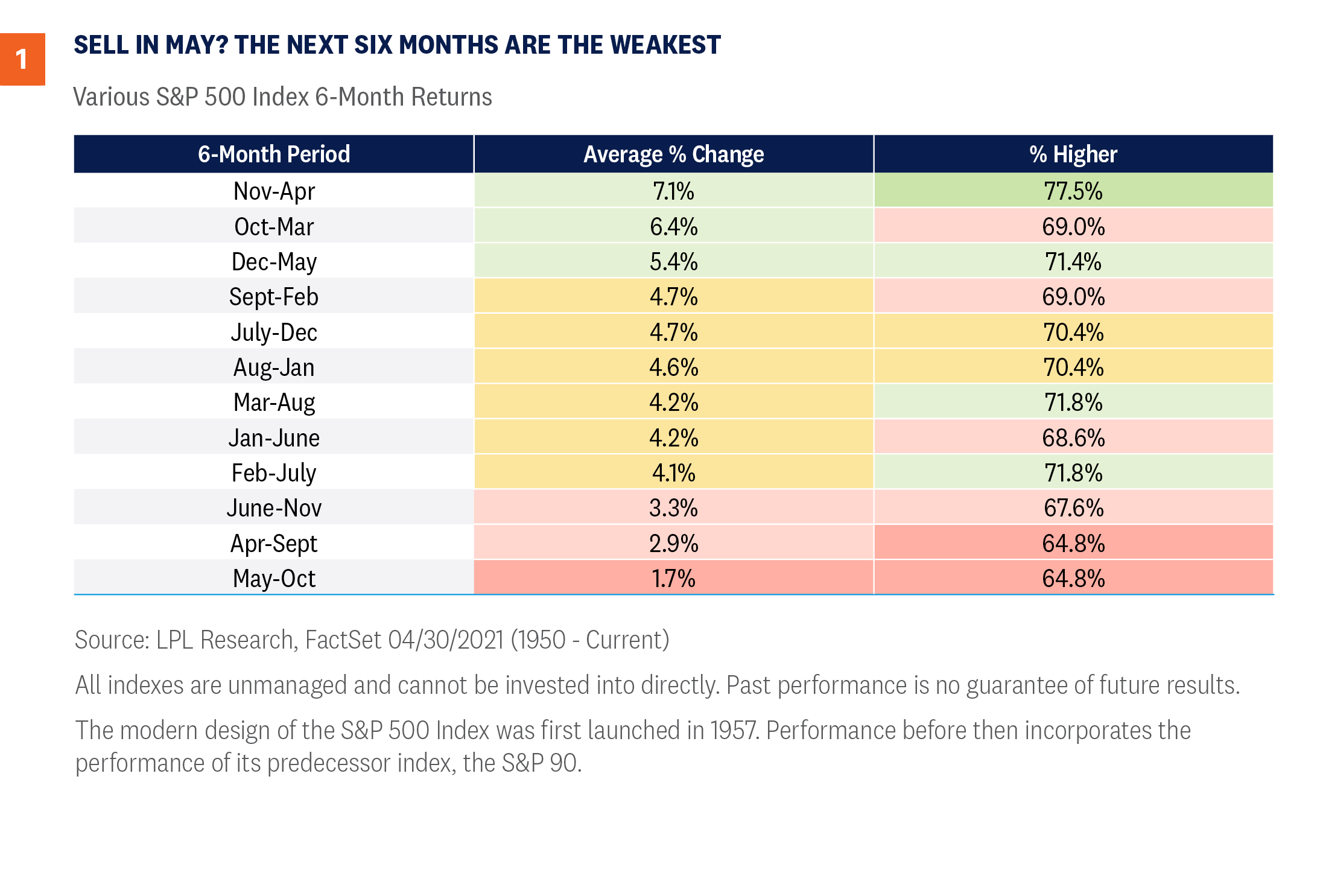

As [Figure 1] shows, since 1950 the S&P 500 Index has gained 1.7% on average during these six months, compared with 7.1% during the November to April period. In fact, out of all six-month combinations, the May through October period has produced the weakest—and least positive—average return.

With the S&P 500 up 87% from the March 2020 lows, we do think the potential for some seasonal weakness is high and would be perfectly normal after such a run.

WHAT HAVE YOU DONE FOR ME LATELY?

As we head into this seasonally weak period, keep a few things in mind. First, the S&P 500 has closed higher during the month of May in seven of the past eight years—so “Sell in June” might be more appropriate. In addition, stocks appear to get a boost in May of a post-election year, as the S&P 500 is up 1.7% on average these years, with only July and November stronger.

The point is that investors shouldn’t necessarily blindly sell on May 1, but rather should be aware that volatility tends to happen in the summer and fall months. As we mentioned in our April 19, 2021 issue Peak Optimism?, we do see some signs that the bar is quite high now for further upside market catalysts. Everyone knows the reopening is happening, and everyone knows the economy is roaring back. From a contrarian point of view, this high bar could be tougher to clear as we move into the seasonally weaker summer and fall months.

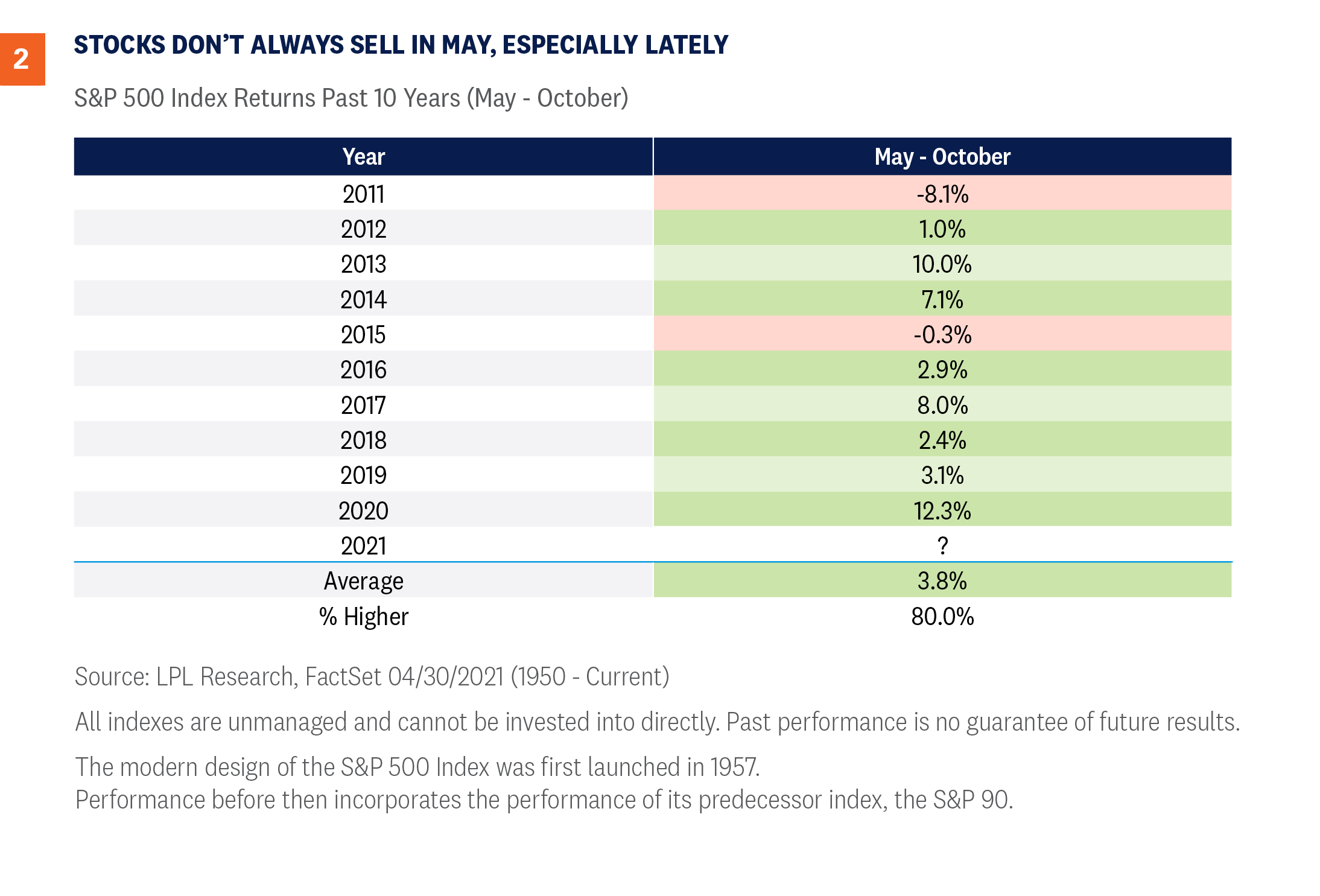

Here’s the catch—and there’s always a catch: These ‘worst six months of the year’ have been quite strong lately. In fact, stocks gained eight of the past 10 years during these six months, as you can see in [Figure 2]. So, although our guard is up for some potential seasonal weakness, be aware it could be short-lived, and we’d use it as a buying opportunity.

FOUR OTHER LOOKS AT THE NEXT SIX MONTHS

Let’s take a deeper dive into these ‘worst six months of the year’:

When April is up more than 5%, like it was this year, the next six months are up 6.2% on average—well above the 1.7% average during these six months.

Post-election years average 2.4% during these worst six months.

The best six months of the year just ended, and they gained nearly 28% this time around. It appears that big gains during these months can eat away at future returns. In fact, the next six months are up only 0.7% on average when the previous six months are up at least 20%.

When the S&P 500 closes at a new monthly high in April, like it did this year, the next six months do much better, up 5.6%.

Putting it all together, the only other year in history to close April at a new monthly high, be up at least 20% during the previous six months, and do it all in a post-election year was in 1961. What happened the next six months? The S&P 500 gained a very respectable 5.1%.

CONCLUSION

The media will have fun with the whole “Sell in May” warning to drive up clicks and views. Although you can’t argue that these months historically have been weak, they still sport a positive return, so totally going away isn’t wise. Recently we’ve been noting some potential reasons for at least a pause in the rally, and now the calendar adds another.

But amid a backdrop of an improving economy, massive levels of fiscal and monetary stimulus, and rising vaccination rates, we don’t expect any pullbacks to last very long, and we’d use any that appear as a buying opportunity. While we upgraded our forecast for the global economy and U.S. corporate earnings last month, for now we are maintaining our fair value target range for the S&P 500 of 4,050–4,100. At the same time, we acknowledge the environment appears supportive for stocks to do better, and we continue to recommend an overweight-to-equities and underweight-to-fixed-income position relative to investors’ targets, as appropriate.