by Jared Dillian, The 10th Man

If you were to describe my trading style, you might say that I like to look for asymmetric opportunities. Places where you could lose a little, but make a lot.

That’s it, that’s the strategy.

The other strategy is called “picking up nickels in front of a steamroller.” Where you can make a little, but lose a lot.

What I’m describing here is optionality without explicitly trading options, but there is optionality in everything we do.

Going to college is a bit like optionality. You pay an annual premium, which gives you the ability to greatly increase your future earnings potential—or not.

Getting tattoos are like selling options—you’re limiting your future earnings potential (especially if you get them on your neck). But you may decide that you are so rich that you don’t care, which explains why both celebrities and the underclass tend to have tattoos.

Once you learn about optionality, you see it wherever you go.

I posted a tweet over the weekend that went a bit viral:

I would not be subscribing to any newsletters from people who were not educated in bonds or options. (For the record, I have taught classes at the undergraduate and graduate level on bonds and options.)

If you know bonds, you understand discounting cash flows, duration, and convexity. If you know options, you know asymmetry, convexity, and volatility. Basically, everything you need to know about finance.

If you know stocks, you know stocks go up, and stocks go down. You have the most primitive understanding of finance imaginable.

Having said that, if you understand stocks, you understand sentiment and psychology, but you don’t understand anything about math.

Stated another way, my investment philosophy is: looking for long balls. 5x–10x opportunities or more.

Inflation Is an Asymmetric Opportunity

If you’ve been reading The 10th Man over the past year, you know that I have been bullish about inflation. That became clear early on in the pandemic, when we were pumping cash directly into the economy.

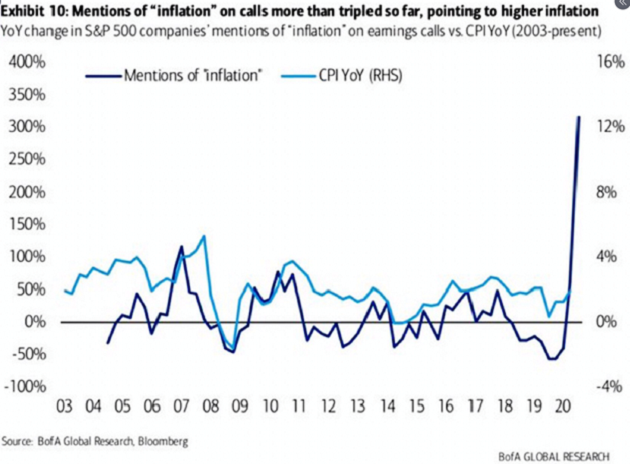

Now, the inflation is here:

Source: @LizAnnSonders

I have read dozens of these earnings calls where inflation was mentioned. It’s showing up in raw material costs, transportation costs, and labor costs. It’s everywhere. And companies are raising prices in response.

PPI printed 4.2% not long ago, which should get people’s attention. Mohamed El-Erian says that 3% inflation at this point is pretty much a given.

For the past year, I have been saying that value stocks and commodity-linked stocks were underpriced. What I did not say (but what I could have said), is that they are cheap options. And they are still relatively cheap.

You may believe that inflation is transitory—lots of people do. “All of this is supply chain stuff or distortions caused by the government,” they say. “Once we work through this, we’ll be back to low and stable inflation.”

This is not my belief. My belief is that we have entered a period of persistently high inflation.

From an investment standpoint, these trades give us lots of optionality—we can lose a little, or make a lot.

Short Options

Everyone knows that selling options uncovered exposes you to unlimited loss. People don’t like to sell puts. I will actually do it from time to time, under certain circumstances, if the volatility is high enough. That’s actually how I acquired most of my position in the VanEck Vectors Gold Miners ETF (GDX).

I think people have mostly learned their lesson from the VelocityShares Daily Inverse VIX Short Term ETN (XIV) blowup of a few years ago, but give it a few years, and they’ll be doing it again.

I’m less concerned about explicitly being short options than I am about implicitly being short options. Buying Apple (AAPL) stock is a form of implicit options selling. What can go right that hasn’t already gone right? What could go wrong?

A dumb stock guy would say that AAPL is “priced for perfection.” This is just an unfancy way of saying that there’s a lot of asymmetry—the stock can go down more than it can go up. This is true of most big tech stocks.

When oil prices went negative last year, there wasn’t much more that could go wrong for oil—and everything could go right. This was the kind of asymmetry that I was looking for. Buying an oil stock at that time was essentially like buying a call option—because the entire energy industry was valued at zero.

Most of the folks you see on TV talking about stocks are very unsophisticated. They may have some understanding of sentiment and positioning, but they are ignorant of asymmetry and optionality.

Of course, many options expire worthless, and I’ve bought stocks in the past that didn’t live up to their promise. But there wasn’t a lot of downside, and that’s the point. It’s like being long volatility—without actually trading any volatility.

It’s what’s worked for me for years, and I recommend you try it out.

And finally, please check out my latest music Mystery—it will keep you focused while you work.

Jared Dillian

Copyright © The 10th Man