by

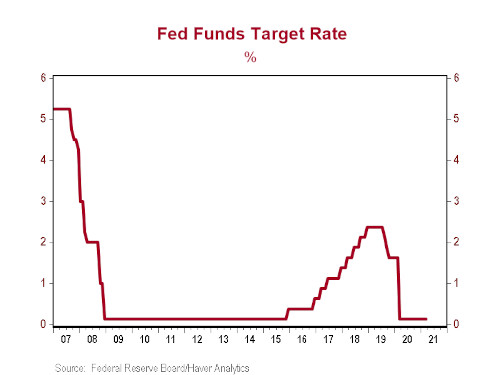

Nobody expected the Fed would lift interest rates today. In fact, virtually nobody expects them to raise rates before the end of next year (and the March dot plots show the Fed's own forecasts have them on hold through 2023). But there are actions – such as tapering asset purchases – that are likely to come before rates lift off. And indeed, this was the first question out of the gate as the Q&A portion of Chair Powell's press conference began. In response, the Chairman stated that the Fed is not even "talking about talking about tapering," before elaborating on a few of the reasons the Fed expects to be on pause for the foreseeable future.

First, on employment, the Fed wants to see a string of strength in job creation. While the March gains were strong, it was only one month, and nonfarm payrolls remain down more than 8.4 million from pre-COVID levels. Even with record employment growth in 2021, the employment market is likely to remain below pre-COVID levels for a while. The economy is not a light switch, and when things were shut down last year, it caused lasting damage. Hundreds of thousands of companies closed their doors, and it will take time for jobs to get back to where they were. With damage concentrated among low-income jobs, the employment mandate is likely to be the key factor keeping policy accommodative for a while.

Chair Powell also reiterated the Fed's belief that labor market slack – and not the massive increase in the M2 money supply – will be the primary factor preventing inflation from moving sustainably higher. In the short term, he said, inflation is being pushed higher for two reasons: 1) base effects, meaning that readings will run high in the short-term simply due to the low levels we are coming off of, and 2) supply chain bottlenecks, which the Fed expects will be resolved as companies and workers get back towards normal. In effect, the Fed puts little weight on the above-trend inflation readings that look likely in the coming months. We expect that inflation pressure from massive money printing will sustain even as supply chain issues ease, but only time will tell.

In the meantime, the Fed will continue to purchase Treasury securities at a pace of $80 billion per month, and agency mortgage-back securities at a pace of $40 billion monthly. For now, the Fed will remain incredibly accommodative. This means faster economic growth (and positive backdrop for equities), but the risk into the future of too loose for too long is rising. The good news is that entrepreneurship is not dead, businesses will re-open, and the US will benefit from productivity gains as a by-product of technology adoption forced by the COVID-19 disaster. Growth will continue, and at an above-trend pace, but the sugar high from spending and loose policy warrants careful scrutiny in the year ahead.

Click here for a PDF version