by Frank Caruso. CIO, US Growth Equities, AllianceBernstein

Many US technology companies use stock compensation to help align workers’ performance with shareholder interests. But stock-based compensation also creates accounting distortions that add risks to unwitting investors—especially as growth company valuations face increased scrutiny today.

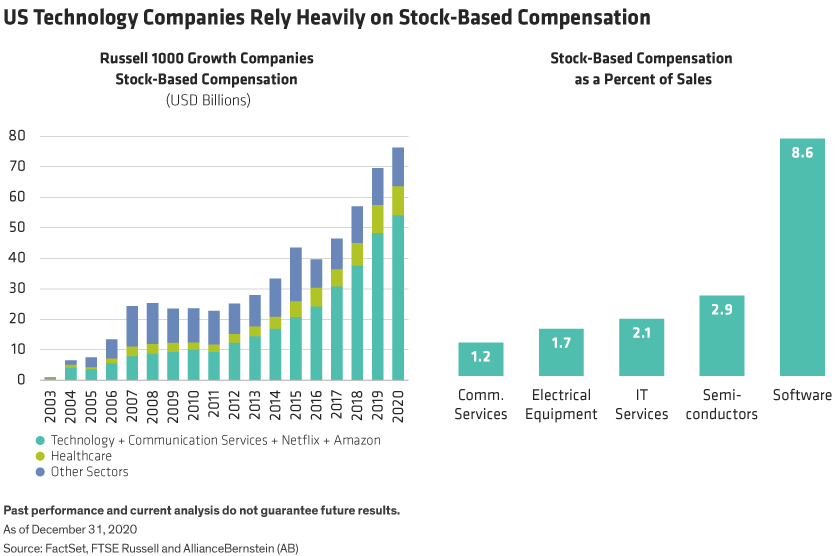

Engineers and salespeople in public US technology firms receive a significant portion of their pay in the form of stock-based compensation (SBC) (Display). Company boards and management teams generally believe that this is a good way to link workers’ performance with shareholders’ interests. Employees seem to like it too, judging by reports that tech firms compete hotly for talent with promises of stock.

Does Noncash Mean “Not Important”?

Tech firms also favor SBC because it flatters company accounts. Investors typically exclude SBC expenses from their calculations of free cash flow on the grounds that this expense is noncash. Firms issue so-called pro forma results and guidance without SBC expense alongside the official presentation. After all, managements tend to do what investors encourage them to do.

Accounting standards require the expensing of SBC. This is because SBC permanently increases (that is, dilutes) the share count, lowering future per-share returns. Equity dilution is noncash only in the trivial sense that it happens directly to the investor through the share count rather than immediately through the cash-flow statement, and in the future rather than the present. But a permanent reduction of future dividends per share is economically significant whether one calls it noncash or not.

Why Care About Stock-Based Compensation?

The divergence between official accounting earnings and pro forma earnings is often extreme. In fact, many US technology firms are unprofitable under the prescribed accounting rules. As a result, shares that are already expensive compared to inflated free-cash-flow numbers are astronomically so when compared to the official measure of earnings (Display).

Investors are left with an uncomfortable conclusion: either they’re ignoring the economic truth, or the accounting profession doesn’t know how to measure profits. We believe the accountants have got this one right. Investors, management teams and employees are taking much greater risks by overvaluing shares than they probably realize.

Are the Good Times Ending?

Until recently, a buoyant market made it easy to overlook some of these risks. Over the past 10 years through the end of 2020, the technology-heavy Nasdaq Composite Index rose five-fold. In recent months, however, technology stock gains have decelerated and shares of some high-flying growth companies have come back to earth.

For employees focused on their jobs, it is easy to forget the larger financial context when accepting SBC. In fact, growing risk appetites and falling interest rates—rather than rising corporate earnings—have fueled most of the stock gains in recent years. By the end of 2020, the interest rate on the US Treasury’s 10-year bond had fallen to barely 1%, from over 3% in early 2011. But in early 2021, rapidly rising US Treasury yields added risks for growth companies, whose multiples tend to be especially vulnerable to higher interest rates.

These trends will also affect the risk premium—the extra return that investors require for owning stocks—which has fallen from a very high 10% to around 5% today.

Coupled with the earnings recovery from the Global Financial Crisis, these valuation tailwinds have provided an enormous boost for stocks, especially growth stocks. It would be natural for employees and managements to attribute these gains to their individual efforts.

Day of Reckoning for Technology Employees—and Investors

But that would be a mistake. Stocks cannot appreciate as fast as in recent years forever, and at some point, a market correction is likely. If this happens, many employees who are heavily remunerated in SBC will discover that they’ve been earning much less than they thought.

When the reckoning comes, demoralized employees are likely to demand more pay in cash rather than stock. This would make the expense of compensating employees too obvious for even the most creative stock analyst to ignore. And the accountants will be able to say they had been warning us all along.

What’s the lesson for investors? SBC is an important example of how pro forma adjustments to earnings can mislead investors. It reinforces why we think profitability measures—such as return on assets and return on invested capital—are a much better way to gauge the sustainability of cash flows and equity returns. As market conditions rapidly change, we think investors in technology companies should dig deeper into employee expenses to ensure that a precarious compensation structure doesn’t undermine return potential for an otherwise solid business.

Frank Caruso is Chief Investment Officer of US Growth Equities at AB

Vincent Dupont is Director of Research for US Growth Equities at AB

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

This post was first published at the official blog of AllianceBernstein..