by Jennifer DeLong, AllianceBernstein

Planning for retirement has historically been focused on saving as much as possible. But if the actual target is to secure income for life, we think giving participants a preview of the future income they’re building can encourage even better savings habits now.

Saving for retirement is a long-standing goal of American workers, but the focus of defined contribution (DC) plan participants is increasingly shifting from how much they can save to how much income they can secure. Encouraging participation and offering matches and sound investment options is a solid foundation, but plan sponsors should also bring retirement income to life for participants.

Visualizing Future Income Now Can Help Avoid Shortfalls Later

Retirement goals can seem distant, so many participants need assurances that they’re on the right path to retire on their own terms…without worry. And translating participants’ current savings into expected retirement income down the road makes it more tangible and relevant.

Besides encouraging better savings behavior, retirement-income visualizations can help participants avoid potential shortfalls, particularly if an ill-timed market downturn happens near or in retirement. But the translation must be as trustworthy as it is transparent. That’s why a guaranteed income stream—like one offered through annuities—that starts building long before retirement can provide the foundation for this income “preview.”

Acknowledging the growing need for better insights into future income, the SECURE Act of 2019 established a lifetime income-disclosure mandate for plan sponsors. Proponents argued that participants need to know (and plan for) their future retirement income—and that DC plans must regularly provide a road map. And while the disclosure is somewhat basic, it still raises much-needed awareness of how far (or short) their retirement savings will go.

Income Awareness Has Been Linked to Higher Participation…and Savings

New disclosure requirements may mean more work for sponsors and their service providers, but the well-documented advantages of fostering an income mindset seem worth the effort, in our view.

When income is front and center, for example, participants are more inclined to engage and save, based on our experience. In fact, among 75,000 active participants in our DC plans that offer an in-plan guaranteed-income option, over a seven-year period we saw a 12% higher savings rate for those who were more directly engaged with their income strategies versus those who weren’t.

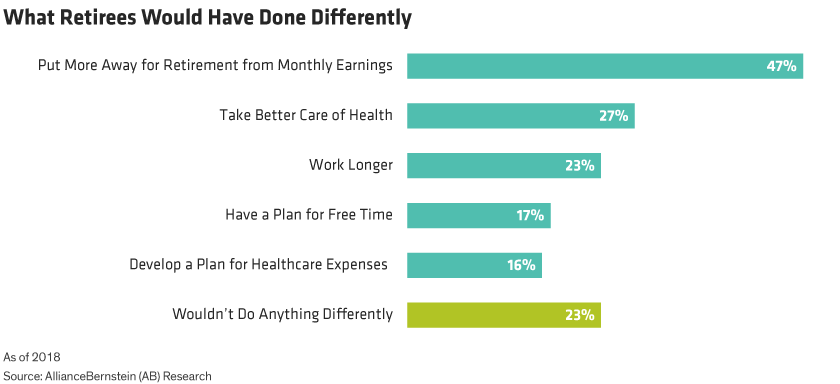

The need to start saving more and earlier is hardly a new concept, and who better to reinforce its importance than today’s retirees? Some 47% said they would have put away more money while they had the chance—nearly double the percentage of those who prioritized their own good health in the lead-up to retirement—based on the AllianceBernstein (AB) survey Inside the Minds of Plan Participants (Display).

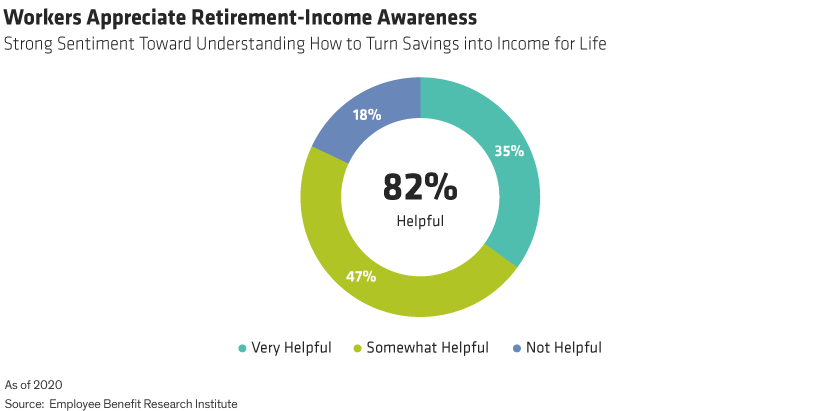

With clear advantages and new federal mandates, plan sponsors certainly have incentive to follow through on how to convert savings to income. Just as importantly, it’s also what participants want. Over 80% of workers said any education or advice along these lines is helpful, according to a survey by the Employee Benefits Research Institute (Display).

Flexibility to personalize income—and make changes any time—is equally appealing, or at least less intimidating than “irrevocable” options such as deferred annuities, which tend to have the opposite effect. Some annuities impose complicated decisions on participants, often leading to procrastination and avoidance altogether—a result that could crimp long-term savings.

Today, retirees are living longer, more active and healthier lives—so retirement money needs to last. Market volatility and potential inflation also need to be considered. If plan sponsors want to help retirees avoid late-inning surprises, they may need a new philosophy that gets back to the roots of why they offer plans to begin with. We believe that those goals are to encourage wider participation, higher savings rates, steadiness in tough markets and income security—all critical building blocks to retiring with confidence.

Jennifer DeLong is Managing Director, Head—Defined Contribution at AB.

Andrew Stumacher is Product Director—Custom Defined Contribution Solutions at AB.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

This post was first published at the official blog of AllianceBernstein..