by Bill Hao, S&P Dow Jones Indices

In the previous blog, we introduced SPACs and discussed market trends that emerged given SPACs’ popularity. In this blog, we will discuss SPACs’ lifecycle, as well as the benefits and risks of investing in SPACs.

SPAC Life Cycle

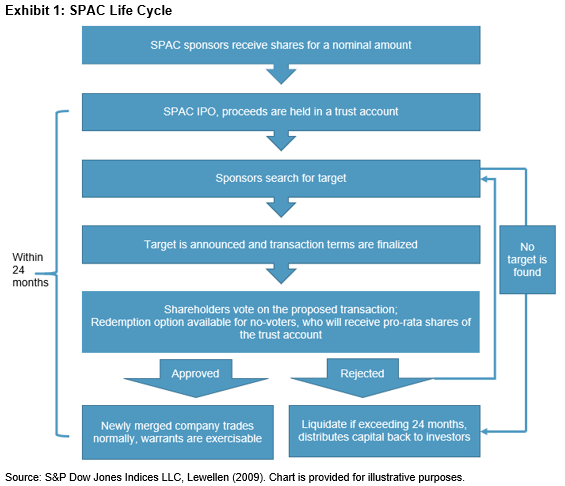

There are three stages in a typical SPAC life cycle.

1. A SPAC’s IPO

When SPAC sponsors form a SPAC, they are typically given 20% of the post-IPO shares for a nominal investment amount. The SPAC then goes through the IPO process. In a typical SPAC structure, the SPAC raises capital by issuing units consisting of one share and one-half or one-third of a warrant. On NASDAQ for example, the shares are generally priced at USD 10 and the warrants are typically struck 15% out of the money (USD 11.50) with a five-year term and a USD 18 forced exercise.1

The capital raised is held in a trust account. The common stock and the warrant typically begin to trade separately, starting on the 52nd day following the IPO.2 Thus, a SPAC could have multiple instruments listed simultaneously, including unit, common stock, and warrant.

2. Seeking a Target

After the IPO, the sponsors will start to search for an acquisition target and finalize the transaction terms once the target is found. NASDAQ requires that the transaction must be valued at 80% or more of the funds held in the trust.3 Typically, the sponsors have 18-24 months to find a target.4

3. De-SPAC

Once the acquisition target is found, depending on the SPAC’s prospectus, shareholders may need to vote on the transaction, or they will receive redemption notices if they choose to receive a pro-rata amount from the trust account and walk away. If the acquisition is approved by shareholders, the SPAC merges with the target company and will often undergo an identifier change to reflect the name of the target business. Otherwise, the sponsor will resume searching for another target. If the sponsor fails to find a suitable target within the pre-defined timeframe, the SPAC will be liquidated, and the investors will receive their capital back from the trust account. This process is detailed in Exhibit 1.

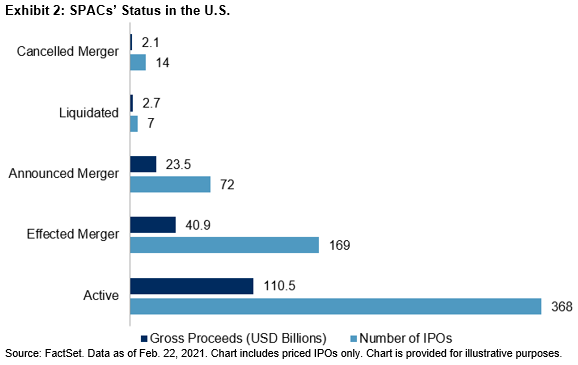

Based on a SPAC’s life cycle, we can split a SPAC’s status into five categories: active, announced merger, effected merger, cancelled merger, and liquidated. Currently, most SPACs in the U.S. are actively looking for the acquisition target (see Exhibit 2).

Benefits and Risks of SPAC Investing

Market participants can gain several benefits through investing in a SPAC, compared with investing in private equity.

- Institutional access: SPACs offer access to investment in acquisitions that are typically otherwise restricted to large institutions through private equity. With SPACs, retail investors can invest with the SPAC sponsors who usually have investment and industry expertise. Unlike private equity, investors do not have to pay management fees to SPAC sponsors.

- Downside protection: The capital raised through an IPO is held in a trust account pending approval of the acquisition, and a redemption option is available for investors. The trust account provides a minimum liquidation value per share, which serves as downside risk protection.

However, investors should also be aware of the risks involved when investing in SPACs.

- It’s a blank check company: A SPAC possesses no assets other than the sponsors’ professed “know-how.” The investor is betting on the sponsors to make a wise acquisition. Presumably, an investor would not invest in a SPAC without confidence in SPAC sponsors and their prior track record of investment success.

- Incentive misalignment – time pressure: The 24-month timeline imposed on the sponsors to acquire a target puts SPAC sponsors under significant pressure. Unlike investors, SPAC sponsors are not entitled to receive any interest back if the acquisition does not occur. This structure creates an almost “do-or-die” situation for sponsors. Thus, SPAC sponsors have every incentive to acquire a target within the requisite period.

- Incentive misalignment – valuation: Since the target company must comprise over 80% of the trust account asset, the SPAC’s sponsors may overpay for the target company to get the deal done.

Summary

A typical SPAC goes through three stages during its life cycle: IPO, seeking a target and business combination (de-SPAC). When investing in SPACs, investors gain access to private equity-like opportunities with downside protection. However, investors should also be aware that SPACs possess no assets, and sponsors’ interests may not align with those of the investors. In the next blog, we will analyze SPACs’ liquidity and historical performance.

Reference:

Lewellen, S. (2009). SPACs as an Asset Class. Available at SSRN 1284999 http://ssrn.com/abstract=1284999

1 The specific terms of listing price and warrant depend on the individual IPO prospectus.

2 https://www.nasdaq.com/articles/your-guide-to-analyzing-spac-investments-2021-01-31/

3 https://www.sec.gov/rules/sro/nasdaq/2020/34-90245.pdf.

4 NASDAQ allows 36 months for SPACs to complete business combination; SPACs are also allowed to extend this deadline per shareholders’ approval.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

This post was originally published at the official blog of S&P Dow Jones Indices, The Indexology Blog.