by Jørgen Kjærsgaard, AllianceBernstein

Credit markets have staged an epic rebound from the depths of March 2020. But in a low-growth, low-yield world, we believe there may be more room to run in 2021.

The COVID-19 pandemic has had tragic results for humanity and has hammered businesses globally. Widespread lockdowns and travel bans have wiped out earnings for many industries worldwide, and developed-market economies may not regain fourth-quarter 2019 real GDP levels until 2022. That’s a sobering picture. But for global credit markets, as we look forward into 2021, we see several factors that will likely prove positive.

Of course, the path to economic recovery will be bumpy and uneven. For investors, we believe a nimble, selective approach will be especially important to grasp the opportunities presented by an evolving corporate debt landscape.

Coronavirus Pandemic Reshapes Credit Markets

Enforced lockdowns have triggered an increase in the level of credit defaults and led to a wave of rating downgrades from investment-grade to high-yield status. This has changed the structure of credit markets, removing the weakest borrowers from both investment grade and high yield, while increasing the quality, size and depth of the high-yield market. Both markets are healthier for it and present opportunities across the credit spectrum for investors searching for the optimal balance.

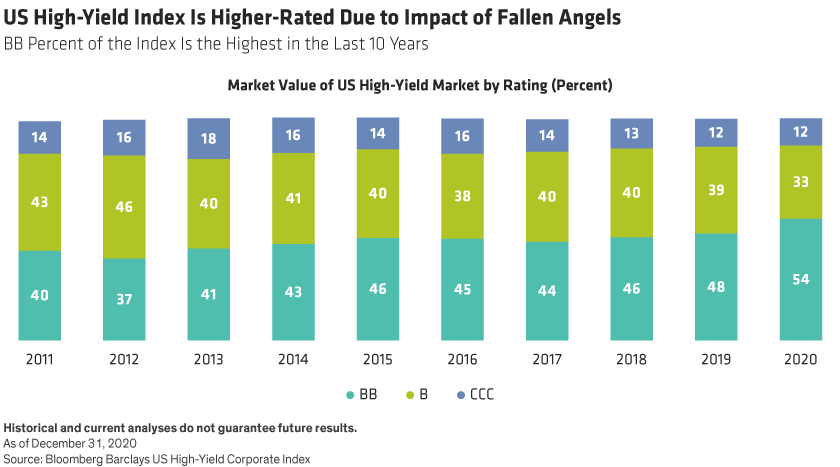

The migration of “fallen angels” out of investment grade has materially increased the size of US and European high-yield markets, by around US$200 billion and €50 billion respectively. These fallen angels include some of the best-known and widely respected names in the business world, including Ford, Rolls-Royce and Carnival.

Their arrival has significantly improved the overall quality of the high-yield index, increasing the share of BB-rated credits in the US from around 48% pre-COVID-19 to 54% (Display, below). In Europe, this new influx of debt also adds depth to the market and consists mainly of “non-callable” bonds which cannot be redeemed early by the issuer. These factors are attractive to longer-term investors such as pension funds and insurance companies, and so increase the demand for high-yield assets.

Fundamentals Are Supportive

We believe credit defaults are likely to peak at around 6% in the US and 4% in Europe, which is in line with consensus forecasts. During last year’s lockdowns we saw the weaker credits removed from indices through default. But we believe we’re now through the worst and we expect future default rates to trend lower as economies recover.

Despite corporate leverage reaching record levels of 2.9x in US investment-grade, 5.3x in US high-yield, and 6.3x in euro high-yield markets (as of June 30, 2020), we’re not overly concerned by the absolute level of borrowings. While these numbers look elevated versus history, we think the solvency picture is stable, for three reasons.

First, 2020 saw record new issuance, strengthening companies’ liquidity buffers and pushing out the maturity dates of their bonds. This should give businesses more time before they need to issue further debt, and help them ride out the rest of the crisis and beyond. Second, thanks to record-low interest rates, debt service costs have fallen, despite actual debt levels rising. Third, we expect that earnings will substantially rebound across most of the economy. Although a few business sectors will continue to struggle, most issuers should be able to generate incremental cash flow after paying interest on their bonds—despite the earnings setbacks caused by further lockdowns.

Technical Factors Strongly Favorable

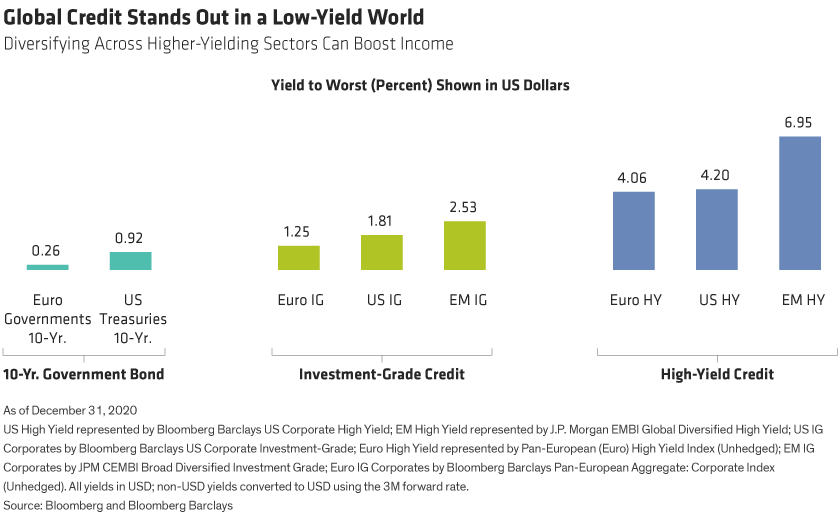

We expect supply to shrink in 2021, given 2020’s record volume of issuance. But demand for credit will likely remain buoyant, thanks to attractive yields, eager income-seeking investors and a globally low-yield environment (Display).

In addition, government and central bank support—such as low-interest-rate policies and securities purchase programs—has aided market liquidity and financing for businesses during the crisis. We expect rates to remain low well into the future and many support programs, including fiscal stimulus, to be extended through the recovery. This should provide continued backing for credit markets.

Attractive Valuations Can Be Found, but Be Selective

In developed markets, corporate credit spreads have already recovered materially, and now sit marginally above pre-COVID-19 levels. That might seem surprising at this stage in the recovery. But because credit migration and defaults have led to higher quality indices, historical comparisons are less reliable. In fact, after adjusting for quality, credit is priced at more compelling spreads today than at this point in a traditional recovery cycle.

The key is to be selective. Spread dispersion across and within sectors will remain significant. But it will take deep fundamental analysis to identify opportunities successfully and to sift winners from losers.

For instance, companies running with higher leverage and exposed business models, such as car rentals, will likely continue to struggle. On the other hand, select travel and cyclical credits trading at attractive premiums may offer better opportunities. We look for companies with stronger balance sheets, more durable businesses, disciplined financial policies, and demonstrable access to capital markets, both in the form of equity injections and debt issuance.

Lastly, environmental, social and governance (ESG) factors are becoming increasingly important to both investors and the companies they invest in. Companies with high ESG scores are more highly valued, and those with poor ESG scores are having increasing difficulty refinancing debt. This trend has accelerated in 2020, and we expect it to become more pronounced in the coming months and years.

Credit Opportunities Across Regions

Global credit investors can find opportunities across regions because of disparities in yield and differing exposure to economic recovery.

For example, among investment-grade credits, pockets of emerging-market corporates offer attractive yield advantages over euro-area and US markets. Emerging markets are also poised to get a bigger lift from the arrival of vaccines and a possible early recovery.

Regional differences are also apparent in the extent of support from central banks. So when considering opportunities, investors need to balance the potential benefits of economic recovery against the powerful advantage of central bank purchase programs.

Across high-yield markets, US credits may benefit from a bigger economic rebound, but euro-area high yield enjoys a robust level of support from the European Central Bank (ECB), as well as a higher aggregate credit quality and lower exposure to the volatile energy sector.

Currently, within US investment-grade, we continue to see value in select BBB-rated credits. In euro high yield, we think BB-rated debt and some banks’ Additional Tier 1 (AT1) subordinated bonds look compelling. For the larger US high-yield market, we see opportunity in select B and CCC names.

Emerging-market high-yield corporates require caution. Special consideration should be given to companies with high transparency and visibility into future cash flows, in our view. Current valuations in Asian credits look particularly attractive. Here, spreads are currently near their historical highs while underlying credit fundamentals are largely stable.

Watchpoints Unlikely to Mar the Outlook for Credit

The path ahead may contain surprises and challenges, but we see plenty of opportunity in credit markets in view of continuing easy monetary policy, committed fiscal stimulus and improving levels of economic activity.

We believe that active multi-sector approaches provide the best risk-adjusted potential returns, especially during times of heightened uncertainty. Such strategies can pair interest-rate risk with more diverse sources of credit risk—including securitized and emerging-market debt—as well as the full range of developed-market corporate credit.

In a world with over US$17 trillion of negative-yielding debt, pockets of the global credit market stand out as a sizeable, investable group of assets offering attractive levels of yield. With fundamentals and valuations supportive, and technicals very favorable, global credit may indeed be in the sweet spot for 2021.

Sources: Bank of America, Bloomberg Barclays, Morgan Stanley, Standard & Poors, AllianceBernstein (AB)

Jorgen Kjaersgaard is Co-Head of European Fixed Income and Director of European and Global Credit, Tiffanie Wong is Director of US Investment-Grade Credit, and Will Smith is Director of US High Yield, all at AB.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time. AllianceBernstein Limited is authorized and regulated by the Financial Conduct Authority in the United Kingdom.

This post was first published at the official blog of AllianceBernstein..