by Brian S. Wesbury - Chief Economist, Robert Stein, CFA – Deputy Chief Economist, and Bryce Gill - Economist, First Trust Portfolios

Nobody expected to see a rate change from this week's FOMC meetings, but interest remained high as the market awaited the latest Fed forecasts on where they see the US economy headed from here. And the updates to the Fed outlook were notable. GDP and inflation projections were revised higher, while the unemployment rate forecasts moved lower, all signaling a stronger economic recovery than the Fed believed possible earlier this year.

How far have their forecasts come? Back in June, the Fed forecast the US economy would see a decline of 6.5% in real GDP in 2020, now they are targeting a decline of 2.4%. The year-end unemployment rate was projected at 9.3% back in June, but is now seen at (the current level of) 6.7% And future year outlooks have improved of late as well, both for economic growth and unemployment, which is now forecast to fall to 5.0% in 2021 and move below 4.0% in 2023. You may be tempted to think that the improved outlook may change the Fed's path for interest rates into the future, but that is the one area in today's report that remained unchanged.

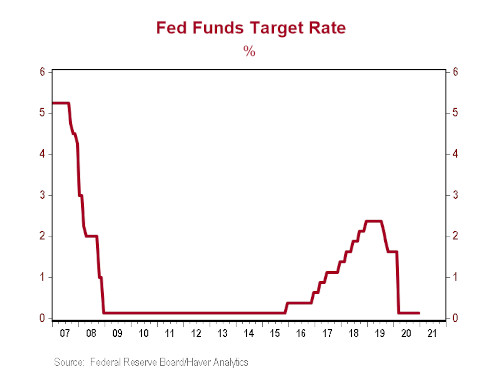

The Federal Reserve has no plans to move rates in 2021, 2022, or 2023 (which is as far out as they forecast in their projection materials). Only one of seventeen voting members believes any change in rates would be appropriate in 2022, while five believe that rates could move higher in 2023. During Chair Powell's press conference, the question arose about supply chain disruptions and the upward pressure those may put on inflation as the economy gets back to normal over the next twelve months, and while Powell acknowledged that may indeed lead to a pickup in prices, the question for the Fed is if those rising prices will be persistent. The Fed is basically saying, "We won't believe it until we've seen it...for a while." In other words, the Fed believes inflation will be transitory and won't force its hand on a rate hike for at least the next few years.

Within the Fed Statement itself, the main notable change to the December release came from a clarification that the Fed plans to continue purchasing at least $80 billion per month of treasury securities and $40 billion per month of mortgage backed securities until "substantial further progress has been made toward the Committee's maximum employment and price stability goals." Again, the press conference brought additional light on this topic. The Fed believes (and we agree), that we still have a ways to go before the labor market has healed to where it was before COVID-19 reared its ugly head. Where we differ is in our belief that inflation will rise – and stay – above the Fed's target sooner and longer than it currently expects. That, in turn, would lead the Fed to raise rates before their post-2023 estimation. In the meantime, artificially low interest rates are a boon for stocks, which we believe remain undervalued, and poised for continued growth in the years ahead.

Click here for a PDF version

Copyright © First Trust Portfolios