by Liz Ann Sonders, Senior Vice President, Chief Investment Strategist, Charles Schwab & Co

Key Points

- The labor market continues to heal; but the level of weakness remains unprecedented.

- Hard-hit industries brought workers back in July, but the impact of virus-related rolling shutdowns could reverse some of that improvement.

- Short-term, Congress is negotiating another income-replacement package; longer term, employment sectors in growth mode employ a larger share of the U.S. workforce than those in contraction mode.

The July jobs report was a pleasant surprise, but not without caveats. Nonfarm payrolls increased by 1.76 million; with 1.46 million within the private sector, and 301k within the government sector. The consensus expectation for overall payrolls was 1.48 million. The separate household survey showed the addition of 1.35 million jobs—coupled with a 62k decline in the labor force, it brought the unemployment rate down from 11.1% in June to 10.2% in July. The broadest measure of unemployment—the U6, which includes discouraged workers no longer seeking employment and part-time workers seeking full-time employment—fell from 18% in June to 16.5% in July.

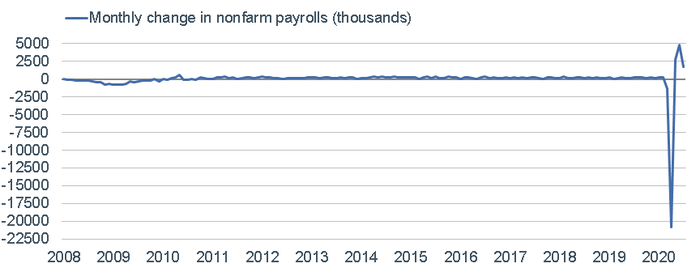

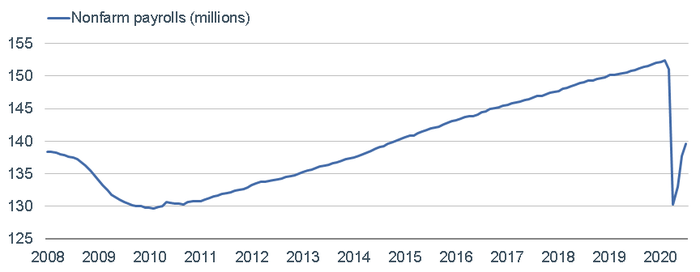

“V” in change, but not level

As you can see in the charts below, the monthly change in nonfarm payrolls looks like more than a complete recovery from the COVID-19 implosion; however, in level terms, there remains a long way to go. There are still 31 million people receiving some form of unemployment insurance benefits.

Rebound in Payrolls’ Change But Not Level

Source: Charles Schwab, Bloomberg, as of 7/31/2020.

In total, there have been 9.3 million jobs added over the past three months; but that is less than half of the jobs lost since employment peaked in February. The employment diffusion index rolled over in July—from 75% in June to 61.4% in July—but remains at a relatively healthy level. This means that the majority of industries are hiring. However, hours worked also rolled over; suggesting companies had to cut hours last month due to the virus’ impacts, even if they didn’t lay off additional workers.

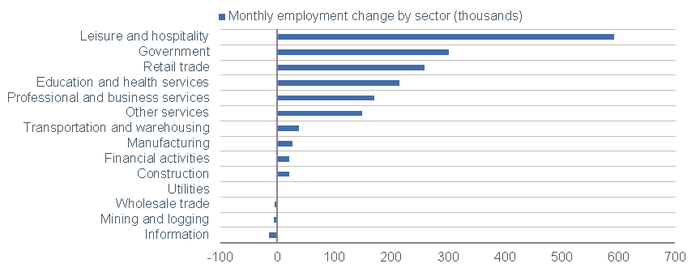

Most of the jobs gained in July were within the services sector; with only 39k added in the goods producing sector. In particular, leisure/hospitality—most damaged from the pandemic—saw the largest gains, followed by government, retail trade and education/health services (see chart below). In terms of government jobs, the surge was partly driven by seasonal adjustment factors. Education payrolls fell earlier in the year due to the pandemic; so the seasonal adjustment resulted in July’s massive surge.

Payroll Gains by Sector

Source: Charles Schwab, Bloomberg, as of 7/31/2020.

Will the real unemployment rate please stand up?

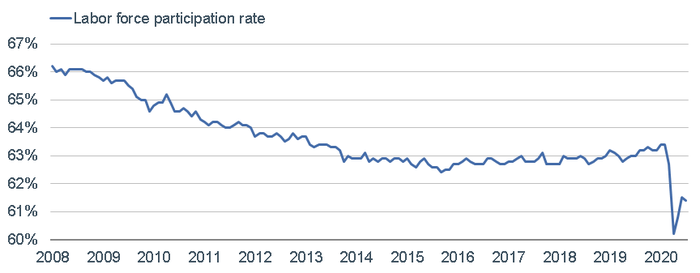

As noted above, the labor force participation rate ticked down by 62k in July, after rising by 3.5 million throughout May and June (see chart below). The BLS reported that a number of workers continue to be mistakenly classified as employed, rather than unemployed on temporary layoff. Without that distortion, the BLS notes the unemployment rate would have been around 11%. Ned Davis Research has been highlighting two alternative measures; including the employment-population ratio and the pool of available labor. The “augmented unemployment rate” fell in July like the headline reading; however, it fell from a much-higher 15.4% to a still-high 14.4%.

Labor Force Participation Rate Ticks Back Down

Source: Charles Schwab, Bloomberg, as of 7/31/2020.

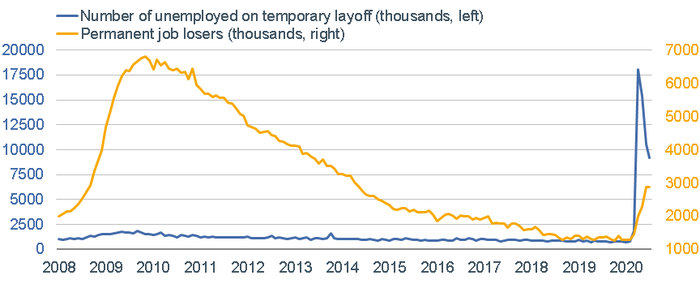

For now, most of the unemployed continue to report themselves as on temporary layoff; with the 1.8% of workers permanently losing their jobs in July unchanged from June’s level (and below the peak of 4.4% seen after the Global Financial Crisis). The direction of these measures, as seen in the chart below, is key to watch over the next several months—especially in light of the recent virus’ surge impact on economic activity.

Temporary Layoffs Down, Permanent Job Losses Up

Source: Charles Schwab, Bloomberg, as of 7/31/2020.

Long-term unemployed expanding

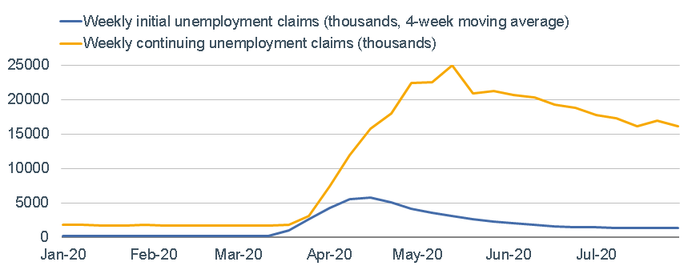

Another caveat to the better-than-expected labor market headlines is the growing number of longer-term unemployed. As you can see in the chart below, continuing unemployment claims remain historically-high. In addition, relative to total unemployed, those out of work for at least 15 weeks jumped to 48.8% in July vs. 18.7% in June; increasing the duration of unemployment. The flows from employed to unemployed and back again have been unprecedented. About 2.2% of the workforce went from employed to unemployed in July and 3.2% went from unemployed to employed. In contrast, during the Global Financial Crisis, the worst month for either was 1.8% of the workforce.

Continuing Claims Remain Extremely High

Source: Charles Schwab, Bloomberg. Initial claims as of 8/1/2020. Continuing claims as of 7/25/2020.

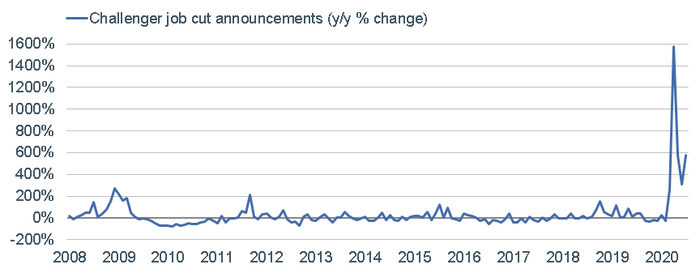

Unemployment claims are, always and now, a leading economic indicator. But there are other labor market indicators that even lead claims, including job cut announcements. July’s announced job cuts, measured by Challenger, Gray & Christmas, jumped 576% year-over-year vs. 305% in June. It was the third-largest on record (with the other two in April and May); with the majority coming from entertainment/leisure and transportation.

Job Cuts Accelerating Again

Source: Charles Schwab, Bloomberg, as of 7/31/2020.

Income replacement has been key to spending

Looking forward, clearly the health of the labor market will be tied to the health of the economy; especially given the hefty weight of consumer spending in the U.S. economy. In the pre-pandemic era, spending among unemployment benefit recipients fell by about 7% in response to unemployment, because typical benefits replaced only a portion of lost earnings. Since the CARES Act was passed in March however, the additional $600 per week of supplemental payments replaced lost earnings by more than 100% for two-thirds of unemployed workers eligible (as per JPMorgan Chase Institute calculations). How the negotiations in Congress over the next stimulus package—and whether there will be a renewal of supplemental unemployment insurance (UI), and at what level—will be key to assessing the impact on the economy.

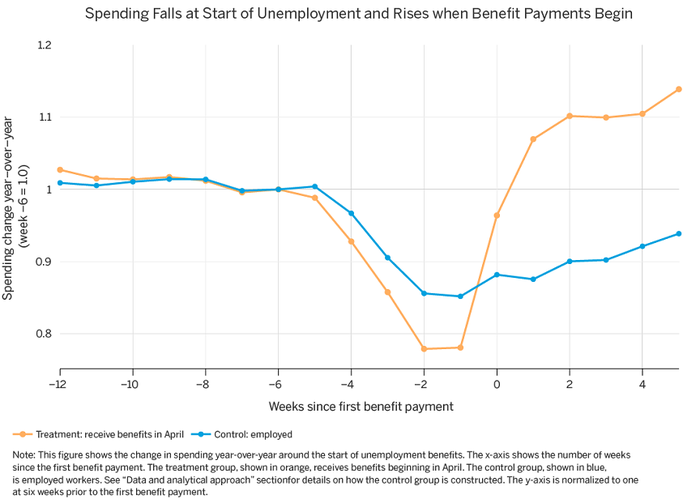

In this year’s second quarter, nominal personal income grew at a 32.6% annualized rate—a record high since data began in 1947. In contrast, nominal employee compensation declined at a -24.6% annualized rate, which was also a record. The yawning spread has been filled by the income replacement associated with the CARES Act $600/week supplement. In terms of its economic benefit, as you can see below, aggregate spending of the employed decreased less than the spending of the unemployed during the initial months of the pandemic. However, the spending of unemployment benefit recipients has not only increased more since then; it’s now well above where it was before the additional benefits kicked in; while spending by the employed remains lower.

Source: JPMorgan Chase Institute (https://institute.jpmorganchase.com/institute/research/labor-markets/unemployment-insurance-covid19-pandemic.

As noted in the JPMorgan Chase Institute analysis, “unemployment insurance (UI), at its current unprecedented scale and level, is not only insuring households against the hardships associated with job loss but also stimulating aggregate demand.” They conclude that “given that UI currently represents around 15% of total wages, allowing the $600 supplement to [have] expire[d] at the end of July 2020 could cause substantial declines in aggregate demand and potentially negative effects on the macro-economy.”

Congress still wrangling

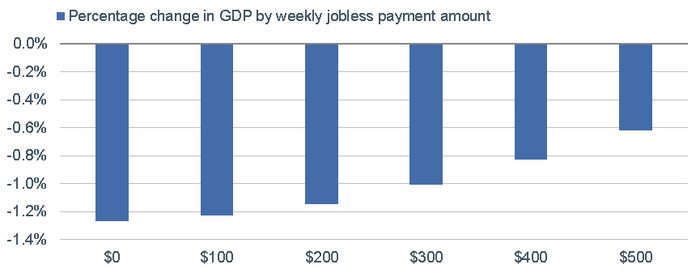

This past Saturday, President Trump announced a few executive actions—being questioned in terms of legal authority—which includes a $400/week “top up” to UI benefits. Whether there is ultimately a package put together through normal Congressional channels, the level of those UI supplemental benefits is a factor in how the economy is likely to fare. The chart below shows the estimated change in 2020’s gross domestic product (GDP) based on the level of UI supplement.

Impact on Economy of Supplemental UI Benefits

Source: Charles Schwab, Wall Street Journal, Moody's Analytics, as of 8/6/2020. Percentage drop is estimated change through the end of 2020, based on size of enhanced payments.

Regardless of what’s ironed out by Congress, the U.S. economy and its labor market has suffered significant hardship; the ripple effects of which have yet to fully unfold. Bankruptcies are on the rise; and although in the aggregate, U.S. virus cases have leveled off, there are significant accelerations in the Midwest; as well as in parts of Europe and Australia.

Reasons for less doom and gloom

Let me conclude with a longer-term optimistic thought. There are a few somewhat-obvious employment sectors that are now under extreme pressure; including bricks-and-mortar retailers, restaurants/bars, recreation (including sports/concert viewings) and air travel. Collectively, they employed about 15% of the workforce pre-pandemic. Conversely, there are employment sectors likely to strengthen or even flourish; including grocery stores, technology, health care, manufacturing and residential construction. Currently, they employ about 32% of the workforce. (Estimates are courtesy of my friend Nancy Lazar and her team at Cornerstone Macro.)

I do believe we are in the early stages of a secular shift in the drivers of the U.S. economy; from heavily-consumer spending/services oriented, to more investment-driven (technology, health care, housing and infrastructure). The good news is those areas represent a larger share of employment than the aforementioned areas under most pressure. Secular transitions are more ocean liner than speed boat with regard to how quickly they occur—and they’re not without labor market destruction along the way. But we will get there.

Copyright © Charles Schwab & Co