by Michelle Dunstan, AllianceBernstein

As more companies tap government stimulus funds, more questions are being asked about how the use of taxpayer money may affect shareholders. To answer these questions, investors must assess how corporate behavior and stakeholder engagement will shape a company’s long-term outlook.

Government stimulus is an essential ingredient to combat the recessionary drag of the pandemic. For many companies, stimulus funds provide a cash lifeline that can make the difference between survival and extinction in today’s tough environment.

Complex Questions for Investors

Yet the provision of public grants or loans also creates questions for investors. Should companies be allowed to draw on taxpayer funds if they didn’t manage their capital responsibly before the crisis? Will shareholders get hurt if a company cancels dividends to accept public funds? And with dividends and buybacks being scaled back, how should investors evaluate company spending on employee engagement and community outreach during the pandemic?

These questions reflect the first test of the new era of stakeholder capitalism. In 2019, 181 US CEOs signed a declaration stating that their businesses would fully consider all stakeholders, not just shareholders. In the Business Roundtable statement, corporate leaders pledged to support the environmental and social health of communities in which they operate and to embrace sustainable practices. Now, companies face tough capital management decisions to balance business dynamics and shareholder interests with public health considerations and other social issues.

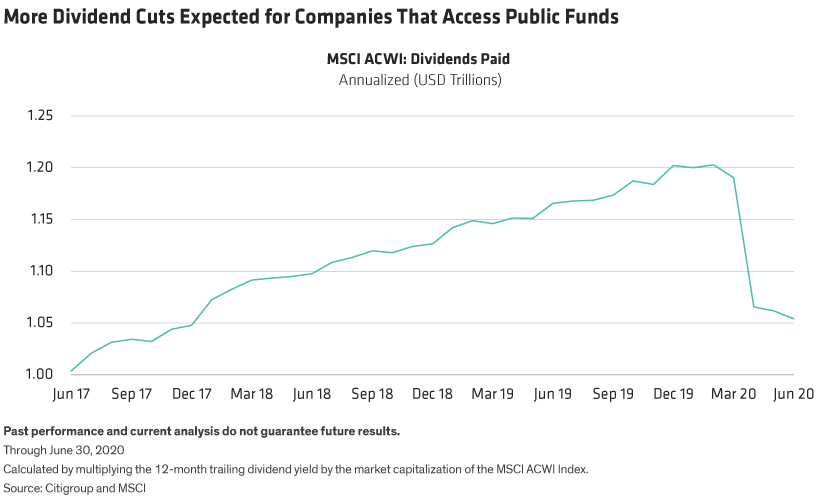

Dividends and Buybacks Are Getting Cut

Shareholder rewards are already under pressure. Dividends paid globally dropped to US$1.05 trillion in June on an annualized basis, a 12% decline from their peak in February (Display). In the US, companies slashed $42.5 billion in dividends during the second quarter of 2020, the biggest cuts since the first quarter of 2009, according to S&P Dow Jones Indices.

Buybacks are also being reconsidered. In the US, S&P 500 companies that contributed to 27% of share repurchases in 2019 have already suspended buyback programs. After the Fed issued guidance in June for large banks to halt buybacks, share repurchases are expected to drop by more than 50% in the second half.

Many companies will face restrictions on dividends and buybacks if they access public funds. Under the CARES Act, US companies that take PPP loans may not pay dividends or buy back shares in the next 12 months or until there are no outstanding loan guarantees. The European Central Bank has ordered EU banks to halt dividend payments and buybacks at least until October 2020. And the Bank of England asked large UK lenders to suspend dividends and cash bonuses for senior executives, saying other stakeholders’ interests should come before those of shareholders and management to support the economy.

Evaluating Debt Levels amid Relief Funds

So how should investors evaluate debt levels versus shareholder rewards? We think the following three issues take on added importance today:

-

Default risk—Do solvency concerns and default risk outweigh expected returns? If the answer is yes—with or without access to stimulus—the investment thesis is compromised. -

Reinvestment rate—Is the company investing enough for business growth? Reinvestment is always key to forecasting future return potential, especially today, when many companies face a cash crunch that constrains their ability to invest for the future. -

Shareholder rewards—Are dividend and buyback levels reasonable in light of the company’s default risk and reinvestment rates? Getting the balance right is tricky in the best of times. Today, public funds add more variables to consider.

For these three issues, the big question is whether the company took on debt responsibly. For example, if a company expects positive cash flow or growth rates while taking on debt, it may make sense to continue paying dividends; this keeps the company attractive to investors for future capital raising. In some cases, even buybacks could be a responsible way to enhance shareholder value if the company doesn’t have clear investment areas for further growth.

Does this capital allocation analysis change in COVID-19? We believe the underlying framework is the same as in normal times, and should be based on an approach that integrates environmental, social and governance (ESG) issues with fundamental security analysis. Yet new variables—in particular, company liquidity—must be considered to identify whether shareholder value is at risk from poor capital management.

Governance and Executive Pay Matter

Given the complexities, proper governance oversight of capital allocation is essential. In addition to traditional fundamental analysis of a company’s financial health, investors should engage with management to discuss how the board is involved in overseeing capital allocation decisions.

Executive pay also deserves attention. We’re wary of executives whose compensation packages were heavily influenced by buybacks and dividend payments, while heavy debts were taken. Investors should look for transparent pay mechanisms based on clearly defined financial performance targets and ESG metrics, in our view. This allows investors to hold senior management accountable for maintaining a sustainable business over the long term. These can include, for example, targets for improving injury rates among employees, diversity goals or carbon emissions within a defined timeline.

Engaging with Employees and Communities

Employees are essential stakeholders for companies to create a successful business. During the pandemic, employee engagement efforts should provide workers with a sustainable labor environment, health insurance and sick leave. Similarly, investors should look for clear communication on timelines for the return of furloughed employees.

Many companies are also supporting local communities during the pandemic. Some CEOs have even pledged to take a pay cut or to donate a portion of their salaries to communities in need.

This isn’t just a moral imperative. Companies that get employee and community engagement right will be better placed to meet business goals in the long run.

Engagement efforts like these might cost more in the short term. Dividends and buybacks may also be compromised. But long-term investors are focused on sustainability and resiliency. Companies that pay more now to support their employees and communities are also setting the stage for stronger long-term performance in a recovery by maintaining a motivated workforce and cultivating customer loyalty. Similarly, companies that responsibly access public stimulus funds—while maintaining reasonable debt levels and staying focused on long-term investment needs—will be better prepared to rejuvenate their businesses when economic conditions improve.

Michelle Dunstan is Global Head—Responsible Investing; Portfolio Manager—Global ESG Improvers Strategy at AllianceBernstein (AB)

Diana Lee is Director of Corporate Governance at AB

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

This post was first published at the official blog of AllianceBernstein..