by Lance Roberts, RIA

Currently, the Fed is injecting liquidity into the markets and economy at a record pace. While liquidity does have positive short-term benefits, is the Fed walking into a trap?

The Unseen

Over the last decade, the Federal Reserve, and Central Banks globally, have engaged in never-ending “emergency measures” to support asset markets. While the stated goal was that such actions were to foster full employment and price stability, there has been little evidence of success.

The chart below shows the expansion of the Fed’s balance sheet and its effective “return on investment” on various aspects of the economy. No matter how you analyze it, the “effective ROI” has been lousy.

These are the unseen consequences of the Fed’s monetary policies.

The Seen

The only reason Central Bank liquidity “seems” to be a success is when viewed through the lens of the stock market. Through the end of the Q1-2020, using quarterly data, the stock market has returned almost 127.79% from the 2007 peak. Such is more than 3x the growth in GDP and 6.5x the increase in corporate revenue. (I have used SALES growth in the chart below as it is what happens at the top line of income statements and is not AS subject to manipulation.)

Unfortunately, the “wealth effect” impact has only benefited a relatively small percentage of the overall economy.

While in the short-term ongoing monetary interventions may appear to be “risk-free,” in the longer-term, the Fed may be getting trapped.

The Fed Liquidity Trap

One of those traps is a “liquidity trap,” which we have discussed previously. Here is the definition:

“When injections of cash into the private banking system by a central bank fail to lower interest rates and fail to stimulate economic growth. A liquidity trap occurs when people hoard cash because they expect an adverse event such as deflation, insufficient aggregate demand, or war.

Signature characteristics of a liquidity trap are short-term interest rates remain near zero. Furthermore, fluctuations in the monetary base fail to translate into fluctuations in general price levels.”

Pay particular attention to the last sentence.

Even though the Fed tried to increase rates in 2017-2018, the tightening of monetary policy led to negative economic consequences. In response, the Fed lowered rates back to the zero bound. (Recently, Fed Fund futures have been teasing “negative” rates.)

Inflation Conundrum

What monetary policy did not do was lead to “general fluctuations in price levels.” Despite the annual call by the Fed of higher rates of inflation and economic growth, the realization of those goals remains elusive.

It is difficult to attribute the decline in interest rates and inflation to monetary policies when the long-term trend has been negative for decades. As I discussed in last week’s MacroView:

“The high correlation between the three major components of our economic composite (inflation, economic and wage growth) and the level of interest rates is not surprising. Interest rates are not just a function of the investment market, but rather the level of ‘demand’ for capital in the economy.

When the economy is expanding organically, the demand for capital rises as businesses increase production to meet rising demand. Increased production leads to higher wages, which in turn fosters more aggregate demand. As consumption increases, so does the ability for producers to charge higher prices (inflation) and for lenders to increase borrowing costs.

(Currently, we do not have the type of inflation that leads to more robust economic growth, just increases in the costs of living that saps consumer spending – Rent, Insurance, Health Care)”

As stated, it is not just monetary policy that is responsible for the long-term degradation in economic growth. It is also the ongoing increase in debts and deficits which are supported by the Fed’s actions.

Monetary Velocity Trap

“The velocity of money is important for measuring the rate at which money in circulation is used for purchasing goods and services. Velocity is useful in gauging the health and vitality of the economy. High money velocity is usually associated with a healthy, expanding economy. Low money velocity is usually associated with recessions and contractions.” – Investopedia

There is no evidence the Fed’s “zero interest rate policy” led to robust economic growth via the transactions of goods and services. Monetary velocity has been clear on this point.

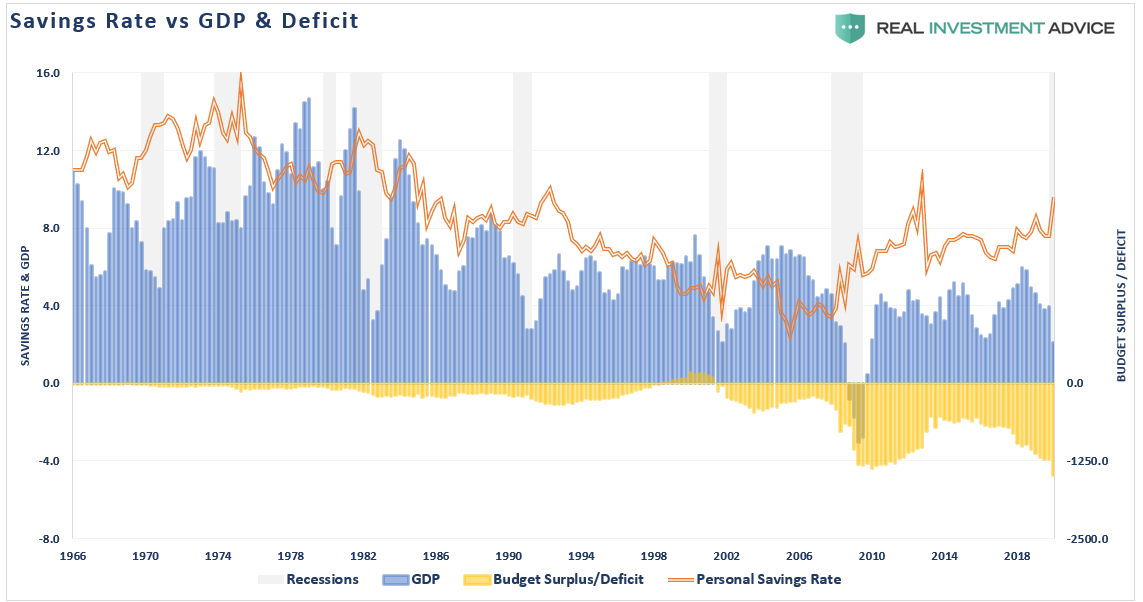

A “liquidity trap” states that people begin hoarding cash in expectation of deflation, lack of aggregate demand, or war.

Well, as discussed in “The Savings Mirage,” we are now officially there.

The issue of monetary velocity and saving rates are critical to the definition of a “liquidity trap.”

As noted by Treasury&Risk:

“It is hard to overstate the degree to which psychology drives an economy’s shift to deflation. When the prevailing economic mood in a nation changes from optimism to pessimism, participants change. Creditors, debtors, investors, producers, and consumers all change their primary orientation from expansion to conservation. Creditors become more conservative, and slow their lending. Potential debtors become more conservative, and borrow less or not at all.

As investors become more conservative, they commit less money to debt investments. Producers become more conservative and reduce expansion plans. Likewise, consumers become more conservative, and save more and spend less.

These behaviors reduce the velocity of money, which puts downward pressure on prices. Money velocity has already been slowing for years, a classic warning sign that deflation is impending. Now, thanks to the virus-related lockdowns, money velocity has begun to collapse. As widespread pessimism takes hold, expect it to fall even further.”

Deflationary Spiral

Such is the biggest problem for the Fed and one that monetary policy cannot fix. Deflationary “psychology” is a very hard cycle to break, and one the Fed has been clearly fearful of over the last decade.

“In addition to the psychological drivers, there are structural underpinnings of deflation as well. A financial system’s ability to sustain increasing levels of credit rests upon a vibrant economy. A high-debt situation becomes unsustainable when the rate of economic growth falls beneath the prevailing rate of interest owed.

As the slowing economy reduces borrowers’ ability to pay what they owe. In turn, creditors may refuse to underwrite interest payments on the existing debt by extending even more credit. When the burden becomes too great for the economy to support, defaults rise. Moreover, fear of defaults prompts creditors to reduce lending even further.”

For the last four decades is every time monetary policy tightens, it has led to an economic slowdown, or worse. The reason is that a heavily debt-burdened economy can’t support higher rates.

The relevance of debt growth versus economic growth is all too evident. Over the last decade, it has taken an ever-increasing amount of debt to generate $1 of economic growth.

In other words, without debt, there has been no organic economic growth.

Running ongoing budget deficits that fund unproductive growth is not economically sustainable long-term.

While it may appear such accommodative policies aid in economic stabilization, yet it was lower interest rates increasing the use of leverage. The consequence was the erosion of economic growth and deflation as dollars were diverted from productive investment into debt service.

Unfortunately, the Fed has no other options.

The Fed Inflation Trap

While “deflation” is the overarching threat longer-term, the Fed is also potentially confronted by a shorter-term “inflationary” threat.

The financial markets have currently priced in perfection. A “V-shaped” recovery back to pre-recessionary norms, no secondary outbreak of the virus, and a vaccine. If such does turn out to be the case, the Federal Reserve will potentially have a huge problem.

The “unlimited QE” bazooka is dependent on the Fed needing to monetize the deficit to support economic growth. However, if the goals of full employment and economic growth quickly come to fruition, the Fed will face an “inflationary surge.”

The “reopening” risk compounds further with the massive surge in the money supply due to the various programs which have sent money directly to businesses and households. Historically speaking, surges in the money supply lead inflationary pressures by about 9-months.

Should such an outcome occur, it will push the Fed into a very tight corner. The surge in inflation will limit the ability to continue “unlimited QE” without further exacerbating inflation. Unfortunately, if they don’t “monetize” the deficit through the “QE” program, interest rates will surge as the Treasury issues more debt.

It’s a no-win situation for the Fed.

The End Game Cometh

Over the last 40-years, the U.S. economy has engaged in increasing levels of deficit spending without the results promised by MMT.

There is also a cost to MMT we have yet to hear about from its proponents.

The value of the dollar, like any commodity, rises and falls as the supply of dollars change. If the government suddenly doubled the money supply, one dollar would still be worth one dollar, but it would only buy half of what it would have purchased before their action.

Such is the flaw MMT supporters do not address.

Modern Monetary Theory (MMT) is not a free lunch.

MMT is paid for by reducing the value of the dollar and ergo your purchasing power. It is a hidden tax paid by everyone holding dollars. The problem, as Michael Lebowitz outlined in Two Percent for the One Percent, inflation tends to harm the poor and middle class while benefiting the wealthy.

Such is why the wealth gap is more pervasive than ever. Currently, the Top 10% of income earners own nearly 87% of the stock market. The rest are just struggling to make ends meet.

As I stated above, the U.S. has been running MMT for the last three decades and the only result is social inequality, disappointment, frustration, and increasing demands for socialistic policies.

It is all just as you would expect from such a theory put into practice, and history is replete with countries that have attempted the same. Currently, the limits of profligate spending in Washington has not been reached, and the end of this particular debt story is yet to be written.

But, it eventually will be.

Copyright © RIA