by Alessio De Longis, Senior Portfolio Manager, Invesco Investment Solutions, Invesco Canada

Our macro regime framework continues to signal that the global economy and all its major regions and countries are in a contraction regime. As widely expected, the economic data are beginning to reflect the disruption caused by quarantines and lockdowns, resulting in a significant deterioration in our leading economic indicators, which we expect to continue for some time. While global market sentiment has stabilized over the past month, it remains in a downward trend, suggesting markets are still expecting downward revisions to global growth expectations. As previously discussed, we believe this macro environment warrants a defensive portfolio posture. We have not made major changes to our asset allocation and continue to favour an overweight exposure in investment grade credit and defensive equity factors.

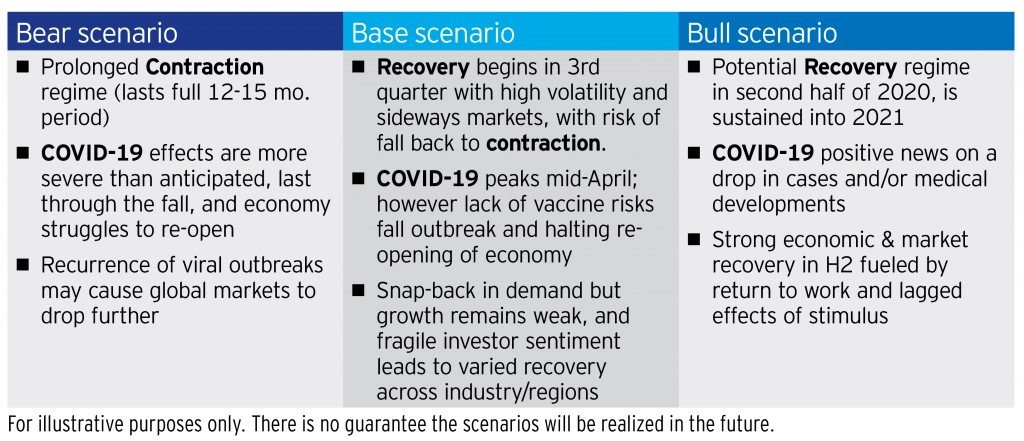

This month we investigate the potential paths forward for the global economy and the likely evolution of our macro regime framework over the next twelve months, conditional on the hypothetical evolution of the Covid-19 pandemic. While it is impossible to make predictions on the medical front, we focus our attention on possible scenarios pertaining to the duration of the pandemic, and how its impact on economic data and growth expectations may drive our regime framework. A brief narrative of three hypothetical scenarios is illustrated in Figure 1. Since our investment process is geared towards adjusting to the changing economic environment, our objective is not to identify the most likely scenario for the next twelve months and position the portfolio accordingly. Instead, we want to evaluate the most likely range of market outcomes, their associated risks, and investment implications.

Figure 1: Three hypothetical scenarios for how the pandemic may unfold

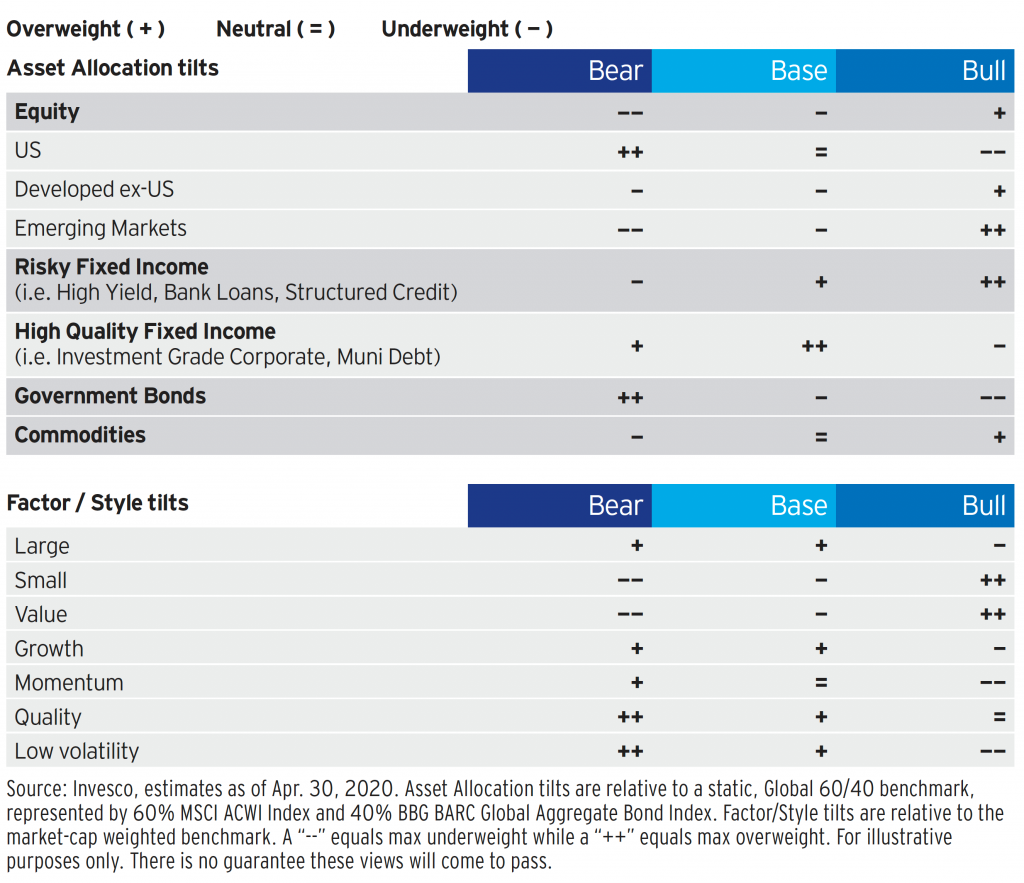

Under these three scenarios, we expect our global framework to oscillate between a recovery and a contraction regime, given the economy today is in a below-trend environment. Next, we outline our tactical asset allocation, style, and factor views for each scenario, as summarized in Figure 2.

Bear scenario: We would expect broad-based risk aversion and outperformance of (relatively) defensive assets. In this case, investors may want to consider below average risk expressed via overweight exposures in long-duration government bonds and high-quality credit, favouring U.S. dollar or U.S. dollar-hedged assets given the potential for further U.S. dollar appreciation. Other considerations include underweight riskier credit assets, especially emerging markets (EM) local currency and hard currency debt, or underweight equities, especially in emerging and developed markets ex-U.S. Within equities, we would favour. growth over value, large caps over small caps, and defensive factors such as quality, low volatility and momentum.

Base scenario: We would expect sideways markets with alternating bouts of volatility. In this case, investors may want to consider average risk exposure, overweighting credit assets through an underweight position in equities and government bonds. Within fixed income, hold an overweight position through high-quality credit – such as investment grade corporate and muni debt – or a combination of riskier credit (i.e. high yield) and long-dated, longer duration government bonds, while reducing exposure in short- and medium-term government bond maturities. Within equities, we may favour. U.S. equities over developed ex-U.S. and emerging markets, growth over value, large caps over small caps, and defensive factors such as quality and low volatility.

Bull scenario: We would expect broad-based outperformance in cyclical and risky asset classes. In this case, investors may want to consider an above average risk posture, expressed via overweight exposures to riskier credit assets and equities and underweight exposures to government bonds and high-quality credit. Within credit, we favour. high yield, structured credit, EM hard currency and local currency debt with the expectation that U.S. dollar depreciates. In equities, we may favour. emerging markets and developed markets ex-U.S. over U.S. equities, and cyclical style and factor exposures, including a preference for value over growth, small caps over large caps, and underweight positions in factors at risk of short-term reversal effects such as low volatility and momentum.

Figure 2: Three hypothetical scenario tilts

Our analysis is an over-simplification of what we think is likely to occur. There may be several unexpected developments, related or unrelated to Covid-19, which may affect these scenarios and the market response. Nonetheless, from our perspective this type of analysis provides a useful context to think about potential outcomes and design action plans given that, as we described in the past, asset prices tend to experience large and rapid adjustments at the inflection points of a cycle, i.e. during a recession and coming out of it.

This post was first published at the official blog of Invesco Canada.