by Klaus Ingemann, AllianceBernstein

The spread of the COVID-19 virus has blindsided conventional risk models. By understanding what went wrong, investors can develop a more forward-looking approach to risk management that considers multiple scenarios for a highly uncertain market environment.

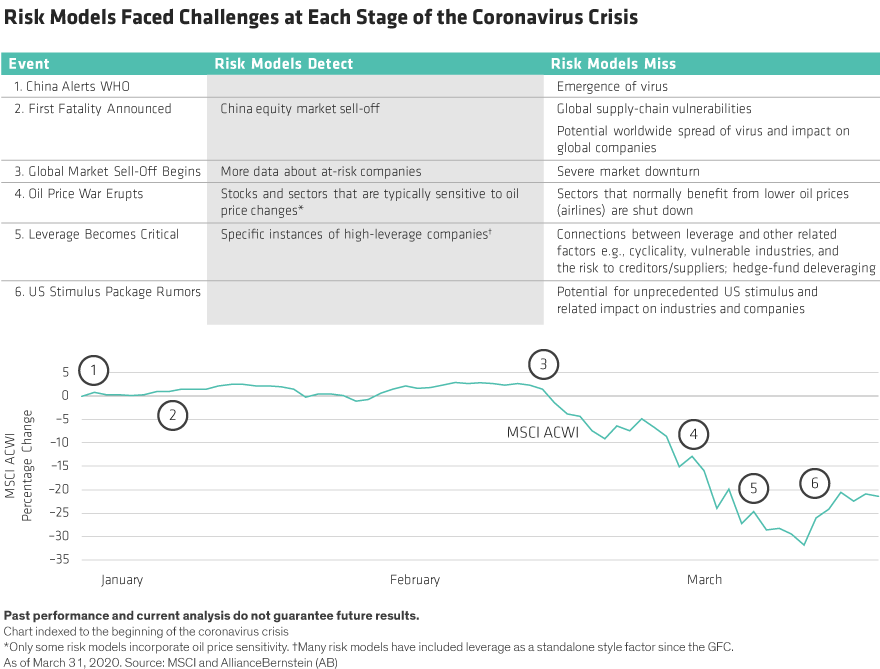

Risk models have become much more sophisticated following the global financial crisis (GFC). But most risk models—which rely predominantly on historical data—struggled to cope with the unprecedented effects of the COVID-19 pandemic. These included: the sudden disruption of global supply chains; the shutdown of cities worldwide; the breakdown of formerly reliable correlations between industry sectors and between investment factors; and the collapse of OPEC+* which triggered violent reactions in energy and stock prices (Display).

No model has been designed to cope with this combination of circumstances. Investors need to understand the strengths and weaknesses of their models to determine whether their signals can be relied upon in crisis situations in general, and through the coronavirus crisis in particular.

Understanding the Basis for Risk Modelling

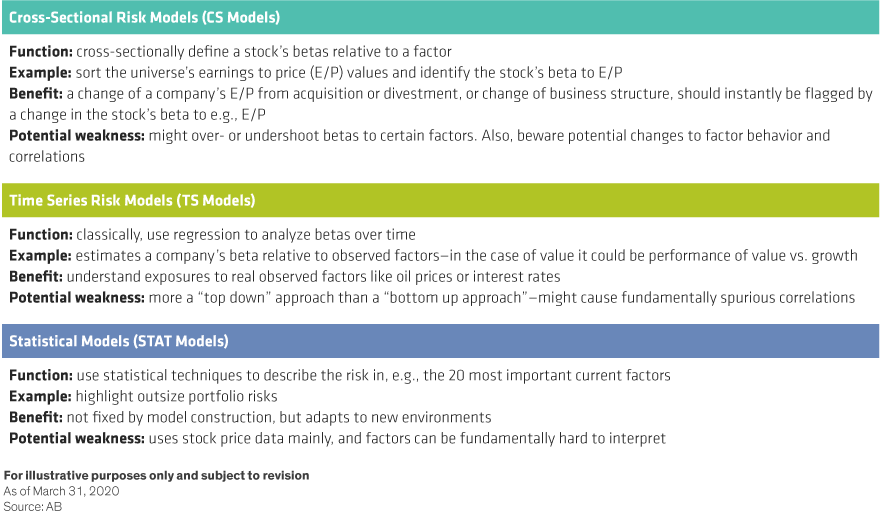

Standard risk models are designed to measure a portfolio’s absolute risk (volatility) or relative risk versus a benchmark (tracking error). They then break down the risk into separate risk factors such as biases to currencies, industries, styles etc., leaving a residual component, which is not explained by pre-determined risk factors. State-of-the-art use of such models allows managers to concentrate risk where they have an edge or skill, and to avoid risk where they don’t. Conventional models typically fall into three categories (Display):

Coronavirus as a Factor

All risk models rely to some extent on factors. But factors can be either static, retaining the same definition through time, or dynamic, meaning their definition changes over time. The coronavirus has a bit of both. As a virus, its characteristics are broadly known and permanent. However, as a disruptive force its impact has evolved through various phases, acting as a dynamic factor that affects many other risks. Each new stage has presented fresh difficulties for risk models. Investors are now struggling to understand unfamiliar risks. These include defined unknowns (like the timescales for social distancing and the limits of policy responses to support world economies) and uncertainties (unknown effects that haven’t been defined yet).

How Did Risk Models Fare as the Crisis Gathered Force?

In the first quarter of 2020, risk models generally fell short of expectations. The major issue was their assumption that historical levels of volatility and correlations would last. With the advent of the coronavirus, volatility soared while historical correlations broke down or reversed because of the simultaneous impact of social distancing, collapsing energy prices, lower policy rates and a macroeconomic crash.

Some classically defensive subsectors like private hospitals were hit hard because of the deferral of medical procedures. Sales of consumer-cyclical products rose online and collapsed across bricks and mortar retailers. And industries that had for decades prospered through supplying China’s factories and wealthy consumers were faced with a sudden and drastic reversal of fortune. Classically inversely correlated sectors that risk models would typically use to offset risk—such as consumer services and real estate—switched to a positive correlation because of their shared exposure to the risk of contagion and social distancing.

Despite these vulnerabilities, some lessons from the global financial crisis (GFC) have improved the ability of risk models to analyze the impact of the current crisis. New factors like leverage and profitability that were introduced since the GFC have been especially important style factors. Jump processes are another important development. Risk models use jump processes or volatility adjustment factors to adjust portfolio volatilities upward more quickly, resulting in expected portfolio tracking error rising faster as risk spikes, instead of increasing slowly as more observations come in.

But there are still plenty of shortcomings that investors need to be aware of in their risk framework, outside of their risk models.

Managing Your Risk Framework for Crisis Conditions

Risk models work best when the world economy is in a relatively steady state. In this environment the past is a helpful guide to the future, historical correlations are reliable, and trends tend to persist. Under current crisis conditions investors need to fall back on a simpler risk containment approach based on human judgement and fundamental analysis. Key lessons include:

1. Supplement your factor risk models with exposure-only models

In a crisis, correlations might change or even flip, while volatilities will certainly increase. So investors should expand their risk-control framework with additional tools. In particular, they should complement their statistical risk models with simple exposure models. These can be based on fundamental analysis of stocks’ exposures to, for instance, styles, countries and industries. Volatility-adjustment features can also be added to risk models.

2. Don’t overreact and consider multiple scenarios

It’s impossible to predict either the precise timeline for the crisis or exactly how securities markets will react at each stage. So structuring a portfolio with a significant bias to recent winners, or in accordance with a specific narrative or scenario, risks being whipsawed by changes in market mood or perceptions.

3. Blend your risk model forecast

Although short-term risk models are better at predicting risk during crises they also come with high volatility and turnover. If your strategy is long-term, blend your risk model input with short- and long-term models, for instance using both short- and long-term model betas when considering portfolio construction.

4. Cash-flow modelling is key

Sustainable cash flows provide a strong basis for future performance—particularly under crisis conditions. Companies must be able to generate enough cash to withstand a prolonged crisis/revenue shortfall.

5. Don’t rely on a single factor

The crisis has repeatedly upended conventional factor relationships and correlations. At any time, relying on a single dominant factor to construct a portfolio carries higher risks. Under crisis conditions it invites random outcomes. Investors should also be mindful that their larger positions may be driving much of their factor exposure. This can create outsize risks if factor relationships change.

6. Avoid cluster risks

Standard risk models are unlikely to identify companies that are linked by common coronavirus themes and that as a group are vulnerable to the same factors. Cluster analysis can identify groups of stocks whose returns have become correlated and that may not be found in the same sectors or that don’t typically share similar characteristics.

We advocate implementing a cluster risk analysis framework that can help define new clusters (say, companies exposed to social distancing, such as restaurants, dentists and fitness centers), and can provide a structured way to determine the level of risk (either relative or absolute) appropriate for that cluster. Determining the size of a portfolio’s exposure to a given cluster should be consistent with both the level of investment insight and the risk/return characteristics of the cluster.

7. Make diversification effective

When conventional style and factor relationships are breaking down, it’s critical to understand the nature of each company’s business model and to analyze potential vulnerabilities on a bottom-up fundamental basis. Instead of relying on historic correlations, there may be a case for diversifying your portfolio across a larger number of carefully researched names. This will enable continued risk-taking in areas of investors’ expertise while limiting and diversifying risks associated with the current market environment.

8. Consider key factors both separately and together

Underlying exposures to the coronavirus, leverage, liquidity and volatility are all crucial to understand—particularly when crisis conditions cause them to interact in a way that magnifies risk. Analyzing these factors manually will pay off under conditions when risk models are struggling to adapt. We advocate rigorous stress-testing of any companies that are vulnerable to a combination of these factors. Stress-testing should drill down to a company’s supply chain too, as that’s where hidden risks may surface later.

9.Look for opportunities among the risks

Forced deleveraging has caused indiscriminate selling during the crisis, for instance through large-scale ETF redemptions and hedge-fund selling. This has created great potential for skilled fundamental investors with a clear game plan who can find opportunities in market rotations.

Know Your Models and Their Limitations

As the COVID-19 pandemic challenges risk models, we believe that examining risk through different lenses using different models will help achieve a more balanced view. Combining fundamental company analysis with a holistic view of how stocks, sectors and scenarios interact in new and unexpected ways can help investors manage unprecedented portfolio risks through a historic market event.

*OPEC + denotes the 11 countries that belong to OPEC including Iran, Iraq, Kuwait, Saudi Arabia, and Venezuela (the five founders), plus 10 non-OPEC oil-producing countries including Russia, Mexico, Kazakhstan, the United Arab Emirates, Libya, Algeria, and Nigeria.

Klaus Ingemann is Co-Chief Investment Officer—Global Core Equity

Thomas Christensen is Senior Quantitative Analyst—Global Core Equity

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

AllianceBernstein Limited is authorized and regulated by the Financial Conduct Authority in the United Kingdom.

This post was first published at the official blog of AllianceBernstein..