by Mark Stacey, Senior Vice-President, Co-CIO, AGFiQ Quantitative Investing, Head of Portfolio Management, AGF Investments Ltd.

The equity market selloff of the past few weeks has been a white-knuckle experience for investors, but the biggest loss facing them isn’t the temporary setback in share prices: it’s the time it will take for the correction to run its course and rebound to new highs.

In fact, the most certain part of any downturn is the eventual recovery. It’s happened every time since the Great Depression and the market crash of 1929, and it will surely happen again this time around. What is more uncertain, however, is the time it takes for a pullback of 20% or more to run its course and climb back to new all-time highs and above.

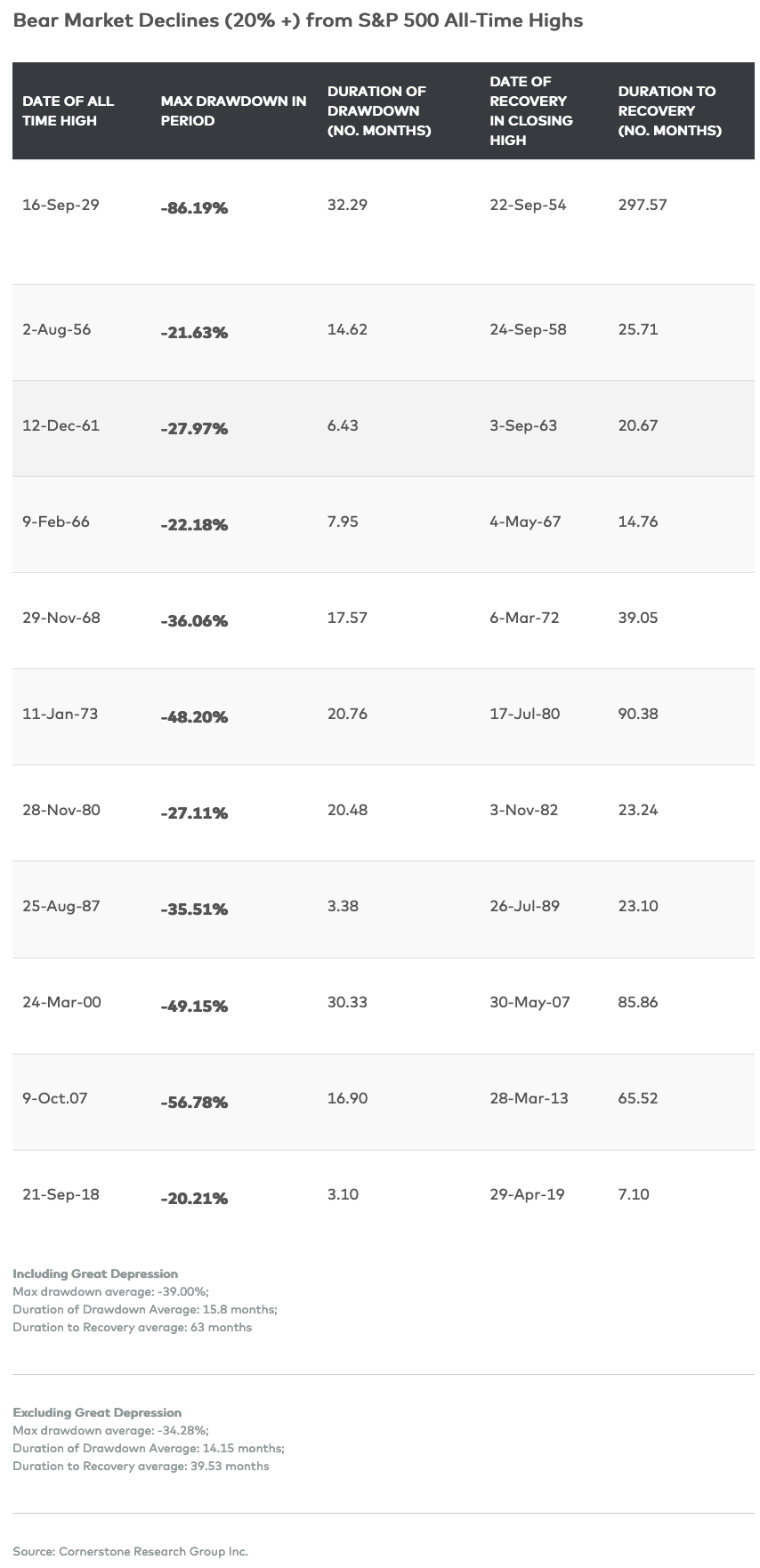

Take, for example, all 12 of the S&P 500 bear markets that have occurred over the past 90 years. The average drawdown period has been almost 16 months and the average recovery from the bottom has been 63 months. In other words, it has taken a total of 79 months on average, or just over six and a half years, for the S&P 500 to fully rebound from past bear markets.

These averages drop considerably when the unparalleled market crash of 1929, which was followed by the Great Depression, is omitted from the equation, but larger selloffs have generally been associated with longer rebounds than those coming on the heels of corrections that have been of a smaller magnitude.

Given this pattern, it’s seems clear that markets always recover, but the time it takes can vary dramatically, based at least in part on the severity of the correction. And it’s this uncertainty that often poses the biggest risk to investors, especially those who have relatively short time frames for realizing their investment objectives. Think, for instance, of the recovery time that a recent university graduate can afford following a correction versus someone who is the just months away from retirement.

So, what can be done to speed up the rebound? Cutting your losses and running for cover during a rout might seem like a good option. After all, it would potentially reduce the size of the drawdown. But timing the market is incredibly difficult to do, and many who move fully into cash may end up missing a part of the recovery and need even more time getting their portfolio back to square one.

Instead, investors should think of cash as one of several tactics that can be employed to help minimize the potential impact of a correction. These short-term changes in positioning might also include an emphasis on low-volatility stocks or defensive sectors, as well as efforts to high-grade holdings with more quality names, but they should always be considered within the context of a strategically diversified portfolio that is designed to mitigate losses throughout a market cycle. This includes exposure to stocks, bonds and alternative asset classes and/or strategies that provide less correlated returns.

In doing so, there is a much greater chance that corrections in one market can be offset by rallies in another, leading to reduced portfolio volatility and a better backdrop for shortening the recovery. That’s not a guarantee that today’s bear market won’t put a dent in people’s financial plans, but when it comes to limiting the recovery period following a selloff, time really is money.

*****

The commentaries contained herein are provided as a general source of information based on information available as of March 26, 2020 and should not be considered as investment advice or an offer or solicitations to buy and/or sell securities. Every effort has been made to ensure accuracy in these commentaries at the time of publication, however, accuracy cannot be guaranteed. Investors are expected to obtain professional investment advice.

The views expressed in this blog are those of the author and do not necessarily represent the opinions of AGF, its subsidiaries or any of its affiliated companies, funds or investment strategies.

AGF Investments is a group of wholly owned subsidiaries of AGF and includes AGF Investments Inc., AGF Investments America Inc., AGF Investments LLC, AGF Asset Management (Asia) Limited and AGF International Advisors Company Limited. The term AGF Investments m ay refer to one or m ore of the direct or indirect subsidiaries of AGF or to all of them jointly. This term is used for convenience and does not precisely describe any of the separate companies, each of which manages its own affairs.

™ The ‘AGF’ logo is a trademark of AGF Management Limited and used under licence.

About AGF Management Limited

Founded in 1957, AGF Management Limited (AGF) is an independent and globally diverse asset management firm. AGF brings a disciplined approach to delivering excellence in investment management through its fundamental, quantitative, alternative and high-net-worth businesses focused on providing an exceptional client experience. AGF’s suite of investment solutions extends globally to a wide range of clients, from financial advisors and individual investors to institutional investors including pension plans, corporate plans, sovereign wealth funds and endowments and foundations.

For further information, please visit AGF.com.

© 2020 AGF Management Limited. All rights reserved.

This post was first published at the AGF Perspectives Blog.