by Michael Hasenstab, Ph.D., Franklin Templeton Investments

You can download the full paper here.

There are now acute and contentious clashes over which economic and political paradigms will dominate the next generation: from capitalism to socialism, and from democracy to authoritarianism. The changing power structures between the world’s largest players increases the potential for a geopolitical event, in a range of theatres from trade to military, that could disrupt financial markets. Recently elevated tensions in the Middle East and frictions between the US and China are two significant examples. Throughout history, shifts in hegemonic power have often proved very unstable to financial markets and thus merit attention.

In addition, there are an increasing number of populist governments, which, in conjunction with a global trend toward extreme polarisation, have stoked greater volatility in economic policy and generally enabled undisciplined economic agendas. This populist surge has led to rising debt loads and corresponding fiscal risks across the developed world. Economic agendas are now increasingly being justified by largely untested economic theories. Whereas Keynesian or neo-Classical economic theories date back to before and around the middle of the last century, Modern Monetary Theory, which justifies printing money to fund fiscal expansion, has emerged with incredible political popularity despite a lack of rigorous theoretical or empirical foundation.

In the United States, divisions among the population have surpassed any point in recent history and given rise to heightened polarisation between political parties. Meanwhile, US deficit spending has deepened significantly, propelling the fiscal deficit toward an annual average of US$1.2 trillion over the next ten years (4.7% of gross domestic product [GDP])1 and necessitating massive levels of deficit funding through US Treasuries. These deficit numbers do not even account for the costs of recent spending proposals such as the Green New Deal, student loan forgiveness or sweeping health care reform.

Similarly, in Europe, nationalist parties have frayed the fabric of the eurozone, testing the political cohesion necessary to both maintain fiscal discipline today and hold the coalition together during a crisis in the future. Crucial structural concerns also remain unresolved, notably including debt sustainability and banking imbalances in Italy.

Concurrently, investors appear convinced that inflation will never be a risk in the US, yet cyclical and structural factors are undergoing significant changes that risk triggering an increase in inflation. Most notably, a move away from the free movement of capital and goods due to inward-looking policies risks increasing prices. A tight labour market, due to an extended period of economic expansion and large restrictions in both legal and illegal immigration, is driving labour shortages in many areas, resulting in a move higher in wages. These labour shortages combined with an increase in the bargaining power of labour—this past year has seen more strikes than any year since the 1980s2 —will likely continue to reinforce these trends.

On the central bank front, the US Federal Reserve (Fed) and the European Central Bank (ECB) were discussing ways to normalise monetary policy as recently as a year ago. Today, however, both the Fed and the ECB have again embraced a stance of greater monetary accommodation. Sustaining this accommodative approach prior to a realised crisis continues to push investors into riskier and less liquid investments. The world is now flush with over US$14 trillion3 in negative-yielding bonds—securities that are designed to return less than nothing. In the US, real yields on longer-dated US Treasuries are negative, reflecting significant valuation distortions for an economy growing at full potential with full employment.

Policies that were once considered highly unconventional have become normalised, as economies become increasingly reliant on central banks to cover gaps in fiscal and economic policy. The combination of already accommodative monetary and fiscal policy limits the tools of policymakers in the next global economic slowdown.

The potential way out of the next crisis could also be inhibited by a deterioration in social cohesion. Even in this period of record-low unemployment and increasing wage growth, popular frustration over heightened levels of economic inequality has significantly widened political differences. If broad economic conditions decline, it stands to reason that this sentiment would worsen, driving even more political polarisation. Whether this, in turn, results in policy paralysis or in a concerted shift toward extreme economic decisions, the ability to effectively and prudently address a significant economic or market downturn will likely be severely diminished.

The Four Pillars of Our Positioning

Given these factors, we are positioning our strategies around four key pillars: (1) maintaining high liquidity through elevated cash balances, with a focus on highly liquid assets and appropriate risk-adjusted position weights; (2) holding long exposures to perceived safe-haven assets, including the Japanese yen, Norwegian krone and Swedish krona; (3) maintaining negative duration exposure to the long end of the US Treasury yield curve; and (4) risk-managing a select set of emerging market exposures that appear better positioned to handle trade disruptions and potential rate shocks. Overall, we are aiming to create portfolios that can provide diversification against highly correlated risks across asset classes.4

- Maintaining High Liquidity in Our Strategies

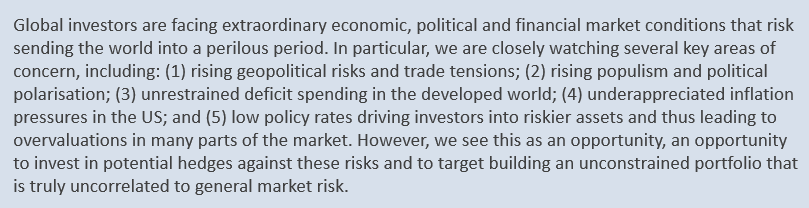

The combination of very accommodative central bank policy combined with a more regulated banking system has amplified credit risk in the shadow banking system. Thus, there has been significant growth in US credit markets over the last decade in areas of less transparency—private issuances with limited financial disclosure and diminished debt covenants. More than half of the high-yield US corporate bond market now comes from private placements, up from around 17% before the era of quantitative easing.5

Additionally, the levered loan market has surpassed the size of the high-yield bond market, with around 80% of its securities having light-to-nonexistent covenants and no public financial disclosures.6 This could be cultivating conditions for the next liquidity crunch. Years of easy money have eroded discipline in the markets by favouring the borrower, thereby damaging the ability of lenders to insist on appropriate financial disclosures and stronger covenants. For every disciplined lender that passes on a non-disclosure deal, there are many more willing to step in and blindly assume the unknown risks. All of this can work as long as credit markets remain bullish, but as soon as credit conditions begin to turn, liquidity will come at an exorbitant cost.

Recent spikes in US repo rates as a result of a supply/demand imbalance in short-term funding markets are a red flag for financial system liquidity risks. Such shocks also signal markets’ diminished capacity to absorb such large and ongoing Treasury issuance. Strains in the repo market have been among the first financial system warning signs in prior crises, indicating that liquidity stress points might be starting to emerge.

Thus, we remain wary of credit risks and liquidity risks in the global fixed income markets and are positioning our strategies accordingly. We are aiming to optimise liquidity within our portfolios by maintaining elevated levels of cash, focusing on more liquid assets and avoiding overvalued sectors, notably in credit. Instead we are focused on appropriately sizing our risk allocations in specific local-currency markets that show stronger levels of domestic liquidity. We are also targeting higher cash levels to have ample dry powder to pursue quickly developing opportunities during a market correction.

Additionally, we are aiming to diversify against index-related risks given the profusion of passive strategies that own the same positions. Passive exchange-traded funds and index funds that become forced sellers of the same securities at the same time are likely to find a dearth of liquidity when they need it most.

- Long Exposures to Perceived Safe-Haven Assets

A number of global risk factors have increased, raising the need to hedge some of our foreign exchange (FX) risk exposures and counterbalance our US rate hedge. The potential for a geopolitical event appears higher than it has been in decades, given ongoing tensions among the major world powers. Additionally, populism and political polarisations are impairing policy decisions, leading to elevated risks for a significant policy error. Massive deficit spending across the developed world has also exhausted many of the resources to respond to a future financial or economic shock. The heavy reliance on monetary policy tools to cure each minor setback the economy suffers has also blunted the ability for those tools to be effective in an actual crisis. In short, there is a risk the developed world has overextended itself on both fiscal and monetary fronts, leaving risk assets highly vulnerable to a financial market event.

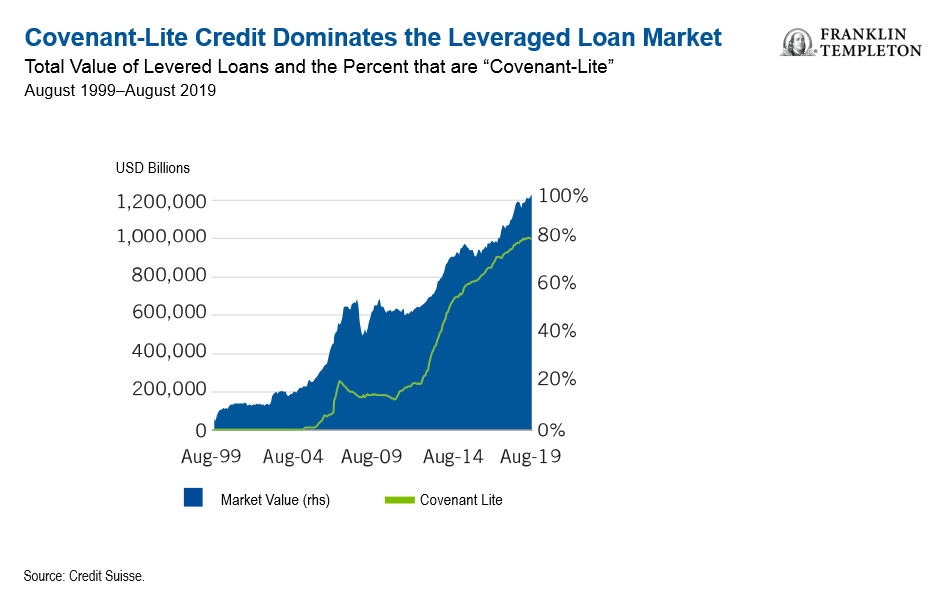

Thus, we have increased our allocations to what have historically proved to be safe-haven assets, both for their specific underlying valuations as well as their ability to hedge against broad-based financial market risks. We have notably increased our long exposure to the Japanese yen as it shows scope to appreciate against the US dollar on softening policy divergence between the Fed and the Bank of Japan, and also based on Japan’s strong external balances, which support a safe-haven status for the yen should global risk aversion deepen in the quarters ahead. We have also added long exposures to the Norwegian krone and Swedish krona as Norway and Sweden benefit from strong fiscal frameworks and current account surpluses that enable the currencies to emerge as safe havens within Europe—a role they previously served during the European debt crisis.

- Maintaining Negative Duration Exposure to the Long End of the Treasury Yield Curve

Markets continue to overvalue longer-term US Treasuries, in our opinion. Negative real yields in the US Treasury market appear highly vulnerable to a potential rate shock given rising deficit spending and rising debt. Inflation risks also remain significantly underpriced in markets, given the exceptional tightness in the labour market stemming from restrictions on immigration and breakdowns in the supply chain. Additionally, there are risks to the Fed’s ability to meet very aggressive market expectations on monetary accommodation that are already priced in across the Treasury yield curve. Rising inflation could put markets in the difficult position of contending with less monetary accommodation than expected.

Thus, we are positioning for curve steepening by maintaining investments in shorter duration US Treasuries combined with negative duration exposure to longer-term US Treasuries.7 The Fed can very effectively control short-term rates, but it cannot always control the economic and technical pressures on the longer end of the curve. We think investors need to diversify against the rate risks loaded in across the asset classes. We are structuring our strategies to be uncorrelated to the interest-rate risks that investors have embedded throughout their portfolios.

- Risk Managing a Select Set of Emerging Market Exposures

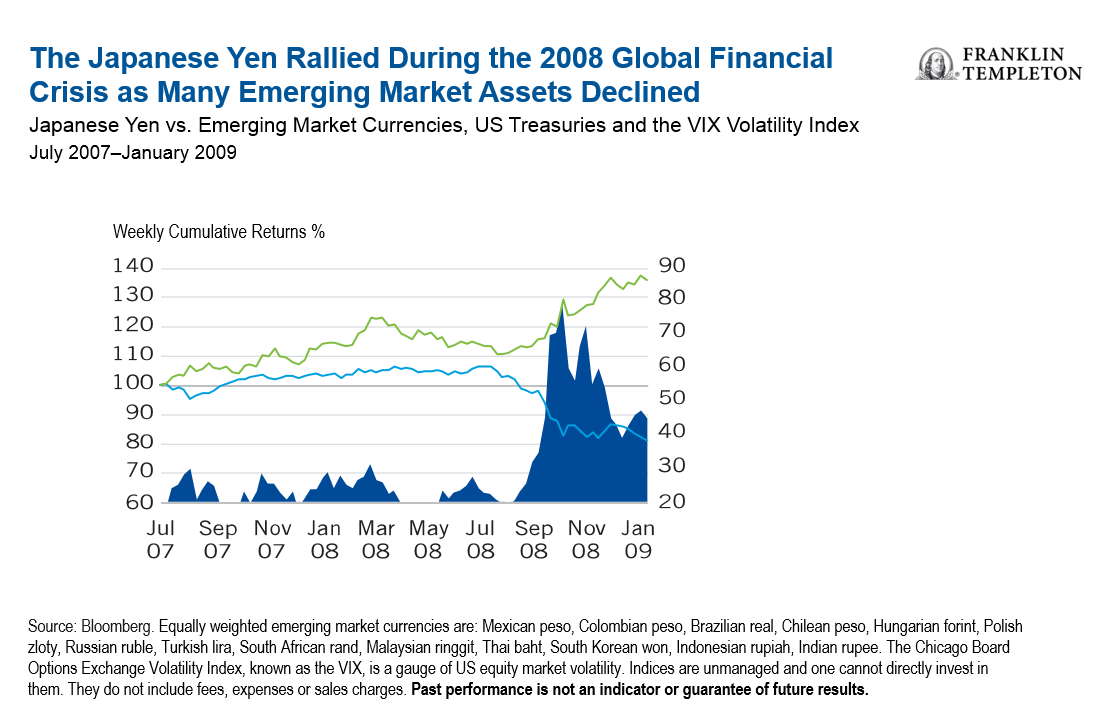

Finally, we continue to see value in specific emerging markets, but we have focused on sizing and hedging our positions for individual risks. We have generally been reducing the overall risk in the emerging market sleeves in our strategies while continuing to aim at isolating the specific alpha8 components through various hedges. For example, we’ve maintained exposures to local-currency bonds in India, but have fully hedged the Indian rupee and moderately reduced the years of duration in the position. For other countries, such as Brazil, we’ve largely maintained exposure while increasing our net-negative position in the Australian dollar as a proxy hedge to certain risks embedded in holding local currency Brazilian Bonds.

The net-negative Australian dollar exposure intends to hedge broad emerging market beta risk across our strategies, as the currency shows strong positive correlation with emerging market currencies due to shared risk factors, such as linkages to China’s economy and commodity markets. While we have become more cautious on the broad outlook for emerging markets as a whole, we continue to see scope for additional valuation strength in specific countries in certain alpha sources. These opportunities vary highly between countries and across risk exposures. We see a number of higher-yielding local markets that we expect to outperform the core fixed income markets in the quarters ahead.

Conclusion

Investors are currently faced with a growing number of unprecedented challenges that necessitate equally unique solutions. Investment strategies that may have worked well over the last decade are not as likely to be effective in the next one, in our view. We think investors need to prepare for today’s challenges by building portfolios that can provide true diversification against highly correlated risks present across many asset classes.

Important Legal Information

This material reflects the analysis and opinions of the authors as at 14 October 2019, and may differ from the opinions of other portfolio managers, investment teams or platforms at Franklin Templeton Investments. It is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed and the comments, opinions and analyses are rendered as at the publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market, industry or strategy. The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of the publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FTI affiliates and/or their distributors as local laws and regulation permits. Please consult your own professional adviser or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton Investments’ U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline.

Changes in the financial strength of a bond issuer or in a bond’s credit rating may affect its value. High yields reflect the higher credit risks associated with certain lower-rated securities held in the portfolio. Floating-rate loans and high-yield corporate bonds are rated below investment grade and are subject to greater risk of default, which could result in loss of principal—a risk that may be heightened in a slowing economy.

__________________________

1. Source: Congressional Budget Office; Update to the Budget and Economic Outlook, 2019 to 2029; August 2019.

2. Source: Bureau of Labor Statistics, U.S. Department of Labor, The Economics Daily: 20 major work stoppages in 2018 involving 485,000 workers, 12 February 2019

3. Source: Bloomberg Barclays Global Aggregate Negative Yielding Debt Market Values (USD), as at 30 September 2019.

4. Diversification does not guarantee profit or protect against risk of loss.

5. Source: Bloomberg Barclays. As at 31 August 2008, the size of the US corporate high yield market was around US$677 billion, and the size of the US corporate high yield 144a market was around US$114 billion. As at 31 August 2019, the size of the US corporate high yield market was around US$1,227 billion, and the size of the US corporate high yield 144a market was around US$659 billion. Rule 144a is a modification of the SEC regulation of privately placed securities, which enables them to be traded among qualified institutional buyers.

6. Source: Credit Suisse as at 31 August 2019.

7. Duration is a measure of the sensitivity of a bond or a fund to changes in interest rates. It is typically expressed in years.

8. Alpha is a risk-adjusted measure of the value that a portfolio manager adds to or subtracts from a fund’s return.

This post was first published at the official blog of Franklin Templeton Investments.