by John Mauldin, Mauldin Economics

As investors we have to make assumptions about the future. We know they will likely prove wrong, but something has to guide our asset allocation decisions.

Many long-term investors assume stocks will give them 6–8% real annual returns if they simply buy and hold long enough.

Pension fund trustees hire consultants to reassure them of this “fact,” along with similar interest rate and bond forecasts, and then make investment and benefit decisions.

Those reassurances are increasingly hollow, thanks to both low rates and inflated stock valuations, yet people running massive piles of money behave as if they are unquestionably correct.

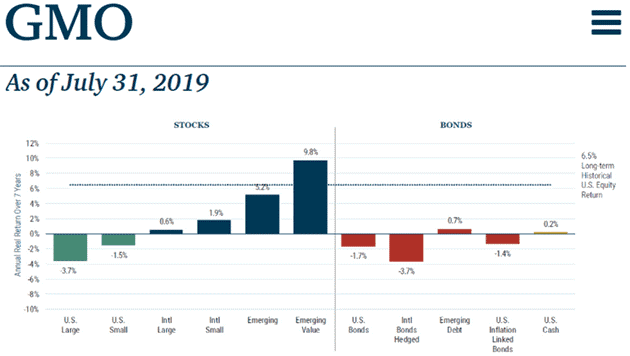

Realistic Forecasts

You can, however, find more realistic forecasts from reliable, conflict-free sources.

One of my favorites is Grantham Mayo Van Otterloo, or GMO. Here are their latest 7-year asset class forecasts, as of July 31, 2019.

These are bleak numbers if you hope to earn any positive return at all, much less 6% or more.

If GMO is right, the only answer is a large allocation to emerging markets which, because they are emerging, are also riskier.

The more typical 60/40 domestic stock/bond portfolio is a certain loss, according to GMO. (Note these are all “real” returns, which means the amount by which they exceed the inflation rate.)

Others like my friends at Research Affiliates (Rob Arnott), Crestmont Research (Ed Easterling), or John Hussman (Hussman Funds) have similar forecasts. They differ in their methodologies but the basic direction is the same.

The point is that returns in the next 7 or 10 years will not look anything like the past.

If you think these are reasonable forecasts (I do), then one reaction is to keep most of your assets in cash for at least a fractionally positive, low-risk return. That’s simple to do. But it probably won’t get you to your financial goals.

The 60/40 Fallacy

Many financial advisors, apparently unaware the event horizon is near, continue to recommend old solutions like the “60/40” portfolio.

That strategy does have a compelling history. Those who adopted and actually stuck with it (which is very hard) had several good decades. That doesn’t guarantee them several more, though. I believe times have changed.

But those decades basically started in the late ‘40s and went up until 2000. After 2000, the stock market (the S&P 500) has basically doubled, mostly in the last few years, which is less than a 4% return.

When (not if) we have a recession and the stock market drops 40% or more, index investors will have spent 20 years with a less than 1% compound annual return. A 50% drop, which could certainly happen in a recession, would wipe out all their gains, even without inflation.

And yes, there have been historical periods where stock market returns have been negative for 20 years. 1930s anyone? Yes, it is an uncomfortable parallel.

The “logic” of 60/40 is that it gives you diversification. The bonds should perform well when the stocks run into difficulty, and vice versa. You might even get lucky and have both components rise together. But you can also be unlucky and see them both fall, an outcome I think increasingly likely.

Louis Gave wrote about this last week.

Historically, the optimized portfolio of choice, and the one beloved of quant analysts everywhere, has been a balanced portfolio comprising 60% growth stocks and 40% long-dated bonds. Yet recently, this has come to look less and less like an optimized portfolio, and more and more like a “dumbbell portfolio,” in which investors hedge overvalued growth stocks with overvalued bonds.

At current valuations, such a portfolio no longer offers diversification. Instead, it is a portfolio betting outright on continued central bank intervention and ever-lower interest rates. Given some of the rhetoric coming from central bankers recently, this is a bet which could now be getting increasingly dangerous.

For the moment, I still think long-term yields will keep falling, helping the bond side of a 60/40 portfolio. Meanwhile, negative or nearly negative yields will push more money into stocks, driving up that side of the ledger.

So 60/40 could keep firing on all cylinders for a while. But it won’t do so forever, and the ending will probably be sudden and spectacular.

Which brings us to my final point.

Friends don’t let friends buy and hold

The primary investment goal as we approach the recession should be “Hold on to what you have.” Or, in other words, capital preservation.

But you may not realize that capital preservation can be better than growth, if the growth comes with too much risk. Here’s the math.

- Recovering from a 20% loss requires a 25% gain

- Recovering from a 30% loss requires a 43% gain

- Recovering from a 40% loss requires a 67% gain

- Recovering from a 50% loss requires a 100% gain

- Recovering from a 60% loss requires a 150% gain

If you fall in one of these deep holes you will spend valuable time just getting out of it before you can even start booking any gains. Once you start to fall, the black hole won’t let go. Far better not to get too close.

I can’t say that strongly enough: Friends don’t let friends buy and hold.

You must have a well thought out hedging strategy if you’re going to be long the stock market.

If your investment advisor simply has you in a 60/40 portfolio and tells you that, “We are invested for the long term and the market will come back,” pick up your capital and walk away.

I can’t be any more blunt than that.

Past performance does not predict future results. That has never been more true than for the coming decade.

The 2020s will be more volatile and difficult for the typical buy-and-hold index fund investor than anything we have seen in my lifetime.

Active investment management is not popular right now because passive strategies have outperformed. But I think that is getting ready to change.

You should start, if you’re not already, investigating active management and more proactive investment styles. You will be much happier if you do.

Relying on past performance as the tectonic plates shift underneath us, as the central bank policies suck historical performance into their maws, we must look forward rather than backwards to design our portfolios.

Copyright © Mauldin Economics