by Nick Getaz, CFA, Franklin Templeton Investments

As global economic growth slows and US-China trade tensions drag on, Franklin Equity Group’s Nick Getaz and Matt Quinlan see signs that some investors may be turning their attention away from the high-growth stocks that have been popular during the recent US equity bull market. Against this backdrop, they explain why they think investors might want to consider “rising dividends companies,” or resilient companies with track records of dividend growth, during various market environments.

In the past three years, high-growth stocks, including some in the technology sector, have propelled the US equity bull market to record highs. These stocks have tended to perform better than the overall equity market, even during periods of geopolitical uncertainty.

However, during recent bouts of market volatility, we’ve seen signs that many growth-focused investors may be starting to view things a bit differently. As US-China trade frictions continue and global economic growth shows signs of slowing, the market seems to be more interested in stable companies with a proven track record of consistent dividend growth.

Often drawn from earnings, dividends are one way in which companies may choose to reward investors. They are typically cash payments made on a regular basis, such as quarterly or annually.

That said, not all dividend-paying stocks are created equal, and our strategy is not focused on high-dividend yield. As long-term investors, our strategy is to invest in rising dividends companies, or companies with a demonstrated track record of substantial and sustainable dividend growth, for some of the reasons listed below.1

1. Rising Dividends Companies Are Long-Term Performers

We believe quality high-yielding companies may be attractive alternatives to investing in the bond market, but often don’t provide the sustainable growth prospects that rising dividends companies have the potential to offer.

According to our research, rising dividends companies tend to experience greater long-term stock price appreciation versus companies that only maintain their dividends or don’t pay one at all. They also tend to experience less volatility over time compared to those companies.

We believe that these performance characteristics are a result of the strong business models and management teams committed to paying an increasing dividend through the ups and downs of the business cycle.

2. Our Rising Dividends Companies Tend to Be Market Leaders

We believe that the companies that meet our dividend growth requirements start with a strong advantage. However, our focus is to identify which of these qualifiers are best positioned to maintain and increase this competitive advantage going forward.

We look to identify dividend growers which:

- are leaders in their industries or market niches;

- have attractive secular growth opportunities that allow the potential for improved profitability; and

- have management teams that have demonstrated sound capital allocation decisions, including investing for future growth and returning an increasing dividend stream to investors.

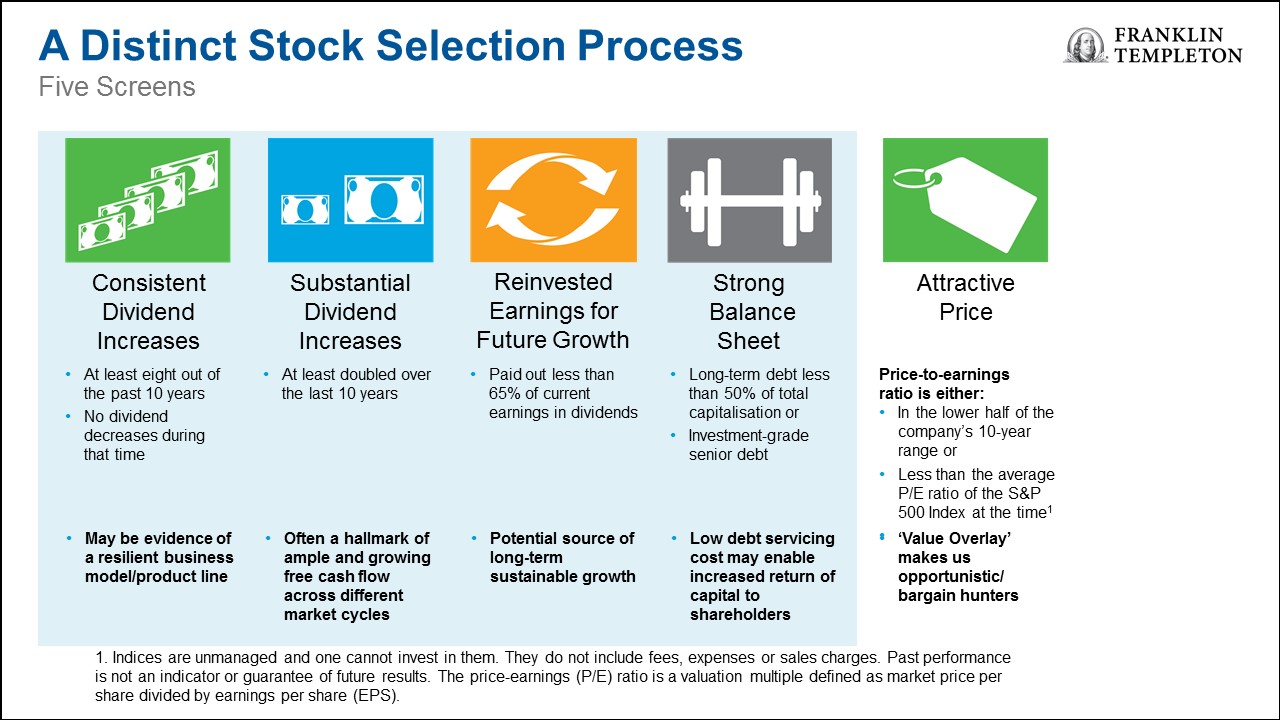

We have found a 10-year period of rising dividends is a good gauge of corporate soundness. In our view, at some point in those 10 years, most companies are likely to have experienced a softer economic period. Yet our experience tells us that some companies are likely to be more resilient than others.

We believe companies that can continue raising dividends through eight of the past 10 years—without a cut—have displayed some measure of fiscal strength. We also look for companies that have at least doubled their dividends during that time.

3. Rising Dividends Companies Are Popping Up in More Sectors

Since the financial crisis of 2008-2009, we have seen a much broader, more diverse group of companies qualify as dividend growers. Before the crisis, financial companies played a larger role in the category, but in the midst of the crisis, many banks cut or eliminated their dividends.

Many in the financials sector have since recovered and have been consistently growing their dividends and are starting to become what we consider to be dividend achievers. Meanwhile, companies in other sectors, including technology, initiated dividend programmes in the early 2000s.

These days, we are finding an increasing number of technology companies qualify as dividend growers, as well as companies in the industrials sector.

Tying it All Together

In our portfolio strategy, we use four quantifiable screens to identify our universe of investable dividend-paying companies and a value screen to make sure we are employing suitable value discipline in our investment process.

Not all high-quality companies will meet our screens, but this process provides a method of identifying a universe of companies with a demonstrated track record of sustainable and predictable performance. With this as a starting point, we can focus in on those opportunities which we believe are most likely to be able to continue this strong performance going forward.

Although we seek to identify companies with revenue streams that will hold up during difficult market conditions, we don’t consider ourselves to be defensive investors. We are looking for companies with good growth prospects in positive market conditions, as well as the ability to demonstrate more resilient performance in challenging markets.

We believe the combination of demonstrated dividend growth and strong business models, along with sound capital allocation, should drive increasing profit and free cash flow growth. This, in turn, tends to drive future investment in the next leg of growth, repeating the virtuous growth cycle and generating a sustainable and substantially growing dividend stream.

The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

To get insights from Franklin Templeton delivered to your inbox, subscribe to the Beyond Bulls & Bears blog.

For timely investment updates, follow us on Twitter @FTI_Global and on LinkedIn.

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Value securities may not increase in price as anticipated or may decline further in value. For stocks paying dividends, dividends are not guaranteed, and can increase, decrease or be totally eliminated without notice. While smaller and midsize companies may offer substantial opportunities for capital growth, they also involve heightened risks and should be considered speculative. Historically, smaller- and midsize-company securities have been more volatile in price than larger company securities, especially over the short term.

______________________________________

1. Dividends are not guaranteed and can increase, decrease or be totally eliminated without notice.

This post was first published at the official blog of Franklin Templeton Investments.