by Matthew Tucker, CFA, Blackrock

Morningstar recently made changes to its Intermediate Term Bond Fund Category. Matt explains the change and what it means for your portfolio.

Fund categories play an important role for portfolio builders by helping them know what they own and also set expectations for risk and returns.

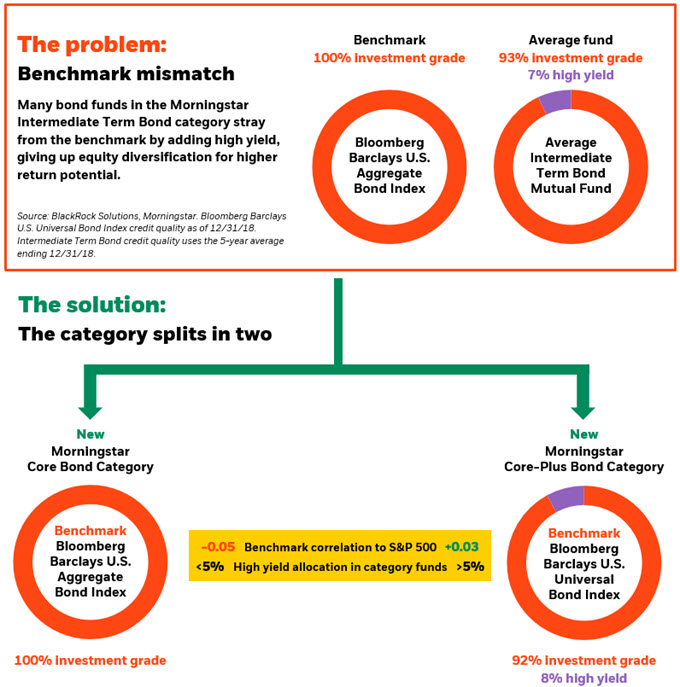

Investors looking for a bond fund for the core of their portfolio historically chose funds included in the Morningstar Intermediate-Term Bond category. This included bond funds that invested across a range of fixed income asset classes, had an intermediate duration (around five to six years) and were benchmarked to the Bloomberg Barclays Aggregate Index.

The challenge for investors was that while the index itself was relatively narrow – for example, it tracks just U.S. investment-grade bonds – the fund category was quite broad, and encompassed funds ranging from the more conservative to the more aggressive.

Time to split

To help investors make the distinction between management styles, on May 1, 2019, Morningstar split its $1.7 trillion dollar Intermediate-Term Bond category into two new categories: the Intermediate Core Bond category and the Intermediate Core-Plus Bond category (see graphic for a summary). Of the approximately 338 bond funds that were in the old category, 145 went into Core Bond and 193 went into Core-Plus. 1

This category split remaps bond funds based on their investment style, which Morningstar assessed using historical holdings, performance and prospectus language. Generally, more conservative, investment-grade-only bond funds were mapped to the Core category, and more aggressive funds — those holding more than a 5% allocation to high yield bonds, bank loans or emerging market debt — were mapped to Core-Plus.

As a result, investors can now better distinguish between different types of strategies and make more informed decisions about the most appropriate fund for their objectives. The new categories each contains a more homogenous set of funds, making is easier to evaluate the performance and risk of like portfolios.

Know your benchmark

Morningstar’s two new categories are now measured against different market benchmarks as well. The Core Bond category keeps the Bloomberg Barclays U.S. Aggregate Bond Index (which holds 100% investment grade bonds), while the Core-Plus now uses the Bloomberg Barclays U.S. Universal Bond Index (which holds on average 5-8% in risker, below-investment-grade bonds).

We view this as a positive for the investment community because now the benchmark more accurately reflects the risk of the funds in each category. (Read more in our previous blog post, “Why your bond fund and its index may not be a good fit.”)

Rising and falling stars

There are some temporary impacts, of course. Many investors may be asking themselves why the star rating of their bond fund has changed. In Morningstar’s old methodology, both conservative and aggressive funds were evaluated against each other, and star ratings awarded based on performance relative to the overall group. With the split of the category we now have like evaluated against like: conservative funds rated against other conservative funds, and more aggressive funds rated against more aggressive funds.

The net result is that some more conservative funds have received higher star rankings, as their performance now looks better relative to other Core portfolios. By the same token, some more aggressive funds actually lost stars as their performance no longer looks as good relative to the more aggressive group of funds in the Core-Plus category.

Is it time to re-evaluate your bond fund?

The change in fund classification opens a door to take a fresh look at your bond holdings. First, ask yourself why you have bond exposure in your portfolio. Is it to diversify equity risk, generate income and/or preserve principal? (You can read more about the 3 roles bonds can play in a portfolio in a previous post.)

Once you know the role you want your bonds to play, you can determine if your current bond fund is meeting your needs.

- Funds in the Intermediate Core Bond category are likely to be more aligned with those seeking to diversify equity risk and preserve principal, due to the 5% limit on riskier bonds.

- Funds in the Intermediate Core-Plus Bond category may be better suited for investors seeking higher income and total return potential, due to looser constraints on higher risk securities.

Fortunately, both categories provide a number of good investment options. And now you can make even more informed choices.

Matt Tucker, CFA, is the iShares Head of Fixed Income Strategy and a regular contributor to The Blog.

- Source: Morningstar, as of 5/1/2019. Based on the oldest share class of all open-end funds in the Morningstar Intermediate Term Bond Category.

Investing involves risk, including possible loss of principal.

Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments.

Investment comparisons are for illustrative purposes only. To better understand the similarities and differences between investments, including investment objectives, risks, fees and expenses, it is important to read the products’ prospectuses.

Index performance is for illustrative purposes only. Index performance does not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date indicated and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any of these views will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

The strategies discussed are strictly for illustrative and educational purposes and are not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. There is no guarantee that any strategies discussed will be effective.

This post contains general information only and does not take into account an individual’s financial circumstances. This information should not be relied upon as a primary basis for an investment decision. Rather, an assessment should be made as to whether the information is appropriate in individual circumstances and consideration should be given to talking to a financial advisor before making an investment decision.

©2019 BlackRock, Inc. All rights reserved. BLACKROCK is a registered trademarks of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

USRMH0619U-883472