by John Lynch, Chief Investment Strategist, LPL Financial

- We look at what’s priced into stocks following year-to-date strength to help gauge potential impact of surprises and disappointments.

- When we look at what’s not priced in, we see several possible surprises that could propel the stock market to new highs.

- Possible positive surprises include the stimulus boost from a potential China trade deal and better-than-expected corporate profits in 2019.

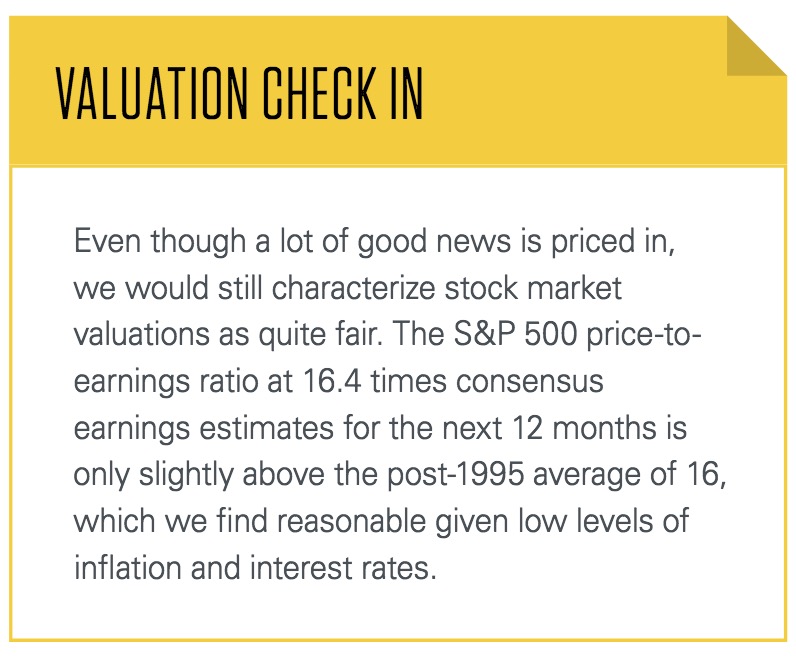

After such a strong rally for stocks this year, you may be wondering what could drive stocks higher from here. With the S&P 500 Index less than 1% away from its all-time high set September 20, 2018, a lot of good news has been priced into stocks. You may also be wondering what possible disappointments could cause stocks to pull back from here, especially given the soft patch in the U.S. economy and corporate profits during the first quarter.

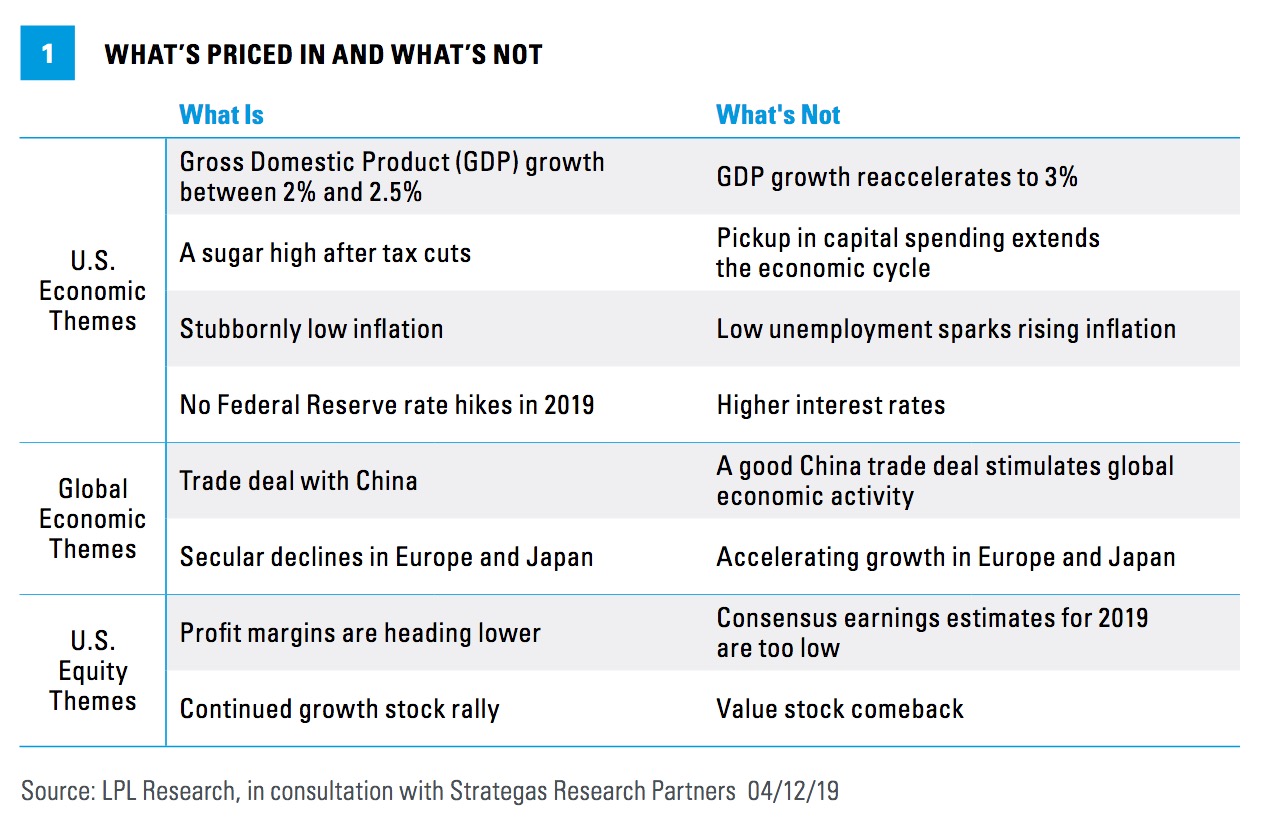

To help us with these questions and in consultation with our friends at Strategas Research Partners, we have taken a look at what may or may not be priced into stocks. In doing so, we have attempted to identify some potential surprises that could drive the next leg of this rally, as well as some possible areas of disappointment if something that is priced in does not occur [Figure 1]. [backc url='http://www.dynamic.ca/leadership/eng/active.html?fund=dreii2f&utm_source=aa&utm_medium=banner&utm_campaign=alts_2019&utm_content=dreii2f']

U.S. Economy – What’s Priced In

GDP growth between 2% and 2.5%. Bloomberg consensus stands at 2.4% real gross domestic product (GDP) growth in 2019. The short stint above 3% last year was considered a one-off and not sustainable after the boost from tax reform that became law at the end of 2017.

A sugar high after tax cuts. Tax reform in December 2017 provided significant stimulus for the U.S. economy. The consensus view is that the peak impact of the tax law has already been felt and that the benefits to the U.S. economy are quickly diminishing, which we believe may be overly pessimistic.

Stubbornly low inflation. The Phillips Curve depicts the relationship between unemployment and inflation. The labor market has been tight for a while, yet wage growth has been moderate, causing many to think the Phillips Curve is dead.

No Fed rate hikes in 2019. The Federal Reserve (Fed) has told us as much, so this is already fully reflected in stock prices. On a related note, markets are pricing in low interest rates and a flat yield curve well into the future.

What’s Not Priced In

GDP growth reaccelerates to 3%. Our forecast for 2.5% puts us near consensus. That means if growth comes in well above that mark (or below, for that matter), the market reaction could be sizable. We believe an upside surprise is more likely than a big miss.

A pickup in capital spending helps extend the business cycle. A China trade deal may unlock animal spirits and drive more capital spending and higher productivity, which may enable more growth with less wage pressure as companies efficiently produce more output. Capital investment incentives from the December 2017 tax reform, including lower levies, repatriation of foreign-sourced profits, and immediate expensing, remain in place.

Low unemployment sparks rising inflation. A modest pickup in inflation is within expectations, but markets are probably not prepared for more than that. Labor markets have been tight for quite some time with moderate wage growth, which has anchored the market’s inflation expectations.

Higher interest rates. With the market having grown accustomed to low interest rates and the Fed on hold, a jump in financing costs would surprise investors. We expect rates to gradually move higher over the rest of 2019, with increases capped by low interest rates overseas.

Global economy – What’s Priced In

Global economy – What’s Priced In

A trade deal with China. All indications are that some form of a deal will get done by June, if not sooner. Recent reports that China has agreed to the U.S. demand for an enforcement mechanism are encouraging.

Secular declines in Europe and Japan. Economies in Europe and Japan have lagged behind the United States in economic growth for quite a while, and markets are inclined to expect lackluster growth to continue for the foreseeable future.

What’s Not Priced In

A good China trade deal stimulates global economic activity. A deal is widely expected, but market participants may be surprised by the economic and market boost from the removal of uncertainty and greater access to Chinese markets for U.S. companies. The possible rollback of existing tariffs could be a positive surprise.

Stimulus-induced growth in Europe and Japan. Recent data in Europe have suggested that economic growth is stabilizing. Possible catalysts for better growth in the second half in Europe include reduced trade tensions and a soft Brexit. In Japan, fresh stimulus could help offset the impending increase in a value-added tax (VAT) increase slated for October 2019.

U.S. Equities – What’s Priced In

Profit margins are heading lower. We’ve heard calls for lower profit margins for several years now. Those calls will be right at some point, but the market seems to be quite confident that time has come, suggesting the potential for a positive surprise. As a result, analysts are calling for stronger sales growth than earnings growth in the first quarter and the rest of 2019.

Continued growth stock rally. The market appears to be pricing in a sustained period of subpar economic growth based on the continued strength in growth stocks. Slower economic growth has tended to make growth companies more attractive as growth becomes tougher to find.

What’s Not Priced In

Earnings estimates for 2019 are too low. We see economic growth ahead as sufficient to drive 2019 S&P 500 earnings growth above current consensus estimates in the 3–4% range, pushed by fiscal stimulus, robust manufacturing output, healthy labor markets, and resolution of the U.S.-China trade dispute.

Value stock comeback. After roughly 10 years of growth stock outperformance, value may be due for a comeback. Relative valuations favor value stocks, while a pickup in economic growth—should it occur—could give cyclical value sectors a boost, notably financials and energy.

CONCLUSION

We believe there are enough potential positive surprises to push the S&P 500 to new highs this year and beyond. That said, clearly there are risks, as there always are. Those risks led us to reduce our recommended U.S. equities allocations from overweight to market weight in late March.

We would not be surprised if the market gets more than it expects out of the U.S.-China trade deal and corporate profits. On the other hand, we are not particularly optimistic that Europe and Japan can deliver better growth in the near term, and the market may be underpricing the possibility that a Fed rate hike later this year could push interest rates higher.

We continue to expect the S&P 500 to end 2019 at or near our fair value target of 3,000, but with the index only about 1% away from that target, and considering the global economic soft patch in the first quarter, we see the risk-reward trade-off between stocks and bonds in the near term as fairly balanced.

Thank you to our friends at Strategas Research Partners for their contributions to this report.

[Download PDF]

*****

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in this material may not develop as predicted.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments.

All indexes are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

LPL Financial and Strategas Research Partners are not affiliates of each other and make no representation with respect to each other.

DEFINITIONS

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country's borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments, and exports less imports that occur within a defined territory.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

Copyright © LPL Financial