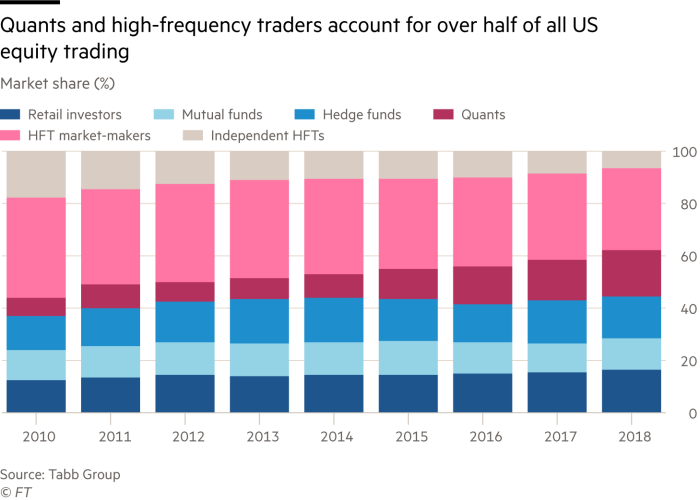

Artificial intelligence (AI), quant funds, high-frequency trading, big data — these terms get thrown around a lot these days and can create confusion and uncertainty. (Case in point: Tesla CEO Elon Musk has said that AI is more dangerous than nuclear weapons, with Facebook CEO Mark Zuckerberg calling such statements “pretty irresponsible.”1) Beyond such dramatic statements, it’s clear to see that quants and high-frequency traders (HFTs) account for more than half of all US equity trading. How does all of this fit into the investing world as we see it?

The importance of a differentiated view

The portfolio managers for the Invesco Canada Equity Small Cap team believe that the foundation of any good investment is having a differentiated and informed view versus the market consensus (which the renowned investor Benjamin Graham once famously called “Mr. Market”). If we take a step back and think about the ingredients of a differentiated view, we believe that, on a high level, this requires using all of the data sources available to us and/or utilizing a more rational thought process.

Gaining an information advantage in a data-rich world

Of course much has changed since the days when Warren Buffett used to go to Moody’s or the SEC’s office to get his hands on company information that wasn’t available elsewhere. In fact, it’s quite the opposite today. Investors have access to a proliferation of data, from online access to detailed company reports, to “alternative data” sold by market-data companies. These alternative data run the gamut from consumer credit card purchase data to satellite images of retailers’ parking lots. Combine this cornucopia of data with today’s quantitative funds – which have come a long way since the late 1980s and today are stacked with PhDs using sophisticated AI – and it’s easy to see that having a superior, differentiated view is very difficult these days — if we’re talking about short-term trends. A lot of money chases this quarter’s or next quarter’s results.

On the other hand, we believe long-term projections are a different game entirely — one in which judgment, experience and harder-to-quantify information play a far bigger role in coming up with a reasonable forecast. For example, instead of mining credit card purchase data to forecast new customer wins in the next quarter for Liberty Broadband Corp., a US cable company held by our funds, we’ll spend our time diving deep into the risk and opportunity of 5G by consulting industry experts, sleuthing through online forums about early customer experiences, going to conferences and the like — none of which can easily be fed into trading algorithms. (Liberty Broadband represented 5.97% of Invesco U.S. Companies Class and 5.66% of Invesco Global Small Companies Class as of Dec. 31, 2018.)

Why do we do this? We believe that the majority of a company’s value lies in its long-term future cash flows — beyond the next one, two, three or even 10 quarters — and that’s why it’s critical for us to understand the long-term trends that shape what the company will look like five years down the road.

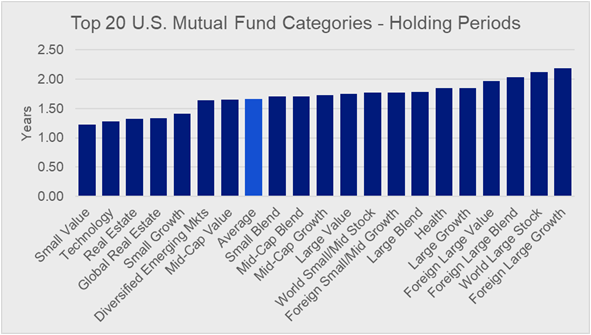

This is how we on the Invesco Canada Equity Small Cap team think about investment horizons and how we seek to differentiate ourselves from the algorithm wars that dominate the short-term landscape. We approach all companies with the mindset of a business owner, getting to the bottom of the drivers that matter in the long run. This is borne out in our consistently long average holding periods of 4.6 to 8 years across our small-cap funds, which stands in stark contrast not only to quant funds, but even to most of our peers in the mutual fund industry.

Source: Morningstar Direct

This post was originally published at Invesco Canada Blog

Copyright © Invesco Canada Blog