There’s a reason why “Don’t fight the Fed” is a market mantra

by Jurrien Timmer, Director of Global Macro, Fidelity Investments

Key takeaways

• After one of the worst Decembers ever, we just had one of the best Januaries, retracing about two-thirds of the 20% decline in only five weeks.

• While several correction analogs look compelling (1994, 1998, and 2011), no two corrections are alike: Context is everything.

• The combination of a technical extreme, a Fed pivot, and the unlikelihood of an imminent recession leaves the market in better shape for 2019.

• While the lows are likely in for this correction, I don’t expect imminent new highs either, because valuations are now higher while earnings estimates continue to drift lower.

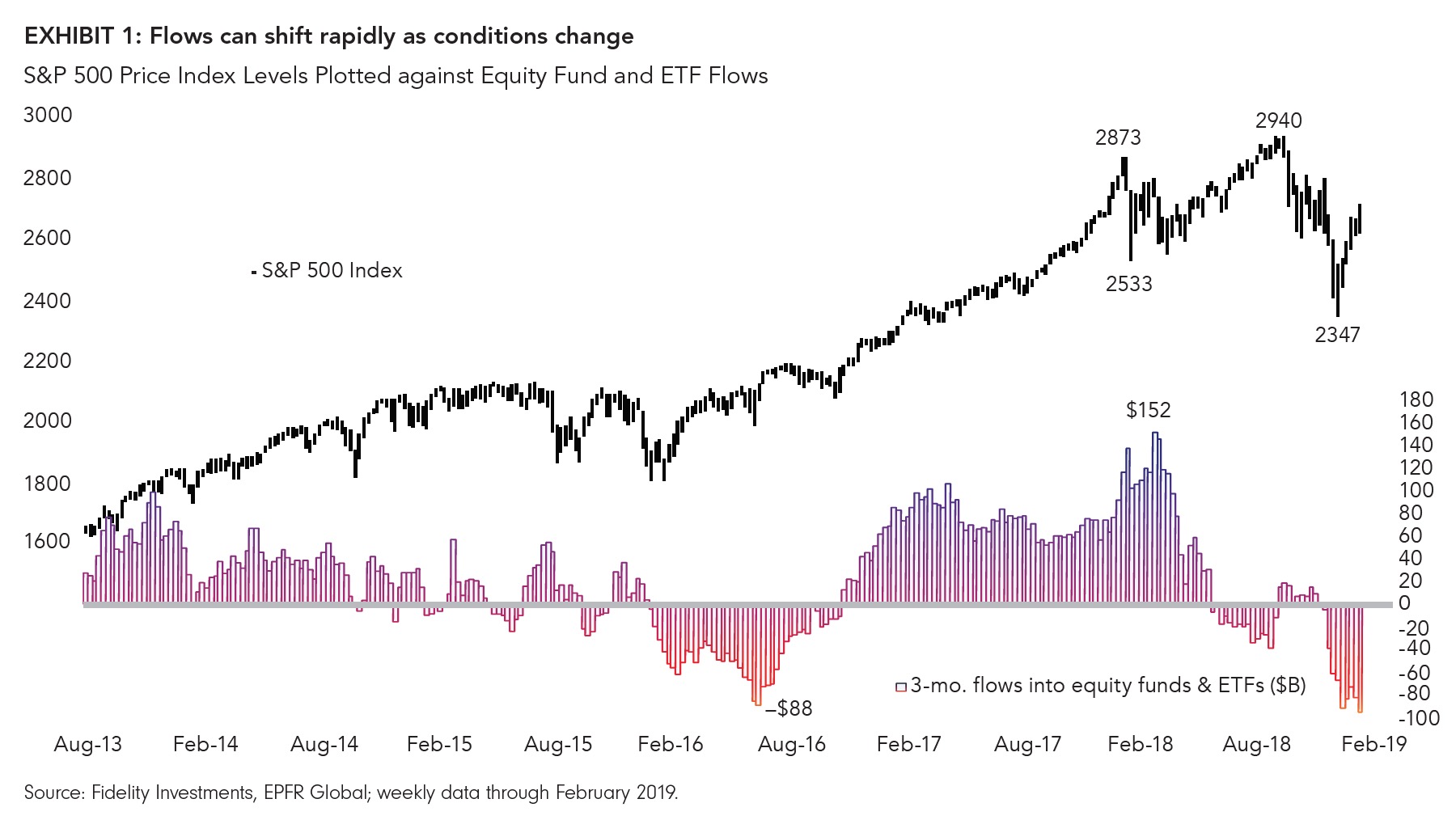

These past four months have proven quite the rollercoaster ride for investors. The S&P 500® index declined exactly 20% from its high at 2940 in early October to its low of 2347 in late December, led by certain financials stocks and the crowded momentum/growth space (most notably the FANG gang—Facebook, Amazon, Netflix, and Google—and similar companies), only to rally 16% over the past five weeks through January 31. And just like that, we went from one of the worst Decembers on record to one of the best Januaries.

It’s a good reminder for investors that when the market goes down, we should resist our fight-or-flight impulses and instead take a long view in the most emotionally detached way possible. That includes evaluating the four major market drivers—earnings, liquidity, valuation, and sentiment—against our investment goals and risk objectives.

I know, it’s a tall order and we all succumb to the loss-aversion dynamic to some degree. The stock market is one of the few places where lower prices usually lead to lower demand. Typically it’s the other way around: When a favorite product or service is discounted by 20%, we usually see that as a good thing and stock up; when it concerns our life savings, not so much.

To wit, investors sold a record $83 billion of equity funds and ETFs during the month of December, according to EPFR Global. That means that a whole bunch of investors locked in a 20% loss, right at the bottom.

This 20% drawdown was the result of a trifecta of circumstances. The main driver was the changing fundamental landscape in the form of slowing earnings growth combined with monetary tightening by the U.S. Federal Reserve. This was compounded by the forced liquidation of crowded momentum trades (Goldman Sachs reports that one of its indexes that tracks FANG-type stocks was down around 30%), as well as a lack of market liquidity, especially heading into year-end. This turned what I had expected to be a garden-variety 10% to 15% correction into a -20% “mini-bear.”

Now that the market has recovered around two-thirds of its decline, the inevitable question is: What’s next? Was the December low of 2347 just “A” low or was it “THE” low? Does the market break out to new highs soon or does it stall out here on the way to lower valuations? To answer this question we need to look at the four major drivers mentioned above: earnings, liquidity conditions, valuation, and sentiment.

What we know is that earnings growth is slowing—and dramatically so. From its quarterly peak of a +26% annual growth rate (AGR) in Q3, earnings growth for Q4 is down to +13% AGR, and the consensus estimates for the coming quarters are -0.5% (Q1), +2.5% (Q2), and +3.2% (Q3). On a calendar-year basis, earnings growth is decelerating from +24% in 2018 to only +6% in 2019. And those estimates continue to come down: The CY2019 estimate was at +12% just a few months ago. At this rate we’ll be lucky to realize current estimates of low- to mid- single-digit growth in 2019.

But against this slowdown scenario are three important offsets. First, valuations came way down in 2018; in fact, I see 2018 as the year of the “valuation reset.” At the January 2018 peak, the forward price-earnings (P/E) ratio was 19.5x and the trailing P/E was 21.9x. By late December the forward was at 13.7x; the trailing, 14.7x. That’s a tremendous de-rating of up to 30%, and it left the market in a much better place in terms of valuation. Second, sentiment did a complete round-trip. At the beginning of 2018, investors were piling into stock funds and ETFs at a $152 billion annual rate and couldn’t get enough of the FANGs. By December they were selling record amounts, to the tune of an $89 billion annual rate (Exhibit 1).

Finally—and most importantly, in my opinion—following its hawkish stance at the December meeting of the Federal Open Market Committee (FOMC), the Fed was clearly taken aback by the sharp drop in stock prices and the concurrent widening of credit spreads and decrease in inflation expectations, as evidenced by a decline in the breakeven rates (the yield difference between a nominal bond and an inflation-linked bond of the same maturity) for TIPS (Treasury Inflation-Protected Securities). And just like that, the Fed pivoted to a more dovish stance at its January FOMC meeting a few weeks ago. Instead of promising to raise rates three or four more times by the end of 2020, plus leaving its balance-sheet reduction plans on autopilot, the Fed all of a sudden is likely on hold for probably the next six months, if not longer, and even its balance sheet is now in play.

This is an important reminder of the old market mantra: “Don’t fight the Fed.” Against a backdrop of a slowing but still-growing U.S. economy (as evidenced by the healthy increase in January’s payroll employment), and amid very few if any, signs of a recession, the above factors all suggest that the 20% drawdown in stock prices and the related 30% de-rating in the P/E ratio was just a mini-bear and not the start of a much deeper market retreat.

Context is everything

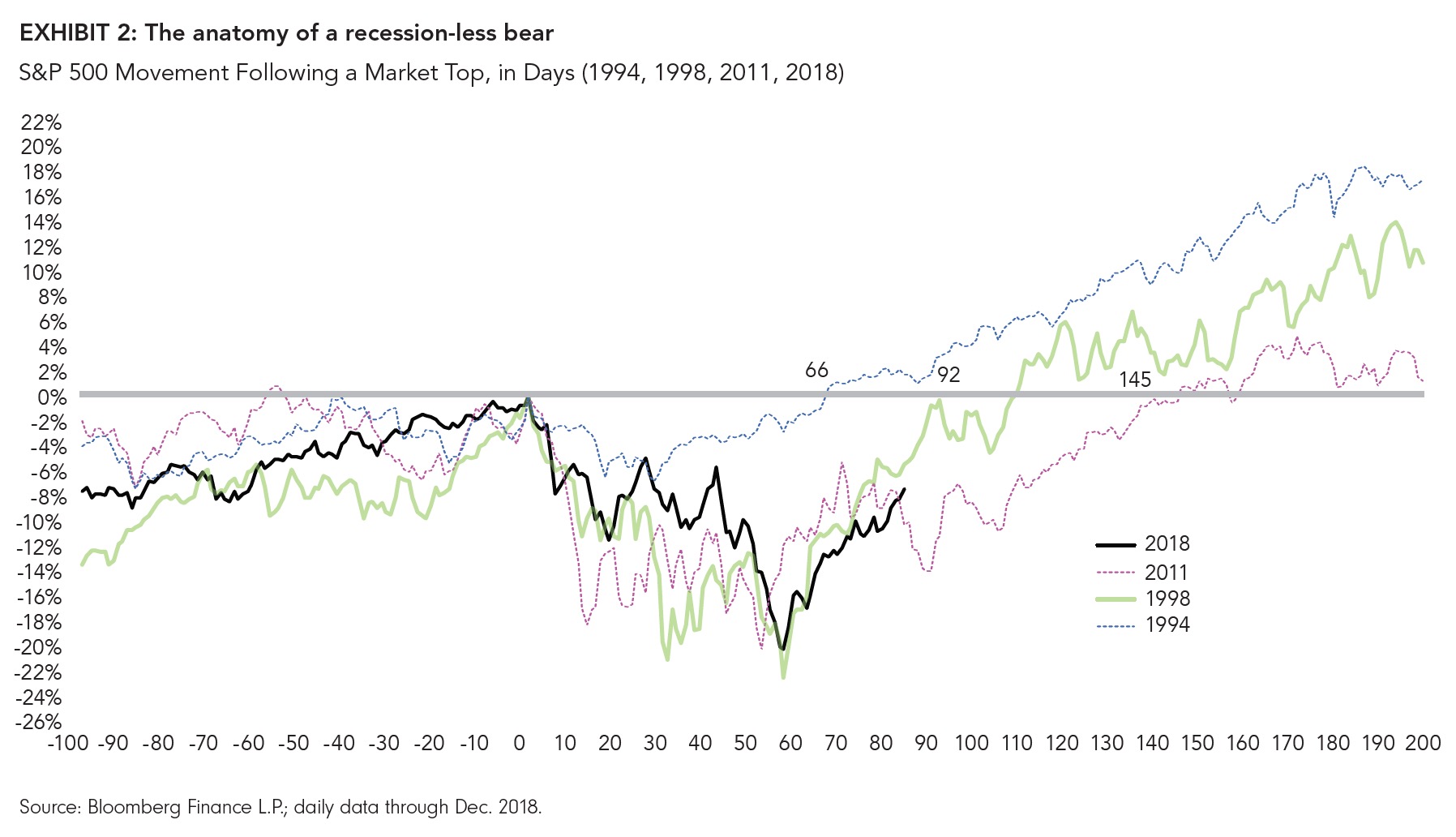

This reminds me a lot of three previous corrections that could be defined as mini-bears: those in 1994, 1998, and 2011 (Exhibit 2). In all three cases, the stock market corrected and the central bank (U.S. or otherwise) pivoted within the context of continued economic growth. In 1994, the stock market was stuck in a year-long correction when the Fed suddenly and sharply tightened monetary policy. While the overall decline for the S&P 500 was only 10%, things actually felt much worse because the majority of stocks were down 20% or more.

As a result, the 1994 cycle was considered a “stealth” bear market. Toward the end of 1994, the Fed pivoted and all of a sudden stocks were off to the races: The S&P 500 gained roughly 38% in 1995.

In 1998, the S&P 500 fell 22% in a short span of time, mostly driven by the problems in emerging markets and, of course, the LTCM (Long-Term Capital Management) hedge fund fiasco that severely tested the global financial system. Again, the Fed pivoted—easing three times in short order—and we suffered no recession. The result was that the S&P 500 took only 95 days to recover all its losses and went on to produce a 68% gain from October 1998 to the next top in April 2000.

In the summer of 2011, the S&P 500 corrected 22%, partly as a result of the U.S. credit downgrade—the first time the federal government was assigned a rating below AAA—but mostly because the European sovereign debt crisis was in full bloom. The Fed did not pivot that time, but in October the European Central Bank (ECB) announced its LTRO (long-term refinancing operation), wherein it provided needed liquidity to eurozone banks.

That was the ECB’s initial foray into QE (quantitative easing). Again, against the backdrop of no recession (at least in the U.S.), this combination of factors allowed for the market to quickly regain its lost ground.

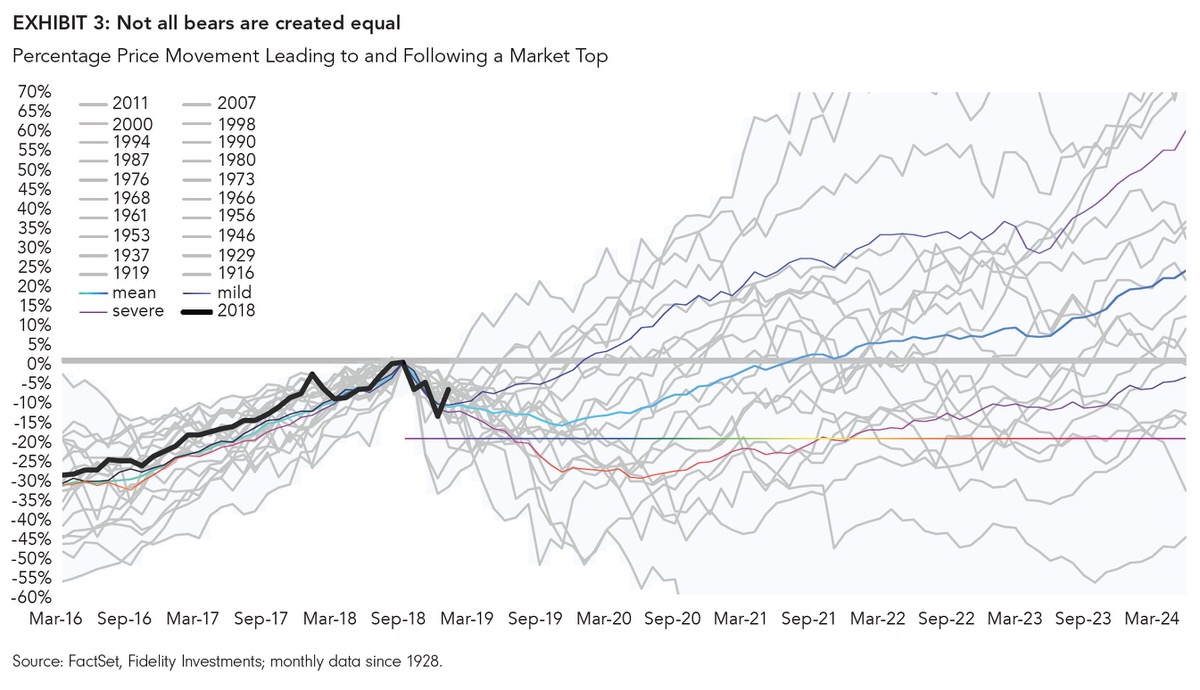

I think these are good analogs and a good reminder that context is everything when it comes to figuring out what to do when the market goes down. Exhibit 3 shows a history of every cyclical top since 1900. You can clearly see that corrections are hardly cookie-cutter affairs; every decline is different in terms of circumstances, length, and magnitude. History only rhymes after all.

A few simple questions offer a case in point: What happens after the market has declined 20%? Is the market up or down a year later? What’s the forward return and batting average? The answers tell you everything you need to know about this “falling-knife” phase of the market cycle: Based on at least 20 cycles over the past 100 years, whenever the S&P 500 or Dow Jones Industrial Average declined at least 20% from a recent high, 55% of the time each index moved higher over the subsequent 12 months—by an average of 23%. This happened 55% of the time. But get this: The 45% of the time that the market continued to continued downward, it dropped by another 24%, on average. So, if you try to catch the falling knife and call a stock-market bottom: When you’re right, you’re really right, but when you’re wrong ...

So are we out of the woods here? In terms of downside risks, I think so; but that doesn’t mean new highs are around the corner. My sense is that we have another quarter or two of market purgatory ahead of us; why? Three reasons: First, while the Q4 earnings season (currently underway) is looking pretty decent (with 72% of companies beating lowered estimates by an average of around three percentage points), the estimates for CY2019 overall, as well as the next few quarters, continue to move lower. Also, the typical bounce in growth rates during earnings season isn’t happening to the same degree as it usually does. So far the Q4 number has increased by 70 basis points (bps) from 11.8% to 12.5%, less than the typical bounce of 300+ bps.

Second, with the S&P 500 recovering 16% while earnings growth is slowing, valuations are by definition getting less compelling again. The trailing P/E multiple has now risen from its low of 14.7x to 16.9x, and the forward multiple has rallied from 13.7x to 15.8x. They’re not “nosebleed” levels by any means, but they’re no longer a bargain either. Finally, while the Fed has pivoted from promising several more rate hikes to now basically saying it’s done for the cycle (or at least the next six months), that’s not the same thing as going from rate hikes to rate cuts, as happened in both 1994 and 1998. So, it’s a bullish pivot but not on the same order of magnitude as the other analogs. But who knows? It’s only March, after all.

Putting all this together, my best guess is that December was an important low, but I also think that from these levels the market is going to have a tough time making sustained new highs. With the stock market having declined 20% in December and the Fed having pivoted, ultimately this all comes down to whether a recession is coming or not. If so, perhaps further declines lie ahead. But if not, this could well be a great opportunity to rebalance.

The source of all factual information and data on markets, unless otherwise indicated, is Fidelity Investments. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus, which contains detailed investment information, before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Certain Statements in this commentary may contain forward-looking statements (“FLS”) that are predictive in nature and may include words such as “expects”, “anticipates”, “intends”, “plans”, “believes”, “estimates” and similar forward-looking expressions or negative versions thereof. FLS are based on current expectations and projections about future general economic, political and relevant market factors, such as interest and assuming no changes to applicable tax or other laws or government regulation. Expectations and projections about future events are inherently subject to, among other things, risks and uncertainties, some of which may be unforeseeable and, accordingly, may prove to be incorrect at a future date. FLS are not guarantees of future performance, and actual events could differ materially from those expressed or implied in any FLS. A number of important factors can contribute to these digressions, including, but not limited to, general economic, political and market factors in North America and internationally, interest and foreign exchange rates, global equity and capital markets, business competition and catastrophic events. You should avoid placing any undue reliance on FLS. Further, there is no specific intentional of updating any FLS whether as a result of new information, future events or otherwise.

From time to time a manager, analyst or other Fidelity employee may express views regarding a particular company, security, and industry or market sector. The views expressed by any such person are the views of only that individual as of the time expressed and do not necessarily represent the views of Fidelity or any other person in the Fidelity organization. Any such views are subject to change at any time, based upon markets and other conditions, and Fidelity disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Fidelity Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Fidelity Fund.

Stock markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments.

Investing involves risk, including risk of loss.

Past performance is no guarantee of future results.

Diversification and asset allocation do not ensure a profit or guarantee against loss.

All indices are unmanaged. You cannot invest directly in an index.

Index definitions

Standard & Poor’s 500 (S&P 500®) index is a market capitalization-weighted index of 500 common stocks chosen for market size, liquidity, and industry group representation to represent U.S. equity performance.

Third-party marks are the property of their respective owners; all other marks are the property of Fidelity Investments Canada ULC.

© 2019 Fidelity Investments Canada ULC. All rights reserved.

U.S: 875556.1.0 CAN: 136215-v2019228

Author

Jurrien Timmer | Director of Global Macro, Fidelity Global Asset Allocation Division

Jurrien Timmer is the director of Global Macro for the Global Asset Allocation Division of Fidelity Investments, specializing in global macro strategy and tactical asset allocation. He joined Fidelity in 1995 as a technical research analyst.

Copyright © Fidelity Investments