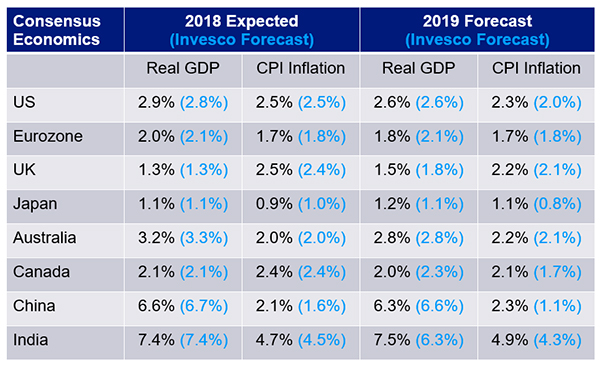

Key takeaways

- 2018 has been a year of turmoil, but, 2019 promises to be much calmer, in my view.

- I believe the Federal Reserve should be successful in positioning the US economy for several more years of expansion.

- Monetary policy invariably dominates fiscal policy in the determination of inflation

2018 has been a year of turmoil with weakness in the bond markets and two significant sell-offs in equity markets. In between there were crises in Venezuela, Argentina and Turkey; ongoing Brexit negotiations; a strong rise in the price of oil; and disruptions created by US President Donald’s Trump’s repeated trade measures — all set against a backdrop normalising US interest rates. However, 2019 promises to be much calmer, in my view.

Though individually damaging, it is my view that these geopolitical events will prove to be no more than waves on the surface of the tide which is the record-breaking expansion of the US business cycle.

United States

US monetary policy is becoming less accommodative, but the Federal Reserve (Fed) is not “tightening,” only “normalising” policy. The current “normalisation” phase is analogous to the mid-course corrections in interest rates that occurred in 1994-95 and 2004-05. The important point about those episodes was that the business cycle continued to expand for several years after the completion of normalisation, and the equity and real estate markets also peaked considerably after these rate hikes were completed.

I believe there is a strong probability that the Fed will be successful in positioning the US economy for several more years of expansion after 2019 or 2020, when the federal funds rate is expected to reach the “neutral” level — i.e., the rate that is neither expansionary nor contractionary, but consistent with steady-state expansion. This would mean that by July 2019, the current expansion would exceed the longest recorded expansion in US financial history — the 10-year expansion of March 1991-March 2001.

There are two broad strands of thinking in the financial markets that run contrary to my view and imply that the US economy is on the cusp of overheating and a resurgence of inflation:

- The first theory points to tightness in the labour market – as indicated by the low rate of unemployment. These analysts rely on the “Phillips curve” to argue that when the unemployment rate has fallen in the past, wages have generally risen, and higher inflation has followed. The problem with this theory is that while it has worked sometimes in the past, it has not worked during the last three business cycles. The theory only worked when money growth was rapid, giving rise to overheating and inflation. In recent years money growth has been low and stable, with the result that the economy is not overheating. Indeed, if we look at Germany, Japan or Israel, the unemployment rate is also at record lows, and yet these economies are not seeing wage or price inflation in any significant degree.

- The second theory claims that a big increase in the budget deficit due to an expansionary fiscal policy will also lead to inflation. But while Trump’s tax cuts and the temporary 100% expensing of investment in a single year have boosted consumption and investment spending in the short run, monetary policy tends to dominate over fiscal expansion. This means there can be no assurance that there will be overheating and inflation. I believe that, despite the low level of unemployment and Trump’s fiscal stimulus, the course of the US economy will remain broadly consistent with the Fed’s mandate to achieve full employment with 2% inflation. This, in turn, should limit the upside risk for interest rates and inflation. By the same token, it should limit the downside risk for the stock market and the bond market, in my view.Turning to trade: The tariffs that have been put in place in 2018 are potentially damaging to trade volumes and will raise the cost of imports for US businesses and consumers. But the important thing to remember is that if domestic spending on consumption and investment is maintained, the damage from tariffs should be minor. There are two reasons why:

I believe that, despite the low level of unemployment and Trump’s fiscal stimulus, the course of the US economy will remain broadly consistent with the Fed’s mandate to achieve full employment with 2% inflation. This, in turn, should limit the upside risk for interest rates and inflation. By the same token, it should limit the downside risk for the stock market and the bond market, in my view.

Turning to trade: The tariffs that have been put in place in 2018 are potentially damaging to trade volumes and will raise the cost of imports for US businesses and consumers. But the important thing to remember is that if domestic spending on consumption and investment is maintained, the damage from tariffs should be minor. There are two reasons why:

- Trade enters the gross domestic product (GDP) growth calculation mainly from the change in the trade balance and the pass-through to domestic prices. The trade measures have not yet shown up in volume terms as Chinese and other exporters rushed to fulfill orders ahead of the increased tariffs, and the contribution of a change in import prices is small compared with the volume and price contributions of consumption and investment.

- The experience of the notorious Smoot-Hawley tariffs of 1930 has been exaggerated. In the past many historians and commentators wrongly blamed the tariffs for the Great Depression. However, the Smoot-Hawley taxes were imposed at a time when domestic demand was collapsing due to mistakes of monetary policy. The lesson: Provided central banks today ensure that money and credit continue to grow, there is no reason to fear a 1930s-style outcome.

Eurozone

Given that fiscal policies in the eurozone are expected to remain restrictive, that leaves monetary policy as the only possible source of macro-economic policy change. In this area, the key feature has been the European Central Bank’s (ECB) tapering of its asset purchases (which are due to end in December) and the associated forward guidance on interest rates next year. ECB President Mario Draghi has said that interest rates are unlikely to increase before summer 2019.

However, it is worthwhile to remember that while quantitative easing (QE) describes monetary policy as it affects the central bank’s balance sheet, and while market participants obsess about interest rates, what matters much more is the growth of money in the hands of the non-bank public. In principle, the key consideration for ending asset purchases or QE should be whether commercial banks are creating sufficient loans that bank deposits (on the other side of their balance sheets) or money growth can continue independently of ECB purchases. Here there is a problem because many eurozone banks are still nursing portfolios of non-performing loans while trying to build up capital, and consequently loan growth has been well below money growth. Terminating the ECB’s asset purchase policy while European banks remain in a fragile condition means that the region will be vulnerable to another slowdown in nominal spending and poses the risk of inflation falling back towards deflation.

United Kingdom

Public debate has been dominated by the details of the negotiations for the UK’s withdrawal from the EU. Although on the surface consumer spending seems quite normal, there has been a slowdown of investment pending the emergence of a clear agreement on the post-Brexit trading environment. House prices in the London area have been static since the start of 2018, and one of Jaguar Land Rover’s factories in the West Midlands has announced that 2,000 staff will move to a three-day week, suggesting that Brexit could lead to a considerable drop in corporate investment.

Meanwhile economic growth as measured by real GDP has slowed from an average of 2.1% in 2015-16 to an average of 1.5% in the six quarters since the start of 2017, with most of the slowdown in business investment. Until business leaders obtain a clear framework for the environment in which they will operate after March 2019, their capital expenditure and hiring plans will remain at least partially on hold.

The same hesitancy has applied in the implementation of monetary policy. Having given clear signs earlier in the year that interest rates would be rising, the Bank of England’s Governor, Mark Carney, and his Monetary Policy Committee voted not to raise Base rate in February and May, but finally raised it by 0.25% to 0.75% in August. However, money and credit growth have been slowing in the background over the past two years.

Japan

The Japanese economy continues to experience sub-par growth and sub-target inflation. Despite five years of aggressive QQE (quantitative and qualitative easing) by the Bank of Japan, little progress has been made in restoring growth and particularly inflation to normality. The economy continues to grow at a modest pace of 1.0-1.5%, due largely to the aging of the population which has meant that the workforce has been declining. Also, QQE has made very little impact on the growth of banks’ balance sheets and hence on money or credit growth, with the result that inflation has remained well below the Bank of Japan’s 2.0% target. I expect little change in 2019.

China and smaller east Asian economies

China is confronting the challenge of deleveraging while attempting to maintain growth by intermittent easing of monetary policy (e.g., cutting reserve requirement ratios, relaxing macro-prudential controls on mortgage lending, and easing some money market interest rates). These moves to ease policy are best seen as a modest counter to the key policy priority of reducing leverage.

Meantime real GDP has slowed and is likely to slow further in 2019. Although some basic industries have recovered from their slump in 2014-16, housing and nominal fixed asset investment have slowed. In my view, none of this activity is likely to pick up significantly in 2019 unless the State Council’s policy of deleveraging is revised. On the external side, the impact of Trump’s tariffs has so far had only a minor impact as exporters have rushed to complete shipments ahead of higher tariffs being imposed from January. In 2019, I therefore expect exports to slow, with only single-digit growth of exports in US dollar terms.

Elsewhere in East Asia, domestic spending has been subdued while export growth has slowed. Looking forward, some smaller, low-cost economies such as Thailand and Vietnam may benefit from some re-allocation of Chinese manufacturing, but the overall outlook will be subject to heightened trade tensions and the “downside risks to global growth” predicted by the International Monetary Fund at its October conference in Bali.

This post was originally published at Invesco Canada Blog

Copyright © Invesco Canada Blog