by Lance Roberts, Clarity Financial

For the last few months, we have repeatedly warned about the mounting risks which were being ignored by an increasingly overly complacent, overly exuberant market. Doug Kass had a good compilation of those concerns on Friday:

- The Fed Chairman seemed more hawkish in tone recently

- Rising interest rates provide an alternative to stocks and reduce the value of long-dated assets.

- Higher inflation (input costs) will pressure corporate margins and profitability.

- A pivot in global monetary policy towards constraint from easing.

- Policy risks.

- Midterm election uncertainties.

- Fiscal policy that has trickled up (not trickling down).

- Our Administration’s trade policy and (as expressed in my missives this week) reversing the post-WWII liberal order holds multiple social and economic risks.

- Increasingly leveraged public and private sectors.

- A leveraged and dangerously weak European banking system who’s left-hand side of the balance sheet is loaded with overvalued assets (like sovereign debt).

- Submerging emerging markets vulnerable to large U.S. dollar-denominated debt that will be difficult to pay off.

- China’s economy is faltering – and its financial system is too leveraged.

- Investor complacency – not a soul in the business media (save the Perma Bears) has warned of a large market markdown since the January highs.

Of course, the sell-off last week was simply more evidence of the influence of “algos gone wild” when technical levels are broken and the robots all hit the “sell” button at the same time. It was also further acknowledgment of the lack of liquidity due to the surge in ETF issuance which has now created a massive amount of overlap risk in the markets.

“When the market goes down, passive fund managers will be forced to sell stocks in order to track the index. This selling will force the market down further and force more selling by the passive managers. This dynamic will feed on itself and accelerate the market crash.” – James Rickards

The same was noted by portfolio manager Frank Holmes as well:

“Nevertheless, the seismic shift into indexing has come with some unexpected consequences, including price distortion. This isn’t just the second largest bubble of the past four decades. E-commerce is also vastly overrepresented in equity indices, meaning extraordinary amounts of money are flowing into a very small number of stocks relative to the broader market. Apple alone is featured in almost 210 indices, according to Vincent Deluard, macro-strategist at INTL FCStone.

If there’s a rush to the exit, in other words, the selloff would cut through a significant swath of index investors unawares.“ – Frank Holmes

Due to massive amounts of Central Bank interventions, combined with low interest rates, investors have been trained to “buy the dips” and disregard everything else. As Frank noted, that bullish mantra has now led to the “second largest bubble in four decades.”

(If you consider the amount of debt and leverage that has been piled on – I would argue this is likely the largest bubble ever as it encompasses so many different asset classes at the same time.)

So, is this time different? Should we just “buy the dip” and keep ignoring everything else?

I am not so sure.

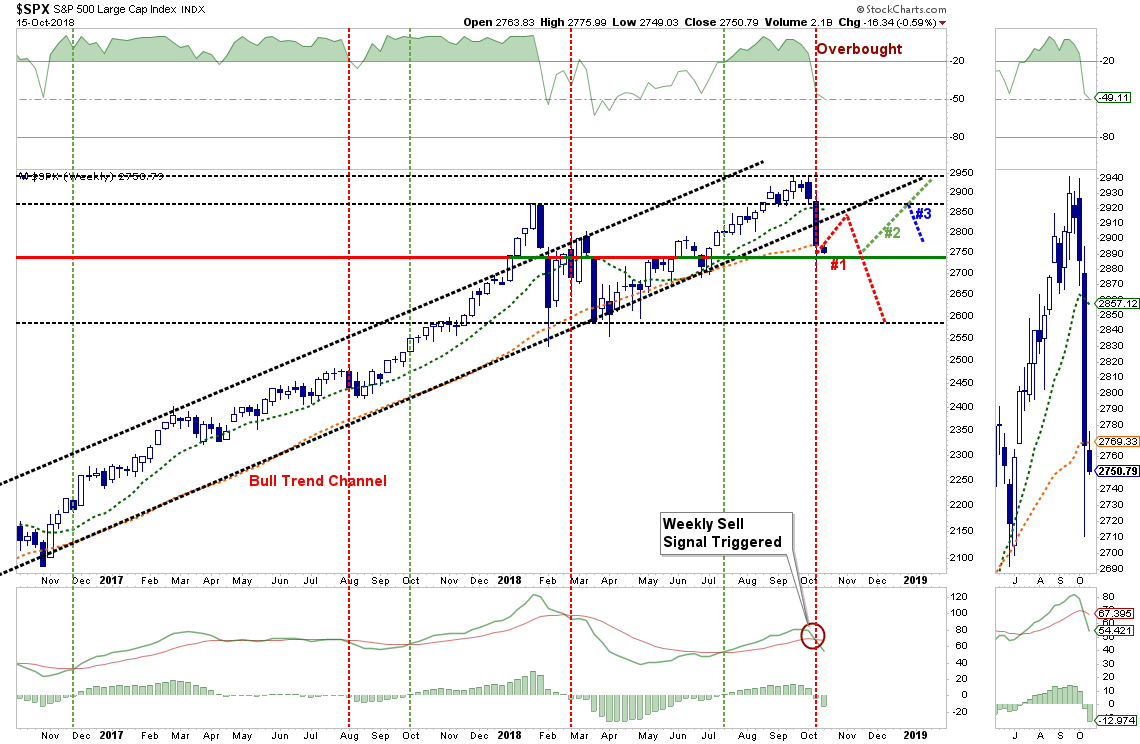

As I noted this past weekend, the technical backdrop to the market has changed for the worse. To wit:

“With the understanding the economic and fundamental background may not be supportive for higher asset prices heading into 2019, the market is also sending a very different technical signal as well. As I showed on Thursday, this is the FIRST time the market has broken the bullish trend line that began in 2016.

As shown below, that break of the bullish trend pulls in a new dynamic of potential market action over the next several months which is more akin to a market topping process than the continuation of the previous bullish trend.”

“Given the short-term OVERSOLD condition of the market, we want to use rallies to rebalance risks in portfolios.

#1 – A rally back to the bullish trend line will be used to reduce risk (ie. raise cash) in portfolios by selling lagging positions and rebalancing risk in winning positions. Rule: sell losers and let winners run.

We fully expect an initial rally to fail as investors caught in the sell-off will be looking for an opportunity to sell. However, if that sell-off fails to hold support at the recent lows it will suggest a bigger corrective action is in process. We will be looking to reduce equity risk further, raise cash, evaluate portfolio allocation models.

#2– If the sell-off following a failed rally holds support at the recent lows, and turns up, such will suggest a rally back to either the January highs or all-time highs. NOTE: A rally back to all-time highs following a corrective pullback will again retest the underside of the bullish trend line from the 2016 lows. Such remains a ‘bearish’ backdrop from equity risk going into 2019 where economic and earnings data is expected to slow further. We will use any rally back to those levels to reduce risk as noted in #1.

#3– If the rally from the recent lows fails at the January highs we will again use that opportunity to reduce equity risk and rebalance portfolio allocations.”

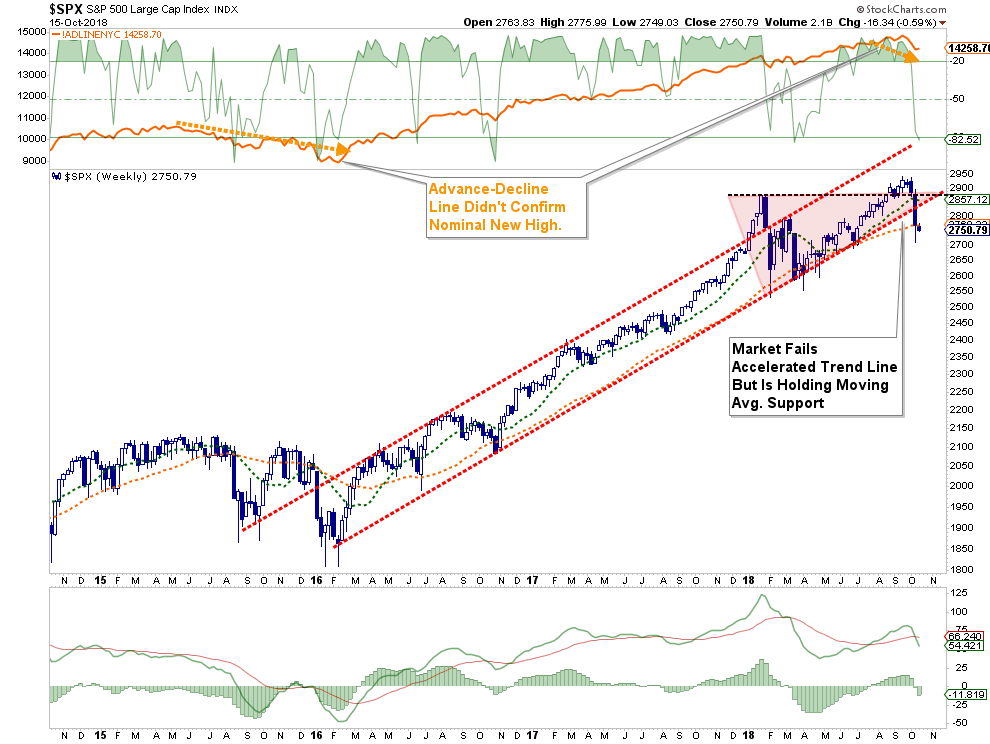

The chart below pulls that analysis back to the 2015-2016 correction where you can see the trend more clearly.

The nominal “new highs” in 2015 were not confirmed by a strengthening cumulative advance-decline line which suggested a correction was likely. The same non-confirmation was also evident with the most recent nominal new highs in September. As noted above, the break below the bullish trend line, combined with the downside break of the consolidation from the January highs, changes the entire tenor of the market heading into the end of the year.

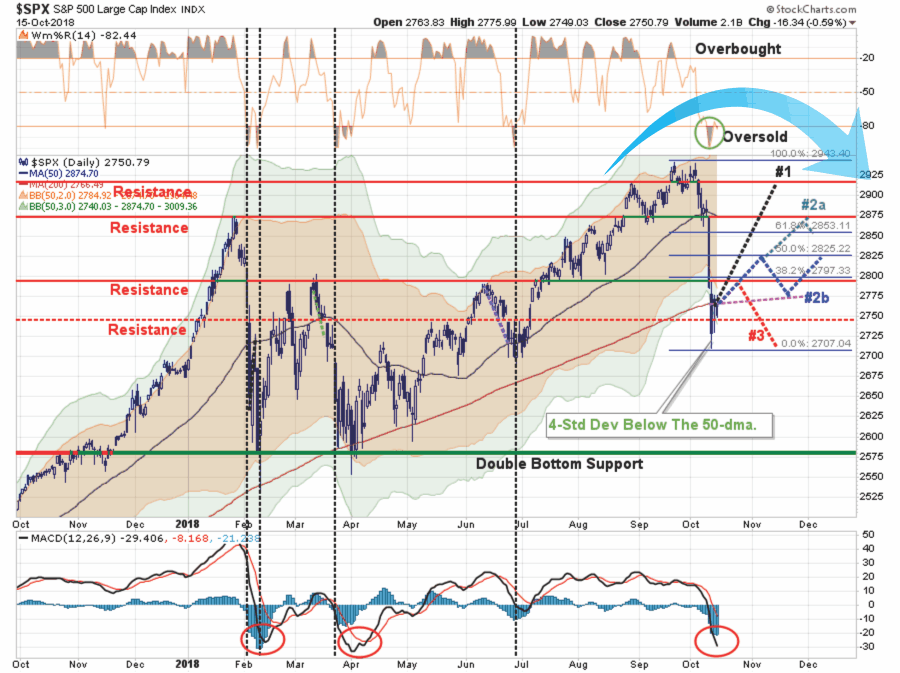

When we switch from weekly to daily analysis, we can update our ongoing “pathway analysis” which we have been producing each week since January. The following chart is updated through Monday’s close.

No matter how many different paths I trace out, the possibilities of the market rallying back to new all-time highs this year have been greatly reduced. As noted, all four possibilities continue to suggest a broader topping pattern in place through the end of this year.

Pathway #1: The most bullish outcome would be from a strong earnings season, combined with a pickup in economic activity from the two most recent Hurricanes, which pushes markets back to resistance near all-time highs. While this is certainly entirely possible, there is a tremendous amount of technical damage to overcome between current levels and that high point. (10%)

Pathway #2a: The market rallies from current levels to the January high. Again, this would likely be fueled by a stronger than expected earnings season and a pickup in economic activity. However, the run to the January highs is capped by that resistance but the market finds support at the 62% Fibonacci retracement level just below. (30%)

Pathway #2b: The most feasible rally from current oversold levels is back to the 50% Fibonacci retracement of the recent decline. The market gets back to very overbought conditions and the market begins to trade between the 200-dma and/or the 32% Fibonacci retracement level. (30%)

Pathway #3: The biggest concern, given the technical deterioration, the threat of weaker economic and earnings growth, and the possibility of a Mid-term election upset, is a rally back to the 32% Fibonacci retracement level which coincides with the previous resistance at the May highs. A failure at the point would likely lead to a sell-off that pushes the markets back to retest last week’s intra-day lows. Lower lows become a real threat. (30%)

Here is the bottom line:

While a year-end rally is certainly feasible, the probability of the markets setting new highs has been markedly reduced.

As I have repeatedly discussed over the last several weeks, prudent portfolio management practices reduce inherent portfolio risk thereby increasing the odds of long-term success. Any rally that occurs over the next few days from the current levels SHOULD be used as a “sellable rally” to rebalance portfolios and related risk. These practices align with our most basic investment rules/philosophies as noted above.

- Sell positions that simply are not working. If they are not working in a strongly rising market, they will hurt you more when the market falls. Investment Rule: Cut losers short.

- Trim winning positions back to original portfolio weightings. This allows you to harvest profits but remain invested in positions that are working. Investment Rule: Let winners run.

- Retain cash raised from sales for opportunities to purchase investments later at a better price. Investment Rule: Sell High, Buy Low

Remember, we can ALWAYS add money back into the markets once the evidence of the continuation of a bull market is available.

Until then, we are going to err on the side of caution.

Copyright © Clarity Financial