by Craig Basinger, Chris Kerlow, Derek Benedet, Shane Obata, Connected Wealth, RichardsonGMP

In an ideal world, any important decision we make in life would go through a rigorous and disciplined process, designed to lead us to the answer most likely to be correct or of greatest probability weighted benefit. This would include assessing all potential options available, the potential outcomes of each option, analyze the consequences including the probability of uncertain events occurring, then make the best decision based on the information available. Sadly, this type of rigorous decision making process is rarely used because it takes a lot of time, energy and resources. Instead we tend to be lazy and more often rely on mental short cuts or our ‘gut’ to make decisions. This saves us tons of time and fortunately often leads us to the correct decision, at least most of the time. However, these short cuts can sometimes lead us to make sub-optimal decisions.

Behavioural finance is the study of how we make decisions. It has a special focus on how and when our shortcuts, labelled behavioural biases, are likely to mislead us. This research displine is gaining more and more attention outside academia, with notable traction in the world of investing.

Investing is really all about making important decisions, with imperfect information, in an uncertain world. In this environment, we would expect the rise of behavioural finance to continue for some time. Understanding many of the behavioural biases and how they can mislead our decision making process can help avoid, or at least mitigate the risk of making a bad mistake.

Behavioural Biases

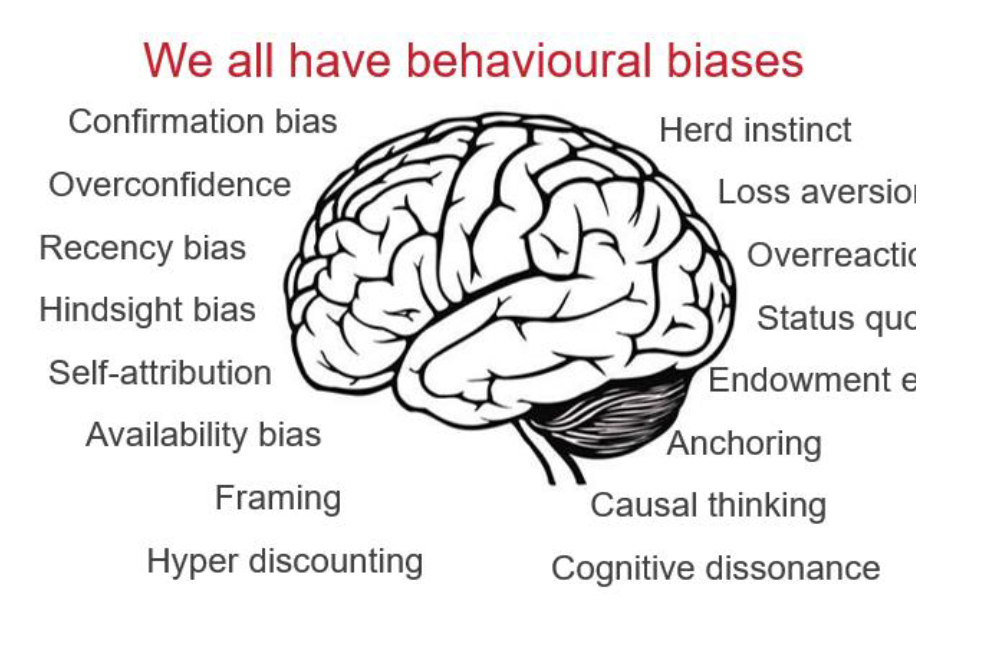

There are many behavioural biases that have been identified and researched over the years. Behavioral Economics Guide 2018 identifies roughly 100. Don’t worry, we are not going through them all. However there are some that are more important than others when it comes to investing.

We believe the most important biases are those that have the biggest potential of leading an investor to an incorrect decision and also have the biggest potential negative impact. Some of the more important biases are listed around the brain to the right.

Behavioural biases are evident in all of us. They impacts how we think, process information and make decisions. However the influence of these biases varies from person to person and from situation to situation. When emotions are elevated, many biases tend to become more evident or elicit a stronger influence on decision making. Who you are is also a key determinant of which biases you may be most at risk.

Investors tend to suffer from some, while advisors or financial professionals tend to suffer from others. In the following section we will dive into a few that are common for investment advisors, how they can cause poor investment decisions and some technicques to mitigate or correct the mistakes.

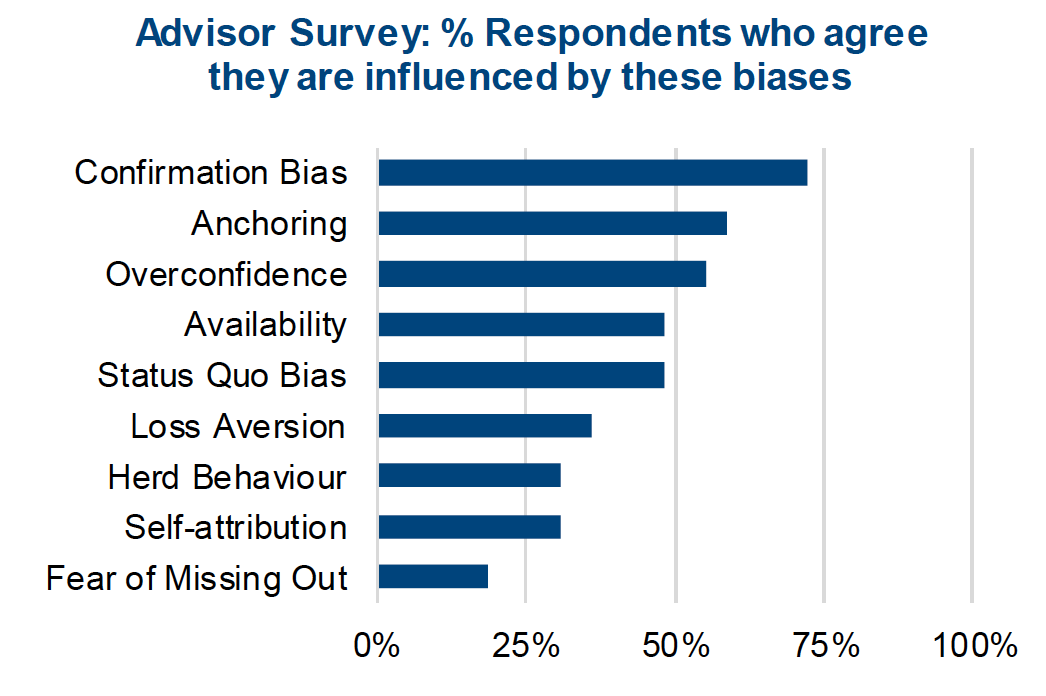

It should not come as a surprise that behavioural biases differ between investors and those providing professional investment advice. Most investors are only involved in investment decisions on a sporadic basis, potentially when changes are being made to their portfolios. Most other times they are more focused on other aspects of everyday life. Meanwhile those providing professional investment advice are involved in making financial decisions, research, analysis and monitoring just about everyday given this is their profession. In a later Market Ethos we will dive into the behavioural biases that most impact individual investors such as herd behaviour, performance chasing, status quo bias and loss aversion. Today’s ethos is all about biases most evidend in advisors, including Overconfidence, Anchoring and Confirmation biases.

The top chart is a survey of financial professions asked whether they are influenced by certain biases. While survey results should always be taken with a grain of salt as respondents will often answer as they would like to see themselves or how they believe the surveyer would like them to respond, the survey findings actually line up with other research. Those biases near the top of the list are most evident in people actively involved in the investment decision process (advisors) and those near the bottom are more evident in those less involved in the investment decision process (investors).

Confirmation Bias

What it is: This is our tendency to seek out information or views that are aligned with our pre-existing opinion or thinking on a topic. This bias also causes us to ignore or discount contrary views. We do this because it actually makes us happier reading or listening to views that reinforce ours, gives us greater confidence in our beliefs.

Investment Process Risk: Confirmation bias is a serious risk to the investment decision making process from a few perspectives. Focusing mainly on research or ideas that aligned with our views can lead to increased portfolio concentration, becoming so emboldened that we are right that we continue to add to a theme, industry, stock, etc. It can also cause us to miss a change in market as you often discredit contrary information. As an example: today many believe Amazon will dominate the world. Not questioning the great company, but many thought the same of Xerox in the 1970s, IBM in the 1980s and the four horsemen of the internet in the 1990s.

How to Defend against this bias – The good news is confirmation bias is often easy to spot and we can catch ourselves just by knowing about it. Other tools include considering why or how we may be wrong in our pre-existing views. What could go wrong with a specific investment or strategy and are we able to put a probability on it? Just by doing this excercise actually opens up our minds to contrary opinions.

Another technique it to force ourselves, or someone on your team to make the counter argument. As an example: our asset management team is bullish on the U.S. dollar but we will often task some members to make the opposite argument. This results in a more balanced view and reduces the chance of being materially surprised.

Overconfidence Bias

Overconfidence is evident in advisors/portfolio managers in the professional finance industry. They often believe their skills will enable them to pick stocks or funds that will outperform. Most of the evidence refutes this belief.

Investment Process Risk: Overconfidence is popular in most professions, including finance. Having confidence in your your views is fine, as long as there is an unstanding the views could be wrong. Letting overconfidence cloud your decision making is the risk. This can lead to under-diversification and excessive trading or performance chasing.

How to Defend against this bias: The markets are a dynamic system that are influenced by the participants. Believing you can solve it is hubris. Understanding your views and how they could be wrong helps. Asking another professional to challenge and poke holds in your views helps.

Anchoring

What it is: Anchoring is usually how exposure to a number ahead of a question can influence your answer. In the investment world anchoring is how investors can become anchored by their original purchase price or another arbitrary price level, such as a high that was previously reached. This is partially related to loss aversion.

Investment Process Risk: No one wants to sell something below what they paid for it, or sell something below a previous high. Anchoring an investment decision on a price can lead to bigger problems. Remember, the stock or market does not know or care what you paid for something. This bias can lead you to holding onto loser way too long, some of which continue to lose.

How to Defend against this bias: Ignoring any reference to original costs or other potential achors can help. As an example in the portfolios we manage, there is no reference to cost anywhere on our spreadsheets. Position size and weight in the portfolio is much more important. Only after a decision is made is the cost considered for tax purposes, which can change the final decision. If you believe you are anchored to a price, getting a second opinion on a potential trade can help. Presumably the second opinion giver won’t be as emotionally tied to the anchor price.

*****