by Valerie Grant, Michelle Dunstan, Equities, AllianceBernstein

Investing in companies that have favorable ratings on environmental, social and governance (ESG) issues has become increasingly popular. But investors might do better targeting companies with poor ESG ratings and a clear commitment to mend their ways.

Searching for companies with weak ESG records might sound counterintuitive. But in fact, identifying companies that are on track to materially improve their ESG performance can yield positive outcomes for both investors and society.

Investors play an important role in motivating these companies to change, through active engagement, proxy voting and other tools available to active managers. Companies that successfully change their ESG practices—what we call “ESG Improvers”—are often on a path to improving their financial and operational performance, which drives better returns.

What’s Wrong with ESG Ratings?

ESG ratings are the backbone of responsible investing. They provide a snapshot of a company’s performance on a range of issues, from protecting the environment to gender equality. But they can be misleading. They don’t really help investors identify companies that are ready to change. And our research has shown very little correlation between ESG ratings and excess returns.

MSCI, a leading ESG ratings provider, has demonstrated a correlation between improving ESG ratings and investment returns. Our research confirms this correlation and shows that companies with the lowest ESG ratings—or no ratings at all—deserve special attention.

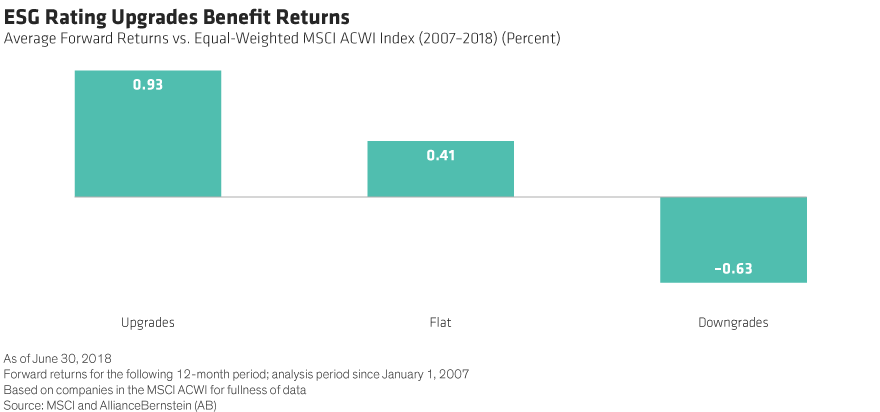

The Redemption Effect

Companies at the low end of the ESG spectrum benefit most from rating upgrades. We analyzed the relative returns for companies with ESG rating upgrades over more than a decade. On average, stocks with upgrades outperformed an equal-weighted MSCI ACWI Index during the next 12 months by 0.93%, while stocks that were downgraded lagged (Display).

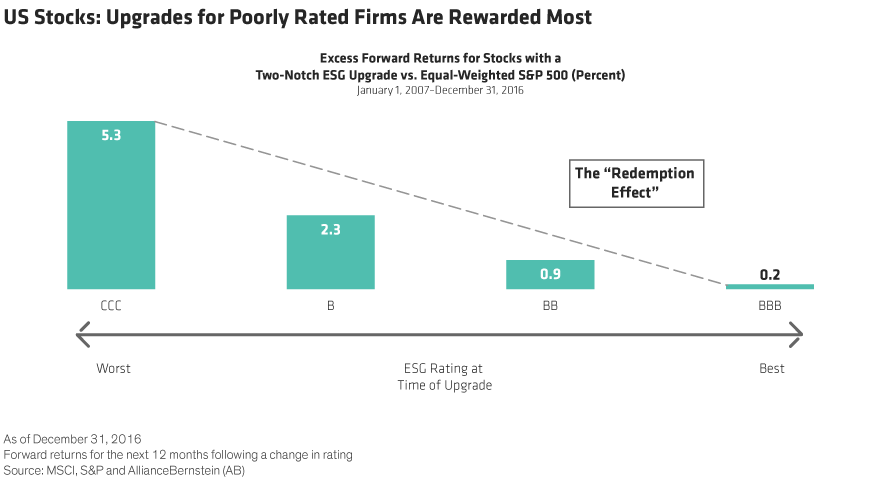

In the US, poorly rated companies that were upgraded generated the strongest rewards (Display). We call this the “Redemption Effect.” Stocks with the worst ESG rating—CCC—that received a two-notch upgrade outperformed the S&P 500 Index by more than 5% in the 12 months following the upgrade. Companies with better ESG ratings—BBBs—barely beat the benchmark despite similar levels of improvement.

The Redemption Effect should prompt investors to rethink their approach to ESG. Just as value investors target undervalued stocks facing a controversy with a turnaround potential, we think investors should look for companies with poor ESG records that are likely to redeem themselves with more responsible practices.

Third-party ESG ratings do have some value. They can help investors understand the current position of a company on ESG issues. However, they don’t help predict how a company may change its behavior—or how its stock returns could be affected. That’s why fundamental investment research and active engagement with companies on ESG issues are essential to implementing an effective “ESG Improvers” strategy.

Emerging Markets: Fertile Ground for Finding Improvers

While ESG improvers can be found around the world, emerging markets offer especially fertile ground for investors. Emerging-market companies tend to have lower ESG ratings than developed-market peers, and there are relatively more companies that haven’t been rated at all. As a result, there are more opportunities for investors to unearth companies with improvement potential.

Anhui Conch Cement, a Chinese cement manufacturer, is a case in point. The company has a low CCC rating because of its subpar disclosure practices. Yet our research suggests that Conch consumes 28% less energy to produce cement than its BBB-rated peers. Current ESG ratings penalize the company for a lack of transparency—but fail to recognize its potential for improved ratings when its superior energy efficiency is acknowledged. As investors in Conch, we helped the company understand how to provide MSCI with data that could lead to an ESG upgrade.

Norilsk Nickel, a Russian mining and smelting group, suffered from a poor CCC ESG rating because of high emissions. However, the MSCI rating was based on a five-year average and didn’t take into account the company’s plans to upgrade its facilities and shut an obsolete smelter. Engaged investors could detect these changes, which led to a substantial reduction in emissions well before MSCI raised its ESG rating of Norilsk to B in December 2017.

These examples show why fundamental research and differentiated insight is needed to distinguish between chronic ESG offenders and reforming companies. We think it’s worth the effort. Investors who want to promote real societal improvements without sacrificing return potential should look for companies with share prices that don’t reflect their determination to clean up their ESG act.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

Nelson Yu, Alex Pizzirani and Amy Yang contributed to this analysis.

Copyright © AllianceBernstein