by Shamaila Khan, Christian DiClementi, AllianceBernstein EM Income, AllianceBernstein

Summer is just beginning, but emerging-market (EM) bonds and currencies have been on a roller-coaster ride for months now. In markets, though, volatility breeds opportunity—and we still see plenty of that among EM issuers.

When 2018 began, we warned investors to be prepared for volatility and a faster-than-expected rise in US interest rates. But we also noted that strong global growth and improved economic fundamentals in much of the developing world have made emerging-market debt (EMD) less vulnerable to external shocks.

That view has been put to the test over the past six months as a sharp rise in US interest rates and the US dollar, and simmering trade tensions, provoked a broad sell-off in EMD assets—dollar-denominated bonds as well as local debt and currencies.

Such broad moves across EMD can obscure the differences between countries, companies and individual securities. The way we see it, the broad-based decline in prices creates an opportunity to add exposure to countries and companies with strong fundamentals that have been unfairly punished.

Less Vulnerable to Outflows

Not all EM borrowers are as vulnerable to a rising dollar as they once were. Many countries have reduced their current account deficits in recent years. That makes them less dependent on capricious portfolio inflows.

At the same time, foreign direct investment (FDI)—a more stable source of funding because it tends to be long term in nature—has increased. Over the past few years, we’ve seen EM basic balances, which combine current account position and FDI flows, improve in every region of the globe.

The most highly indebted borrowers are more exposed, of course. Yet how policymakers react to crises matters. Argentina and Turkey both suffered runs on their currencies in the second quarter. But Argentina’s central bank arrested the decline by swiftly hiking rates while the government lined up International Monetary Fund support. Turkey’s central bank waited weeks before acting, and has been subject to criticism from the country’s president, raising concerns about the independence of Turkey’s central bank.

Put another way, the quality of policymaking and government effectiveness clearly differs across EM countries. That’s why it’s so important for investors to be selective and deliberate about where they invest.

EM Corporates More Resilient

EM companies are less exposed to changes in the dollar than investors may realize, too. Many that borrow in US dollars tend to do so because they have a natural affinity for the currency. For example, their export revenues may be dominated in dollars, which acts as a natural hedge against their dollar liabilities. For these types of firms, a rising dollar is good news because it boosts their margins, which leads to higher cash flow and creditworthiness. Other firms keep their dollar liabilities manageable by hedging them back to their home currencies.

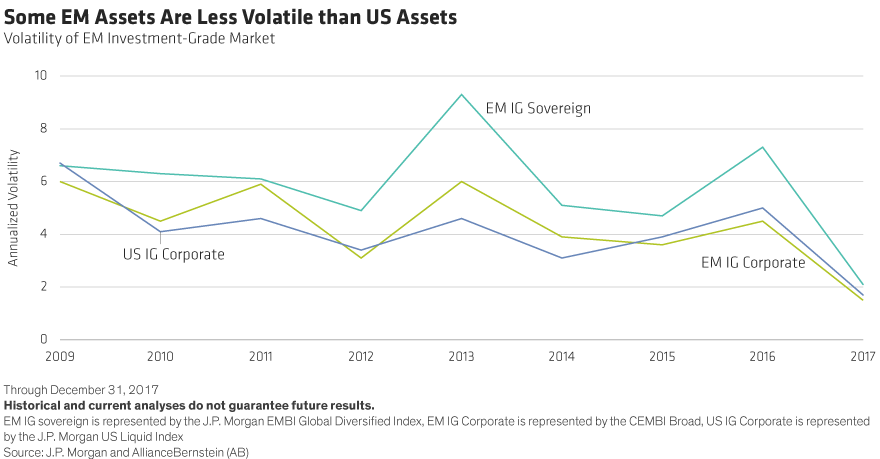

EM corporates with investment-grade ratings have also become much less volatile investments. In fact, over the past three years, high-grade EM corporates have been less volatile than their US counterparts (Display). This is partly because the buyer base has improved: these assets tend to attract large institutional investors with longer investment horizons.

Monitor Risk, but Keep It in Perspective

There are always risks to monitor. But it’s important to keep them all in perspective.

Let’s start with trade. The rhetoric has been troubling, particularly from the US administration. But so far, the pattern (with regard to the NAFTA talks, the Trans-Pacific Partnership and the US-China disputes) seems to be to start with a threat and then gradually move toward negotiation. In other words, the administration’s bark—so far—seems to be worse than its bite. This could change, of course, and bears watching. And with governments negotiating in public, be prepared for more volatility.

Growth is slowing in China. But global growth remains strong, and so do commodity prices, in part because China has been scaling back its mining for environmental reasons, and major oil producers have been cutting supply. That’s good news for EM countries that are net exporters of commodities.

Finally, there’s political risk. This never goes away, and key elections in Mexico and Brazil this year could lead to more short-term turbulence. But other recent events—the Italian elections, the rise of Donald Trump, Brexit—have injected political risk into developed-market assets, too. Yet in most cases, investors aren’t being paid for it.

EMD investors are. For example, dollar-denominated high-yield EM sovereign debt has rarely been cheaper. As of June 8, it offered a yield pickup of about 1.65% over US high-yield corporate bonds, according to J.P. Morgan data. The spread between the two has been that high less than 10% of the time. For careful investors, this may present an attractive relative-value opportunity.

We still think robust global growth, prudent policymaking and smaller deficits will help fortify many key EM countries against external shocks, and we still see value across EMD assets. In particular, investment-grade EM corporate bonds have been remarkably steady in today’s volatile markets and may appeal to investors who want to boost their return and income potential without taking undue risk.

With volatility likely to stay high this year, it’s important to carefully manage overall portfolio risk and to pinpoint tactical opportunities. That means staying active and taking advantage of broad downturns to pick up assets at attractive prices. And for long-term investors with the luxury of long time horizons, today’s conditions present an opportunity to add value in one of the most rapidly growing sectors in the global fixed-income market.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Copyright © AllianceBernstein