Markets Unfazed by Rising Risk of Populism in Italy…for Now - Context

by Fixed Income AllianceBernstein

While Italy’s bond yields have risen, investors have so far reacted relatively calmly to the rising probability of a populist Italian government. Based on the fundamentals, the potential downside scenario looms larger than markets seem willing to consider.

After weeks of feverish negotiations (and with a last-minute request for more time), the anti-establishment Five Star Movement (M5S) and right-wing League (formerly the separatist Northern League) are working to reach an agreement to form Italy’s next government. It’s uncertain how long such a government would last, but populist leadership could have big implications for Europe’s markets.

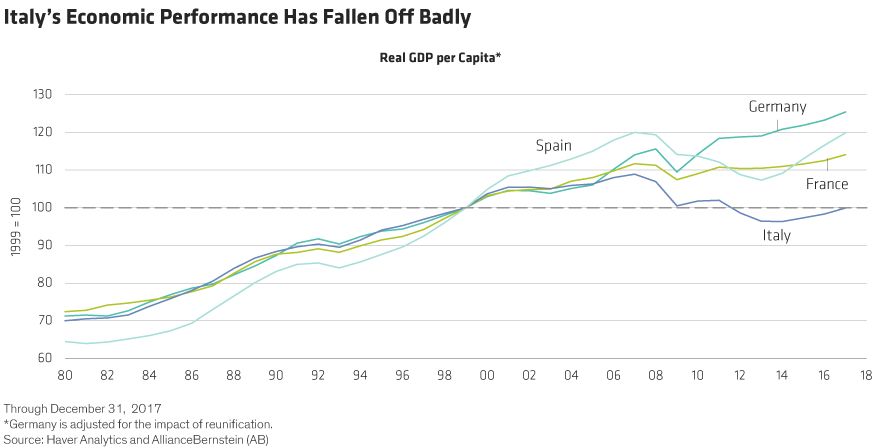

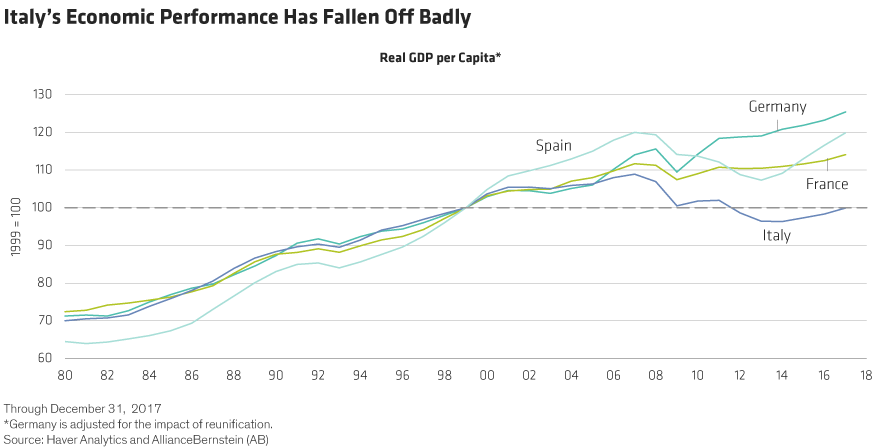

The arrival of a populist government in Italy should come as no real surprise—not even to Europe’s political establishment. As we’ve highlighted in the past, Italy’s recent economic performance has been truly abysmal. And, coincidence or not, its relative position has deteriorated markedly since it joined the euro (Display).

Capital Markets Shrug Their Shoulders

So far, financial markets have reacted relatively calmly to these developments, with the yield spread between the 10-year Italian bond and German Bunds rising from a low of 113 basis points in late April to 156 basis points as of May 17. However, this only takes the spread back to where it was at the beginning of January.

The most obvious reason for the modest reaction is that European Central Bank (ECB) bond purchases continue to provide a backstop for the market. And Italy’s yield spread versus Spain suggests that a political risk premium is already attached to Italian bonds (Display).

There are other plausible explanations. Investors may think that the government won’t last long—or that it will act very differently once it gets to sit at the high table (think Greece’s Syriza). The market probably also draws some comfort from the recently toned-down anti-euro rhetoric of both M5S and the League.

Collision Course with Brussels and Creditor Nations?

But there’s also a clear element of complacency at play in the market’s modest reaction.

There are considerable differences between the electoral platforms of M5S and the League, but the parts they can agree on—repealing the 2011 pension reform, tax cuts, minimum incomes and higher spending—are likely to put Italy on a collision course with Brussels and the euro area’s creditor nations. And recent comments from both parties suggest they are happy to precipitate a confrontation.

If a new government pursues these policies in earnest, it will also put the ECB in a tough spot. Quantitative easing has provided support for peripheral bond markets, but the turning point in the sovereign-debt crisis was ECB President Mario Draghi’s “whatever it takes” speech in mid-2012.

That speech was ultimately the result of a grand bargain—Italian President Silvio Berlusconi resigned (November 2011), the fiscal compact was signed (March 2012), Draghi delivered the speech (July 2012) and German Chancellor Angela Merkel supported the ECB president despite the Deutsche Bundesbank’s protests.

If a populist Italian government does decide to openly flout the euro area’s budget rules, we’ll end up with a classic fiscal free-rider problem (think Greece pre-2010 or an International Monetary Fund program with no conditions). There are likely to be limits to the ECB’s and/or German government’s tolerance for such a situation, particularly given the example it would set for other countries.

More Downside than Upside Risk

So, what are the market implications? It’s certainly possible that the consensus view is right and that the bark of a M5S-League coalition will be worse than its bite—or that the coalition will be so short-lived that it will have little impact.

But we struggle to find the positive news that could drive Italy’s bond-yield spreads lower from this point. And we can see that a scenario recently considered a tail risk—a populist Italian government, flouting Europe’s fiscal rules and in conflict with its creditor nations—seems to be playing out before our eyes. And we keep going back to Italy’s woeful GDP per capita charts.

Sooner or later, it seems that something has to give.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Copyright © AllianceBernstein