by Equities, AllianceBernstein

Passive equity strategies have seen massive inflows over the last decade, in part owing to active management’s struggles. But a closer look at the story within the story suggests that leaving active out of the equation could be leaving money on the table.

First, a little history on how we got here.

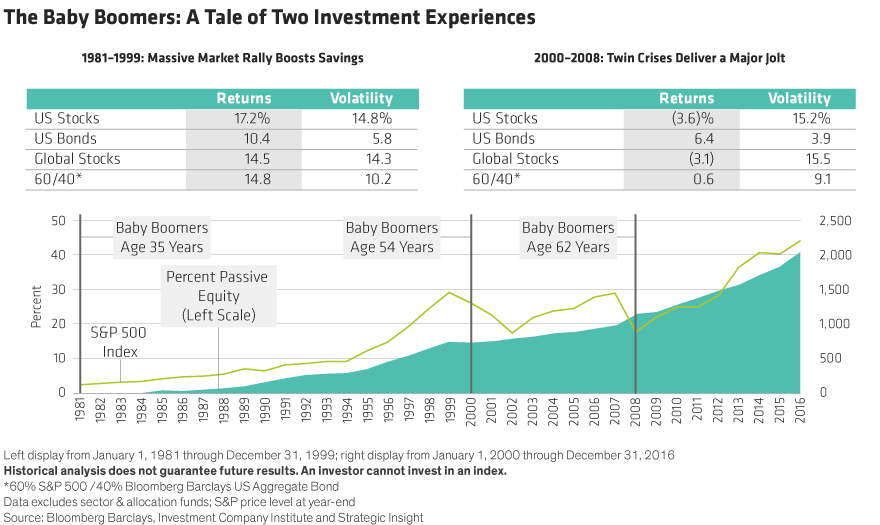

In the early 1980s, the baby boomer generation started to enter its peak earning years—and stepped into the biggest equity bull market in history. From 1981 through 1999, the S&P 500 Index delivered annualized returns of more than 17% (Display). More earnings and a wealth-building rally created a winning formula for investors.

But as the oldest boomers began to approach their retirement years, they were hit with two major market crises—the bursting of the tech bubble and the global financial crisis. This challenging period from 2000 through 2008 left investors reeling, with their wealth eroding just as retirement was approaching.

As a result, many baby boomers took a fresh look at how they thought about investing. One of the prevailing thoughts: “Active management didn’t help me defend in the downturns.”

That line of thinking sparked a broader assessment of active management’s struggles. With that in mind, investors sent a wave of money into passive strategies.

What Was Behind the Active Slump?

It’s certainly true that active managers—as a group—underperformed over time. But the success of active managers also varies a lot, based on important factors such as the specific time period, the equity category and how active a manager actually is.

We see two structural themes behind active’s slump.

First, actively managed assets and asset managers’ staffs grew explosively in the 1990s. A growing number of alpha seekers made it harder for active managers to add value. Second, many active managers that had raised large amounts of assets became less active. They managed closer to the benchmark—perhaps to avoid underperforming and losing a growing amount of client assets in a strong bull market.

In terms of the underperformance, there are many ways to analyze the numbers. One well-known academic study1, covering the years from 1990 through 2009, compared the degree of managers’ activeness with relative performance versus benchmarks. As a group, active managers underperformed—after accounting for fees—by about 40 basis points per year.

But on closer examination, the most active 20% of managers fared quite well. These “diversified stock pickers,” defined by low tracking error and high active share, beat their benchmarks by 1.26% on an annualized basis. The takeaway: True stock pickers provide the greatest opportunity for outperformance.

Market Environment Makes a Big Difference, Too

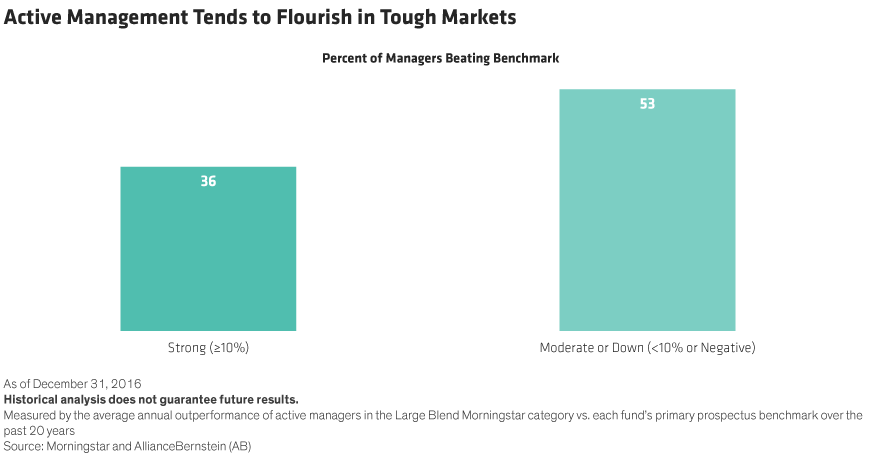

The market environment also plays a big role. In the great rising tide of strong beta-driven markets, the individual boats of active management don’t really matter. Volatility tends to be low—and so is dispersion. When equity market returns were 10% or higher, only one-third or so of active managers beat their benchmarks (Display). In fact, the toughest times for active are when the market is rising and valuations are expanding.

But when market returns were under 10%, over half of active managers outperformed. In other words, when the tide wasn’t rising as high or was falling, the individual boats mattered more.

Is the Active-Passive Pendulum Swinging?

Why should these factors matter to investors?

-

The environment ahead seems likely to favor active. Valuations remain elevated and market returns are likely to be lower ahead. With returns likely to be lower and volatility higher, dispersion among individual stock returns seems likely to rise, creating more opportunities for active managers to stand out.

-

It’s only recently that we’ve started to see the return of market drawdowns. In these market conditions, active managers have tended to outperform historically—helping to protect portfolios against the downside.

-

Just as the wave of growth in active management caused structural problems, the surge in passive investing is creating challenges, too. With so much money and so many passive vehicles chasing so few stocks, the risks of—and potential damage from—crowded trades are magnified.

The way we see it, the debate really shouldn’t be about passive versus active. It’s about how and where to deploy each to get the most effective balance of market exposure and potential alpha generation from high-conviction active management.

1Active Share and Fund Performance, Antti Petajisto, 2013

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Copyright © AllianceBernstein