Three Reasons Why US High Yield Belongs in Your Portfolio

by Gershon Distenfeld, Director, High Yield, AllianceBernstein

Looking for a way to increase your US exposure without adding equities? Need more income but worried about rising rates? US high-yield bonds deserve a place in your portfolio.

The high-yield market has had a good run over the last few years—so good, in fact, that some investors may be wondering whether it’s time to cut their holdings. We don’t think it is.

If you want diversified exposure to the US economy, high-yield bonds have an important role to play. Here are three reasons why:

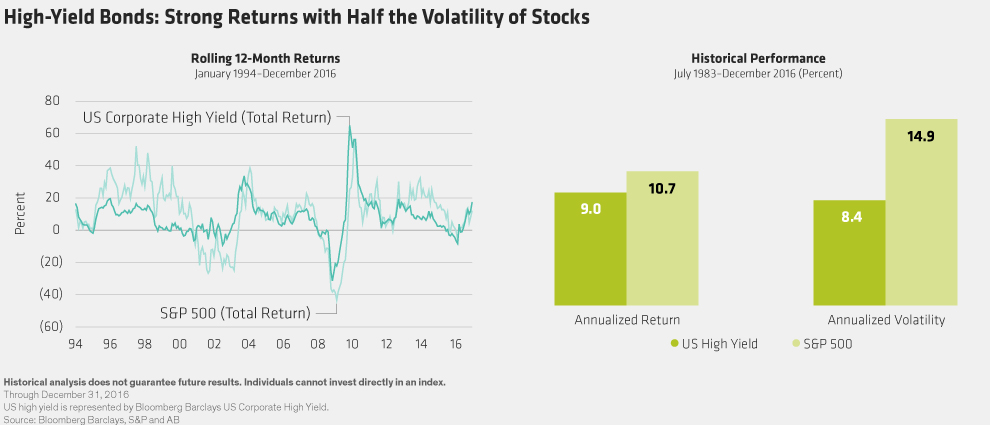

1. High-yield bonds are a great substitute for US stocks. Most investors consider high-yield bonds part of their fixed-income allocation. But they act more like stocks. This is because, like stocks, high-yield bonds are strongly linked to the business results and fundamentals of the companies they represent.

There’s one important difference, though. Over the long run, high yield has produced equity-like returns with half the volatility of stocks (Display). With US equities valuations looking stretched, now may be the ideal time to stir some high yield into the mix.

Of course, high-yield bonds aren’t cheap today, either. Credit spreads—the extra yield these securities offer over comparable government bonds—have narrowed and the market is in the final stages of one of the longest credit cycles in history.

But here’s the rub: history has shown that US high-yield bonds lose less than US stocks during downturns and recover those losses more quickly. A big reason for that is high yield’s steady stream of income—in the form of semi-annual coupon payments—that gets paid in bull and bear markets alike. And as long as an issuer doesn’t go bankrupt, investors get their money back when the bond matures.

Are stocks and high-yield bonds overdue for a correction? That’s hard to say. But when a correction does come—and corrections are not unusual for either asset—we expect high-yield to hold up better and rebound first. In other words, a portfolio that mixes in high yield should provide better protection.

2. High yield usually does well when interest rates rise. Rising rates worry a lot of high-yield investors. But they shouldn’t. Rising rates usually go hand in hand with faster economic growth, and faster growth tends to boost corporate profits—good news for both bond issuers and bond investors. This is why high-yield bonds are generally not as correlated to interest rates as investment-grade bonds.

If anything, income-oriented investors with long investment horizons should be rooting for higher rates. When their bonds mature, they can reinvest the proceeds into newer and higher-yielding bonds, likely increasing their total return.

A rapid rise in interest rates could sting high yield in the near term, though the market would adjust over a long time period. Fortunately, a rapid increase doesn’t seem likely. With just four rate hikes in 18 months, the Federal Reserve has made it clear that it intends to tighten policy gradually. Between 2004 and 2006—the Fed’s last gradual tightening cycle—US high yield delivered an annualized return of 8.5%, outperforming most fixed-income sectors.

3. High-yield bonds have better—and more predictable—return potential than bank loans. Here’s another mistake investors often make when interest rates rise: they ditch high-yield bonds for floating-rate bank loans. The logic is simple enough: floating rates should offer protection as rates rise.

But what many overlook is that loan issuers can call and refinance those loans at will. And with high investor demand driving loan prices up and yields down, they’ve been doing just that. A record $332 billion in loans were repriced in the first half of 2017. That means big savings for issuers and lower-than-expected returns for investors. Loans have returned 1.9% so far this year. High-yield bonds? Nearly 5%.

Generally, we’ve found that the yield you start with when you invest in high yield is a pretty reliable indicator of what you can expect to earn over the next five years. Today’s yield-to-worst for the broad US high-yield market—the lowest likely return you should get barring significant defaults—stands at 5.6%, well above forecasted returns for bank loans or passive equity strategies.

We’re not saying that investors should focus exclusively on high yield. At this late stage in the credit cycle, it pays to be selective and diversified. But with the US economy gaining traction and equities looking stretched, investors simply can’t afford to ignore the US high-yield market.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Copyright © AllianceBernstein