by Zero Hedge

Following on from his recent cautious commentary on low levels of bond yields and equity vol (and cheapness of gold), DoubleLine Capital's Jeff Gundlach outlined details of his views on the markets to CNBC this morning and what the catalyst for "an explosion in volatility" could be.

Gundlach recommends investors "de-risk" their stock and bond portfolios as his "favorite indicator" suggests "yields are going to break out to the upside," and that will lead to market volatility.

"One of the things that I follow to give a really good short-term cyclical indication of the yield of the 10-year Treasury is the ratio of copper to gold," Gundlach said Tuesday on CNBC's "Halftime Report."

The copper-to-gold ratio just hit its highest level since May 2015.

"When the copper-gold ratio is rising it's incredibly suggestive that something is going on that might be a little inflationary," he said.

"It suggests to me yields are going to break out to the upside. ... The leg up in yields will be a catalyst of volatility in the market."

As a result, Gundlach believes it may be wise to lower exposure to assets that are up dramatically during the bull market.

"I think you should be de-risking systematically," Gundlach said.

"Even if it takes six to nine months for the markets to head down you're not giving up very much."

Furthermore, as we noted previously, the bond manager expects the yield jump to cause volatility and is buying puts on the S&P 500...

"One of the biggest manias out there right now is selling vol... because the carry on shorting the VIX is strong as long as volatility doesn't spike very much."

Gundlach believes that the next drop in the markets will "send the VIX not to 10... but easily to 20."

Gundlach notes confidently...

"I'll be disappointed if we don't make 400 percent on the puts, and we don't even need a big market decline for that to happen."

Which makes sense as we noted previously, it will not take much to make the VIX go bananas...

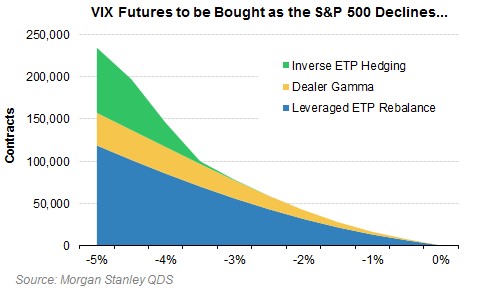

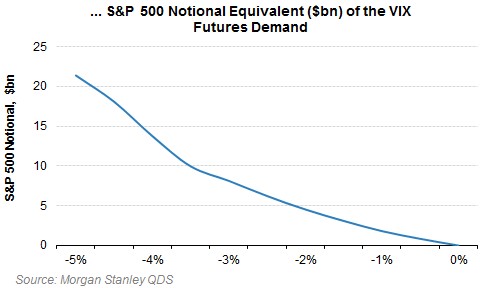

It’s easy to become numb to the low volatility environment and the risks it presents. While trying to pick a trough in vol has been a fool’s errand, focusing on the risks resulting from vol being so low is not. Low volatility has produced a regime where the risks are asymmetric and negatively convex, so being prepared for an unwind is critical. This is not a call that vol is about to spike, but you need a plan if it does.

This note details how a short vol unwind might develop. A violent rise in volatility could be driven by just a 3% to 4% one-day S&P 500 selloff. Right now the risk is greatest in the VIX complex, and demand for VIX futures from three main sources could result in 100,000 contracts ($100mm vega) to buy in a down 3.5% SPX move. For context VIX futures ADV over the last year is 230,000 (although has risen to as high as 700,000 in big selloffs).

Copyright © Zero Hedge