Jeffrey Saut: "Never say never"

by Jeffrey Saut, Chief Investment Strategist, Raymond James

“Never say never. Never say always. Always reevaluate. And never give up.”

. . . An old Wall Street wag

Upon entering this business in 1971 my father gave me this advice:

“Son, if you think the stock market is going up be bullish. If you think it is going down be bearish, but for gosh sakes take a stand! There are far too many folks in this business that talk out of both sides of their mouths such that no matter what the stock market does they can say, ‘See, I told you that was going to happen.’”

Accordingly, Andrew and I take stands on the long-term, intermediate, and short-term direction of the various markets. When you take a stand, especially a short-term stand, you are going to be wrong more often than you think. The real investment trick is when you are wrong you say you are wrong, and you say you are wrong quickly, for a de minimis loss of capital. Being wrong happens to even the best of us. For instance, take a look at my deceased friend Sir John Templeton, and the early performance of the Templeton Growth Fund, as described by Barron’s from an era gone by. I like this story:

. . . the legendary Sir John Templeton began his fund near the top of the 1955 bull market. He raised $7 million (amid as much “market hoopla” as the brokers could generate), then promptly underperformed the S&P 500 the first three years by 17.9%, 8.3%, and 6.7%, a cumulative deficit of 2.9% (with negative absolute returns in two of those three years). As a result of his “dismal record,” Templeton wound up in 1957 with only $3 million in the fund, less than half of what he started with, and his fund ranked 115th (14th percentile) out of 133 funds in the Weisnberger study of relative investment performance. He did not get back to $7 million until 1969, some 14 years after he began. And the rest, as they say, is history.

Being wrong is something most Wall Street pundits never admit to, yet back in March we wrote a report titled “Being Wrong and Still Making Money.” That report discussed a study by Lee Freeman-Shor. In his article the author states that successful investors tend to become either “Assassins or Hunters,” while the unsuccessful investor becomes a “Rabbit” (read it here). Interestingly, currently the conventional call in the financial markets is chronic criticism. Look for the cloud in the silver lining growl the bears. Yet, good investors are instinctively and compulsively contrarians. You have to learn to go opposite mayhem markets. Certainly if you are early it’s indistinguishable from being wrong.

Clearly, we were early when our short/intermediate models flipped positive the week before the presidential election. We even received some pretty curt emails the morning following the election with the preopening Dow futures printing down some 800 points. Nevertheless, in our verbal comment that morning we deemed any weakness a “buy.” Fast forward to late January when those same two models suggested caution in the near-term with the potential for a 5% - 10% pullback and we recommended tilting accounts accordingly. Wrong, for after only a marginal pullback by the S&P 500 (SPX/2439.07) into the beginning of February, the SPX traveled higher into March 1st. In that rally our short-term model turned positive, but the intermediate model did not, so we exercised the rarest commodity on Wall Street – patience. Then in early March the short-term model slipped into negative territory, again looking for a 5% - 10% pullback. Hereto that proved a wrong “call” with the SPX experiencing only a 2.6% drawdown. However, on April 19th those models were in sync on the upside and we said so in these reports.

Then, on May 25th, the short-term models suggested the SPX would “flat line” for the next two weeks and we wrote:

“Currently, we believe a trading high is due here with a subsequent hover around the recent highs in the offing over the next few weeks. Following that, if correct, there should be another whole new leg to the upside. If wrong, our hunch is it will be wrong on the downside with the indices moving higher than most expect.”

That flat line “call” looked good until last Thursday/Friday’s “Two Step” that carried many of the indices out to new all-time highs. So what now?

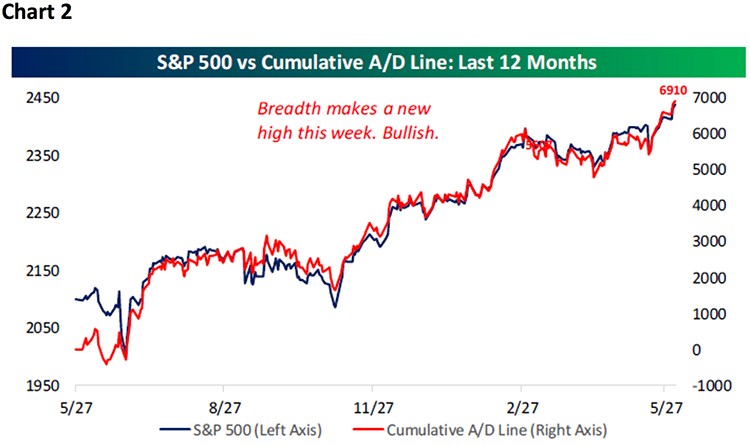

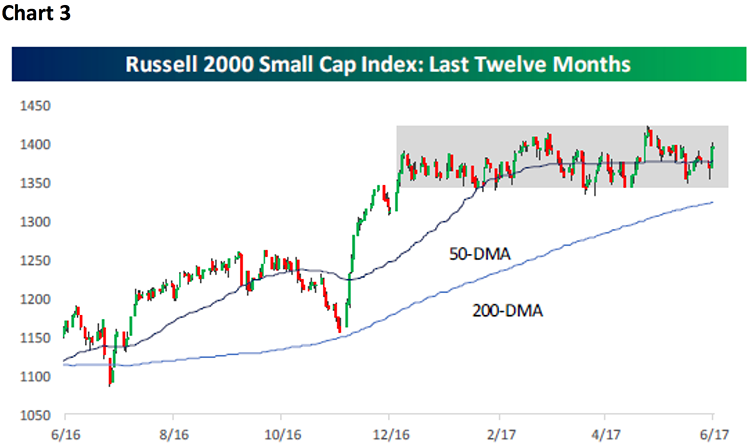

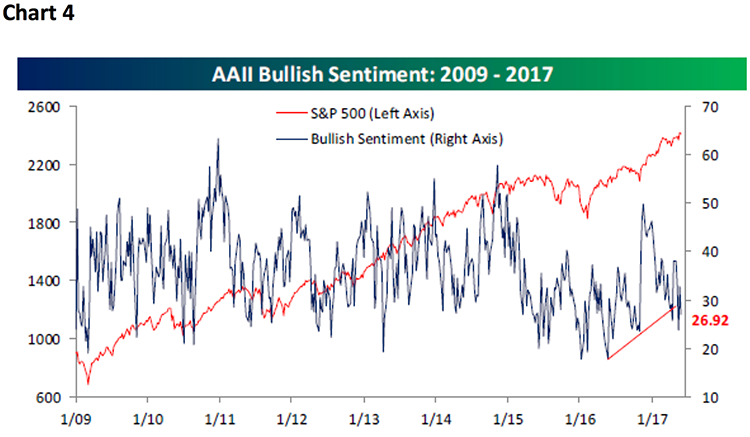

Well, looking at a chart of the SPX over the past 12 months shows that every time that index has broken out above a prolonged trading range it has begun a new leg to the upside (chart 1 on page 3). Stock market breadth is confirming the upside (chart 2), Lowry’s Buying Power continues to expand while Selling Pressure is contracting, the lagging Russell 2000 (RUT/1405.39) rallied late last week (chart 3), earnings remain on the perky side, bullish sentiment still stinks (chart 4 on page 4), and the list goes on. Accordingly, we think the anticipated “new leg to the upside” has begun earlier than our models predicted.

As for what’s driving the upside, readers of these missives should already know why we think stocks are headed higher over the long run, but in this week’s Barron’s Strategas’ Jason Trennert and Daniel Clifton chimed in with some reasons of their own. The last time I spoke with Jason we were at CNBC’s studios and his comments then were just as cogent as they were in Barron’s. To begin, they posited that investors are assigning a low probability of President Trump getting his agenda through. That should create opportunity in 2017’s second half. On the regulatory side, they doubt Dodd-Frank will be changed, but noted that the Fed’s bank stress test could be eased, allowing some $100 billion in excess capital to be returned to shareholders (like Andrew and I said last week, “buy the banks”). Of particular interest was this quip from Jason, “Since the 1980s, there has never been a period in which a rise in small-business confidence didn’t lead to a pickup in nominal gross domestic product.” Another gem was, “A variable cost of capital will greatly aid active managers, because it will increase dispersion and lower correlations (if that sounds like me it should). Of course, there were other gleanings like, “Repatriation (of offshore profits) would boost earnings per share by $2.58 on the S&P 500 in 2018 (and) if you have successful tax reform you’re looking at $7 to $8 of additional EPS in 2018.” To which we add, “Well said!”

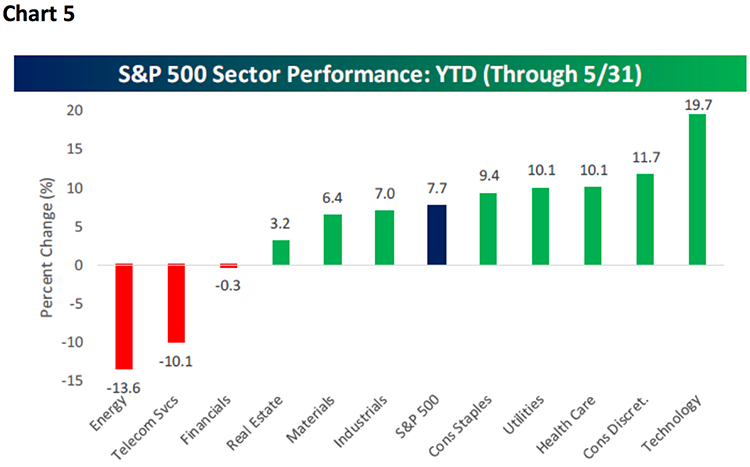

The call for this week: While select negatives remain, the path of least resistance is to the upside, much to the surprise of most participants. We like the idea of buying some of the laggards. In the Barron’s article Jason recommended buying the SPDR S&P Regional Banking exchange-traded fund (KRE/$52.36). I continue to own and like my friend David Ellison’s Hennessy Small Cap Financial Fund (HSFNX/$24.17). David is also the portfolio manager of the Hennessy Large Cap Financial Fund (HLFNX/$19.27). Another laggard is the Energy sector (chart 5); here we like select favorably rated names from our Master Limited Partnership (MLP) research universe. In fact, we think commodities in general are attempting to form a double bottom in the charts (chart 6) and would add this asset class to portfolios. This morning the preopening futures are flat despite the grip of more terrorism over the weekend as the sun rises over the transom of my boat.