Three ways we manage risk in emerging markets

by Jeff Feng, Head of Emerging-Markets Equities, Invesco Hong Kong Ltd. Invesco Canada

Many investors perceive emerging markets (EM) as a risky place to invest their money. Visions of faraway places with different approaches to business, regulation and governance can be intimidating, but the reality in many EM countries is very different today than it was just twenty years ago. In this blog post, I’m going to discuss the three main ways our funds differ from others when it comes to managing risk and maintaining a strong risk/return profile for our EM investments.

Focus on rising middle class

An important element of our funds that helps mitigate risk is a distinct focus on consumption-related businesses. In my opinion, the most certain investing theme in emerging markets is the rise of middle-class consumers. This simple fact, which has proven true the world over, is that when people have more money in their lives, they start to spend beyond the basics. As they become able to, people will buy things like cosmetics, entertainment, vacations and even enhanced education for their kids. This type of consumption is far more predictable than commodity prices, which are driven by myriad of volatile forces. To illustrate how this plays out in our investing, Trimark Emerging Markets Class is currently made up of 21.25% consumer discretionary companies and just 6.79% industrials and 0% resources (as at April 28, 2017).

Dedicated discipline

Ultimately, our investment discipline is what drives every buy or sell decision. We use the acronym FORS to refer to our business-quality criteria:

- Free cash flow

- Organic growth

- Returns on invested capital

- Sustainable competitive advantage

We focus strictly on finding high-quality companies that generate high free-cash-flow conversion, above average organic growth rates and high returns on invested capital. In addition, we want to see all of these protected by a sustainable competitive advantage. Essentially, this means we want growing companies that earn good returns on shareholders’ capital, produce a lot of cash, and have some business elements that make it very hard for others to replicate – allowing the company to dominate in its field with little fear of others stealing market share.

High quality companies tend to perform better in difficult times. In fact, in my experience they tend to grow over time by taking market share away from weaker competitors, particularly when the economy is weaker and they are able to leverage their relative balance-sheet strength and robust free cash flow.

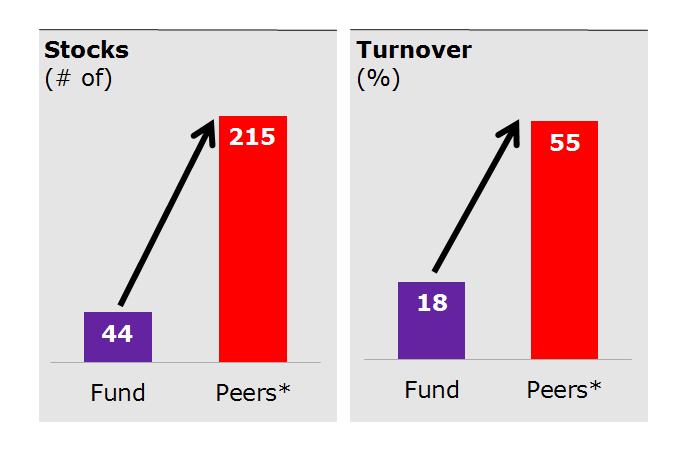

Know before you buy

Guided by our FORS investment discipline, our day-to-day process is vital to both risk mitigation and the strong performance of the fund. Our research process is long, in-depth and thorough. The average historical turnover rate for Trimark International Companies Fund is approximately 18% – very low compared with our competitors in the marketplace. We are extremely prudent in terms of the names we put in the portfolio. We do not make decisions based on what’s held in any benchmark index, and our research allows us to have high-conviction in our decisions.

Sources: Invesco Canada and Morningstar Research Inc., as at April 30, 2017. Underlying data is as of April 30, 2017 or latest reported.

This chart is for illustrative purposes only.

*Peer data represents an average of those funds within Morningstar’s International Equity category and excludes fund of funds and index fund structures.

There could be major differences in the objectives, investment strategies, fees, costs and other factors among the funds included in the average.

At the portfolio level, we carefully evaluate risk exposures both backward- and forward-looking. Backward-looking means that on a quarterly basis we look at the risk profile to ensure nothing has significantly shifted based on the movement of individual stocks within the portfolio. Forward-looking means that whenever we want to add a new company to the portfolio, we review every aspect of the risk profile to determine how the addition would change the risk exposure of the overall portfolio. That is a key part of our portfolio construction process. We tend to start with a 1% allocation and move up toward 3% during the initiation phase of purchasing a stock. We don’t typically allow our positions to go above 7% and if a company’s stock price drops 15% below our cost base, we re-evaluate our initial thesis, from both a qualitative and a quantitative perspective to determine if it continues to provide a sufficient margin of safety to continue owning during what we believe is a temporary downturn.

We are focused on quality companies and want to take advantage of the continued growth of the middle class in many emerging market countries. In my opinion, these three things – business quality, consumption-driven investment focus and disciplined portfolio construction – work together to create a portfolio that seeks to generate better risk-adjusted returns for our investors.

*****

For more information on funds managed by Jeff:

Trimark International Companies Fund

Trimark Emerging Markets Class

Trimark Global Fundamental Equity Fund/Class

This post was originally published at Invesco Canada Blog

Copyright © Invesco Canada Blog