Cheap for a reason? Beware the value trap

by Nick Kalivas, Senior Equity Product Strategist, Powershares (Invesco), via S&P Dow Jones Indices

What is a value trap?

While value can be an appealing investment strategy, identifying value opportunities is not as easy as it might appear. One of the drawbacks of value investing is the so-called “value trap.” A value trap occurs when a stock appears cheap, but is trading at low multiples due to underlying problems with the stock’s issuer. In other words, the stock is cheap for a reason and could trade even lower in the future. Changing industry conditions, secular shifts in technology, and management miscalculations can lead to value traps. Further, some valuation measures may be backward-looking when the market is pricing the future.

Value traps are real. Let’s take a look at two examples:

With only a few exceptions, between January 2011 and February 2016, Target’s price-to-earnings (P/E) ratio ranged within two points of the P/E ratio of the S&P 500 Index. However, in the spring of 2016, Target’s P/E ratio started moving lower, with its ratio spread to the S&P 500 Index widening to 6.5 by October 2016. Judging by its discounted P/E ratio, Target stock appeared inexpensive — “a value” to the broader market. At the close of October 2016, Target shares were priced at $68.73. Despite this discounted P/E ratio, however, Target’s stock went on to fall an additional 20% to $55.19 by March 2017. By contrast, the S&P 500 Index rose 11.1% over this same period, leading to a yawning P/E discount of 10.77.

In retrospect, Target’s valuation compression appeared linked to competitive pressures, a long-term trend toward online shopping, and changing consumer preferences and buying habits. Whatever the reason, Target’s stock price decline in the face of a low P/E ratio illustrates how difficult and risky ascertaining real value can be.

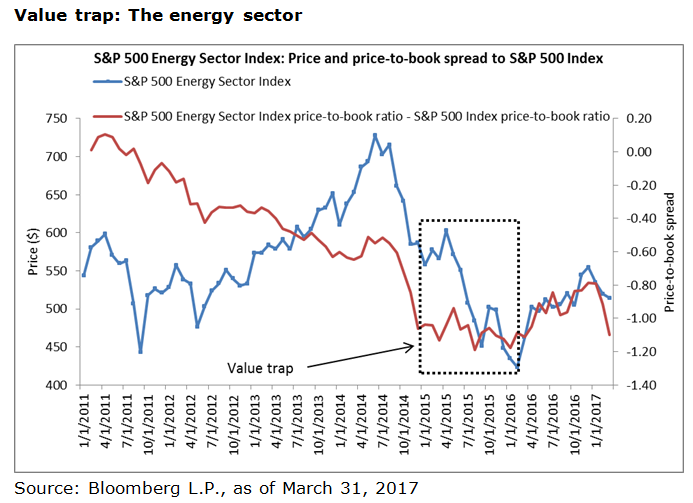

Another interesting case of a value trap can be found in the energy sector. (Given the high volatility of energy P/E ratios, I use price-to-book ratios in this example.) On a price-to-book basis, the spread between the S&P 500 Index and the S&P 500 Energy Index went from 0.10 in April 2011 to -1.04 by the end of January 2015. Despite these low valuations, the price of the S&P 500 Energy Index retreated another 24% over the ensuing 12 months. So, even though the energy sector had become more attractively priced, energy prices continued to drop — again highlighting the difficulty in discerning value. By contrast, the S&P 500 Index declined only 3.1% across this same period.

The energy sector’s valuation compression was based on the surprising weakness in oil prices, which are a key determinate of energy company revenue and profitability. Front-month West Texas Intermediate crude oil futures were priced at over $100 per barrel in June 2014 and had plunged to less than $35 per barrel by March 2016. The increased use of fracking — a disruptive technology change — played a key role in the energy sector’s value trap. Even though fracking was not a new concept in 2014, its impact on production, coupled with an ongoing economic slowdown, contributed to valuation compression within the energy sector.

Overcoming value traps

One way to overcome value traps may be to combine the value and momentum factors. This is because the value factor can screen for stocks that are attractively priced, while the momentum factor looks for stocks that have recently demonstrated strong risk-adjusted returns, which may help reduce the probability of buying into a value trap. Rising value stocks may be a sign that value is being unleashed and a stock is moving toward its intrinsic value.

Of course, there is always the risk that momentum stocks fall out of favor as market conditions shift. Companies can report bearish business developments that can reverse a positive price trend and catch investors leaning the wrong direction. Moreover, the momentum factor can struggle during periods where investors are reducing risk and asset returns are highly correlated.

The momentum factor may also provide an opportunity to manage risk. This is because value stocks showing poor momentum can be removed from a portfolio (depending on when it reconstitutes), reducing the chances of continuing to hold a value trap.

Copyright © S&P Dow Jones Indices