A Spring Revival of Economic Growth

by Carl Tannenbaum, Asha Bangalore, Northern Trust

Incoming “soft data” and “hard data” conveyed vastly different U.S. economic conditions as the first quarter unfolded. The actual real gross domestic product (GDP) report for the first quarter settled the debate, with the message from hard data prevailing over the former.

Markets have scaled back expectations on both the timing and size of any tax cut and infrastructure spending packages. We continue to believe that there is only a small chance of a fiscal policy package being put in place in 2017.

The 0.7% increase in real GDP during the first quarter reflects a sharp drop in auto sales, a big reduction of inventories and the impact of residual seasonality. Research from the Federal Reserve Bank of Cleveland indicates that residual seasonality has held back first-quarter real GDP growth by 0.8 percentage points between 1985 and 2015, suggesting that the opening three months of this year were not as weak as it might initially appear.

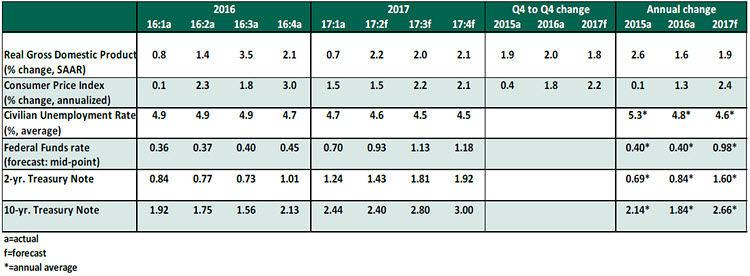

Key Economic Indicators

Key Elements of the Forecast

-

- Consumer expenditures rose only 0.3% in the first quarter, the weakest reading since the fourth quarter of 2009. Auto sales declined in the first quarter after a large increase at the end of 2016. As we discussed last month, car sales are being hindered by an overdue correction in credit conditions. An unusually warm winter held back expenditures on utilities during the first three months of the year. A partial reversal of these factors is projected for the second quarter.

-

- Nonresidential investment expenditures on both structures and business equipment offset weaknesses among other components of first-quarter GDP. Although continued growth of structures outlays is unlikely in the second quarter, business spending on equipment and software should maintain an upward trend. The oil rig count continues to advance, implying that oil-related industry is back in play after a setback following the plunge in oil prices.

-

- Residential investment expenditures have posted two strong quarterly gains. The moderate growth outlook for the housing sector stems from cross currents. On the one hand, solid employment conditions bear positively on housing demand. At the same time, the influence of strict mortgage underwriting practices and higher home prices in some parts of the country are negatives. Also, a significant accumulation of student loans in the current expansion is another factor that has lowered the creditworthiness of potential homebuyers and prevented household formation. Consequently, a measured pace of activity in the housing sector is most likely in the quarters ahead.

-

- The April unemployment rate at 4.4% is a cycle low reading, and below the range the Fed designates as full employment. Long-term unemployment and the number of discouraged workers are close to the pre-recession level. Part-time employment for economic reasons is also at a cycle low. Nonfarm payroll employment advanced 211,000 during April, a step up from the revised gain of 79,000 in March. Hourly earnings moved up 7 cents in April, but the underlying trend (+2.6% from a year ago) is muted. The Employment Cost Index, a broader measure of labor costs, increased 2.4% from a year ago in the first quarter after moving up 2.2% in the fourth quarter. The bottom line is that an acceleration of employment compensation is not visible even though the economy is at full employment.

-

- Inflation readings slipped slightly in March. The March personal consumption expenditure index rose 1.8% from a year ago versus a 2.1% increase in February. The core personal consumption expenditure price index, which excludes food and energy, was up 1.6% in March, down 20 basis points from the prior month. Inflation is predicted to move close to the Fed’s 2.0% target as the economy continues to grow close to its potential capacity.

-

- The 10-year Treasury note yield is up about 20 basis points from the low registered in mid-April, but below the 2.62% mark reached in mid-March. Essentially, the bond market has reassessed the likelihood of a fiscal stimulus package and the prospect of a populist revolution in Europe.

- The Fed held the policy rate unchanged (0.75% to 1.00%) at its meeting last week and considers the first quarter slowdown in U.S. real GDP growth as a transitory event. This view and the sanguine labor market report enhance the case for a higher policy rate at the June 13-14 meeting.

northerntrust.com

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2017 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

Copyright © Northern Trust