Fear Not: EM Bonds Can Handle Higher Rates, Trump - Context

by Shamaila Khan, EM Fixed Income, AllianceBernstein

Higher interest rates, a stronger dollar and Donald Trump: three reasons to avoid emerging-market (EM) debt? Not necessarily. Rising rates seem to be signaling faster growth, and that’s good news for many EM bonds and currencies.

EM debt—both US-dollar and local-currency denominated—produced solid returns in 2016. But most came in the first half of the year. Donald Trump’s victory in the November US presidential election and his fiscal stimulus plans left investors scrambling to price in higher inflation. That pushed up US Treasury yields and the dollar.

As a result, EM bonds and currencies took it on the chin. Global investors worried that higher US rates would draw money out of EM assets and into US ones, putting pressure on EM government and corporate balance sheets. Trump’s antitrade platform and his pledges to rip up trade pacts didn’t help sentiment, either.

Does this mean it’s time for investors to retreat from emerging markets altogether? We don’t think so—for several reasons. To start, let’s look at rising US rates. Yes, long-term rates are higher, and the Federal Reserve may raise short-term borrowing costs more quickly in 2017 than investors expected just a few months ago.

GROWTH IS GOOD

But here’s the thing: why rates rise matters. In this case, markets are clearly pricing in faster growth and higher inflation, and a stronger US economy should boost economic activity elsewhere, emerging markets included. It’s especially good news for EM commodity producers, who stand to benefit from any further stabilization or rise in the prices of oil, gas, metals and other natural resources.

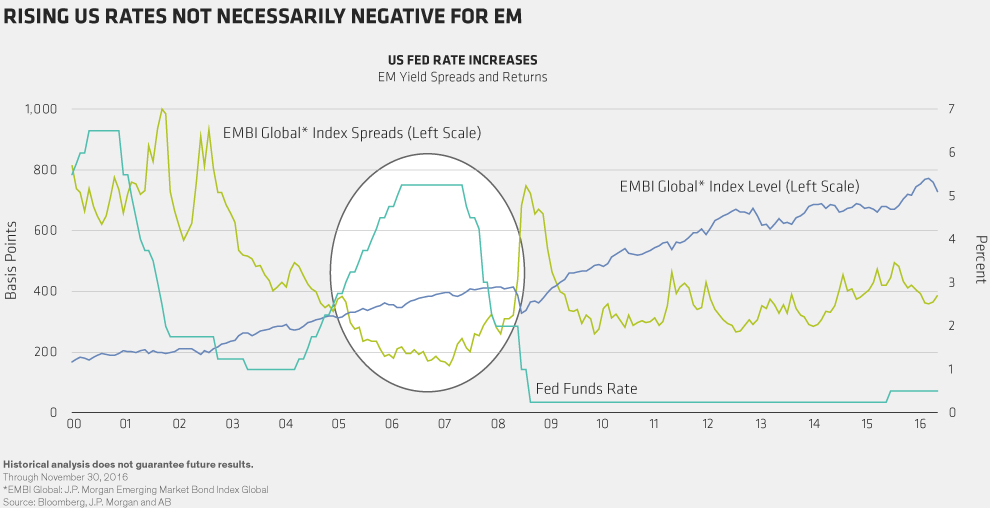

As the following Display shows, a period of gradual Fed rate increases and improving growth can coincide with tighter EM yield spreads and rising returns. On the other hand, the past several years of extremely low growth and rates in the US and other developed economies have hurt emerging economies and EM assets.

HOW EMERGING MARKETS BUILT UP SHOCK RESISTANCE

What’s more, rising rates aren’t a big problem for emerging markets today. That’s because many countries, including South Africa, India, Indonesia and Brazil, have spent the past few years chipping away at their external imbalances and reducing large current account deficits. The adjustment was painful, but it’s paying off in the form of stronger economic fundamentals, and it leaves EM assets less vulnerable to rising rates and other external shocks.

That wasn’t so in 2013, the last time US Treasury yields spiked suddenly. Back then, most emerging markets were on a borrowing binge. When rates rose, the flow of capital into these economies quickly dried up.

AN ATTRACTIVE PAIR: HIGH YIELDS, LOW INFLATION

There’s another reason why EM debt looks attractive: stable inflation. Most EM currencies have clawed back the losses they suffered against the dollar in the weeks after Trump’s victory, which should keep inflation in check. Firmer commodity prices should also provide support for many EM currencies..

Many developed countries are moving in a different direction. Japan has embraced fiscal expansion, and Trump has pledged to cut taxes and spend up to $1 trillion on infrastructure over the next 10 years. Markets are betting these policies will lead to inflation.

The result: inflation-adjusted real yields on EM bonds are among the highest available, and real interest-rate differentials between emerging and developed markets are close to their highest level since the global financial crisis.

WINNING WITH A HANDS-ON APPROACH

What about President-elect Trump? While he campaigned on an antitrade platform, we can’t claim to know which policies he’ll pursue in office or which will become law. Protectionist policies may put pressure on open economies like Mexico or many in Asia that are heavily exposed to trade with the US. But commodity-producing countries will be less affected, provided commodity prices continue to stabilize or rise.

In other words, there’s still plenty of value to be had in EM bonds and currencies. But finding it requires an active, hands-on approach. Blind faith in an index exposes investors to the good and the bad alike. It takes a more selective approach to uncover the winners and boost the income-generating power of your portfolio.

Of course, policy uncertainty in the US and beyond will keep markets volatile. But shying away from all EM debt amounts to tarring every asset with the same brush. We think that could be a costly mistake.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Copyright © AllianceBernstein