by Robert Stammers, CFA, CFA Institute

All professionals have sought to acquire new habits and skills over the past few years.

Ambitious strivers read highly celebrated books such as Stephen Covey’s The 7 Habits of Highly Effective People, Dale Carnegie’s How to Win Friends and Influence People, and Spencer Johnson’s Who Moved My Cheese? to gain an edge in hopes of improved performance and individual achievement.

Despite these efforts, many investment professionals continue to exhibit behaviors that negatively influence performance. Unfortunately, bad habits are difficult to break, cemented through years of experience and encouraged through firm mandates, compensation structures, and an individual’s performance goals.

Recognizing Bad Habits

If individuals and firms are going to be effective at eliminating these bad habits, the first step is to identify the most egregious — those that seriously impede the achievement of long-term client goals. To help, we asked CFA Institute Financial NewsBrief readers what patterns they thought were the most counterproductive.

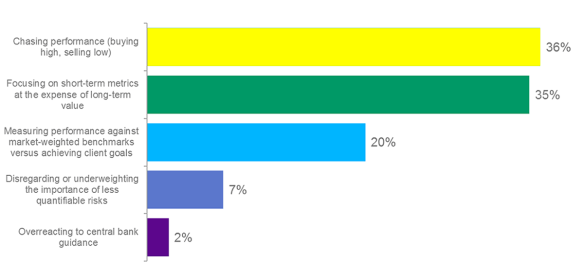

Which of the following habits exhibited by investment professionals is most harmful to clients?

According to the 608 respondents, the two practices most likely to adversely affect clients are chasing performance (buying high, selling low), with 36% of the vote, closely followed by focusing on short-term metrics at the expense of long-term value, at 35%. Measuring performance against market-weighted benchmarks versus achieving client goals garnered 20% of the responses.

By contrast, poll participants viewed disregarding or underweighting the importance of less quantifiable risks (7%) and overreacting to central bank guidance (2%) as less harmful.

It’s no surprise that the habits that focus on short-term performance rather than long-term client objectives would be found most troubling. The question is: What needs to be done at the individual and organizational level to motivate professionals to do the right thing?

Misdirected Motivation

A new study conducted by State Street Center for Applied Research (CAR) and the Future of Finance provides insight into how organizations can motivate better behavior and improve organizational and individual performance. “Discovering Phi: Motivation as the Hidden Variable of Performance” explains the discovery and meaning of a hidden variable — “phi” — that can affect performance. The Greek letter phi is used as an acronym for the motivational forces of purpose, habits, and incentives.

According to the research, high-phi professionals are high performers who have a sense of purpose directed toward realizing client goals. High-phi firms can expect greater organizational performance, employee engagement, and client satisfaction.

The research suggests that investment management professionals are highly motivated. More than half of the 3,300 surveyed said they were in the industry because they were passionate about finance. The research also found, however, that a majority of those same professionals are also demotivated in some way. This implies that their hard work, passion, and motivation may be misdirected, funneled into the general goal of outperforming the market rather than delivering on a client-specific value proposition.

In addition, 36% of asset and wealth managers indicated that acting in their client’s best interest exposed them to various types of career risk. Investment professionals are expected to make decisions based on their client’s long-term time objectives, but their performance and incentive structures are evaluated on much shorter timelines.

Changing Habits

The motivation study suggests that investment management is a low-phi industry. So what needs to change?

Corporate culture and compensation structures must be reformed to incentivize behaviors that achieve long-term client objectives. For that to happen, firms need to foster a sense of purpose in their employees, one rooted in creating value and serving the greater good. Instead of relying on mission statements and other corporate slogans, firm leaders have to to articulate a compelling vision and act in accordance with it.

Successful firms instill a sense of ownership and corporate citizenship in their employee and offer ample opportunity for professional development, fostering both soft skills and those that influence investment decision making.

Leadership must identify and eliminate old and ineffectual habits and develop strategies to instill new client-centric ones. Many firms will need to realign their purpose around client needs rather than short-term metrics. Indeed, according to the study, decisions should be driven more by phi than by a concern for short-term performance.

Behavioral change does not have to be driven wholly by the firms themselves. Clients can influence adviser motivation and behavior by building a trust relationship, ensuring that their goals are understood and that achieving those goals is the basis for measuring performance.

Investment professionals need to be introspective. They need evaluate their behavior and determine whether their habits truly serve their clients. They should continue a career-long program of identifying and incorporating those skills and behaviors proven to benefit clients. Those professionals and firms that learn to break the cycle of negative or ineffectual habits will ultimately add the most value.

Copyright © CFA Institute